")

Judging from the numbers at the tail end of the third phase in the Lebanese lockdown and the start of the transition to a winding-down phase, the picture is flawless from the medical and from the insurance supervisory angle: Lebanon’s case count of severe COVID-19 illnesses up to the second half of April 2020 has been medically and administratively manageable. There was no need for dreaded selections by attending physicians—of who would get respiratory support on a ventilator and who would not—and, in a proxy indicator, there was no undue stress on the hotline of the Insurance Control Commission because of hospitalized persons’ complaints over exclusion clauses in their existing medical insurance policies.

And although trust in politicians is as rare as a $100 dollar bill in an ATM these days, one had absolutely no need to rely on assurances by government ministers or community leaders to believe the unfathomable: that something in this country was moving the right way. The numbers confirmed that the country has so far been responding with uncommon effectiveness to the medical dangers of the COVID-19 pandemic.

Firstly, the around 700 confirmed cases up to the last days of the third lockdown period have been reassuringly low, with a slow rate of increase. This impression is compelling, notwithstanding the under-powered testing for coronavirus infections in the population. Even if one hypothesizes a gap between actual infections and confirmed infections to be in the thousands of cases, or upward of 1000 percent, it seems simply implausible that a high cresting of severe COVID-19 infections would have gone unnoticed across the entire (very small) country—particularly when one takes into account the country’s intensity of social communications, the high connectivity of family networks, and the recent protest movement’s shattering of previous social barriers to free expression.

More significantly, no alarming developments have been observed in the crucial count of deaths from the pandemic. There may be—and this must be assumed with high degrees of certainty—individuals who are not included in the official fatality number of 24 as of April 25 because they passed away in their homes in villages or perhaps behind the veils of emergency tents in the southern suburbs. There may thus be deaths related to the pandemic that did not get reported as COVID-19 fatalities. But fatalities show in national statistics even if they are not attributed to the pandemic. And the overall seasonal fatality numbers in Lebanon have not been reported anywhere to be in vast excess over those of previous years, contrary to what the statistics show for countries such as Italy, France, Spain, and the UK, and also are beginning to show for New York City in the United States.

For the months of March and April, available data from these most-affected countries show that total fatality counts—attributed to COVID-19 or not—have increased undeniably, thereby strengthening the case for vigilant coronavirus containment measures in those countries and countering conspiracy tales that suggested normal death rates to have been present.

In Lebanon, a conceivable theory of hidden death counts would go in the opposite direction, not alleging that overall fatality numbers were the same as every spring as conspirationalists say in Europe, but alleging that the number of COVID-19 fatalities in this country from the last six weeks is seriously underreported. Of course, the statistics of weekly deaths in Lebanon this April might very well not be available for many weeks and then only as reliable as any other tally in a statistically impaired country. But the question remains if a statistically significant and communally unnoticed aggregation of March/April fatalities in the hundreds or thousands could really occur here.

Deaths per 1 million inhabitants in the pandemic’s worst-hit countries were reported to be multiples of what was this spring observed in Lebanon in terms of deaths per capita. Could a proportional increase of such magnitude have been kept hidden from attention in Lebanon’s small and family-centric society? In a country with this newly hyper-sensitive and protest-eager civil society?

Upon accepting that the Lebanese response to the COVID-19 pandemic to date has shown good results and saved lives—but without drawing the false conclusion that the country will continue to be spared from worse developments—quite a few questions remain. And these are questions that urgently wait to be answered as the global moods shift from containment of the virus to alleviating the repercussions of lockdowns on economies.

As the pandemic’s current wave might be slowing in some countries and yet must be expected to surge in others, and as a following wave is expected by many epidemiologists to strike later this year, the question for policy-makers and governments is how to balance the need for a restart or reinvigoration of economic activity on the one hand with the need for containment of the virus on the other. For corporate strategists and investors, the challenge is to limit sunk costs, identify sustainable opportunities that emerge in the wake of the pandemic, reorient teams from old economic nags to new stallions, and also assess risks of the coronavirus recession that might manifest with a delayed fuse.

Both of these uncertainty complexes—the need of policy-leaders to reduce economic risks while staying on top of the containment and treatment needs, and the need of economic agents to assess risks and potential new rewards in the business landscape—have the common denominator of risk evaluation and risk management. This bears the question, if pertinent evaluation on the balance of medical and economic coronavirus risks or hints for economic opportunities could be procured from the industry that has prided itself over all others as harboring top expertise in the assessment and management of risks in the global economy. This is the insurance industry with its more than $5 trillion in premiums, or more than 6 percent of global GDP in 2018.

Not all bad news

Curiously, while wave after wave of bad news have been hitting the world economy during the coronavirus crisis, the globe’s insurance giants and reinsurance behemoths have not constantly been in the front row of bad news during the pandemic—as opposed to banks, manufacturing, construction, real estate, hospitality, event, entertainment, tourism, and travel companies as well as all sorts of micro, small, and medium businesses. But insurance interacts with all these economic agents as well as with the, so far, significantly fewer sectors that are named as the best winning bets in the pandemic, such as pharma and biotech companies or online networking, communication, and entertainment companies.

Where then is insurance itself positioned in context of the global recession, and what can insurance mathematicians, or actuarial consultants, tell us about the changing risk landscape that nations have to navigate with painfully dwindling resources?

As a preamble to looking at those questions, two facts deserve to be noted: Insurance leaders and risk analysts have for years considered the increasing risk of a human pandemic. The threat level assessment of a pandemic, however, had been ridiculously low when viewed against the real unfolding costs of the current pandemic.

Illustrating the limits of risk surveys and models are, for example, the annual risk maps compiled by the World Economic Forum, which in January of this year named climate risks, economic confrontations, and “domestic political polarizations” as the risks that were top on the minds of economic elites.

But underestimation of pandemic risk by several dimensions of magnitude was found also in more specialized academic exercises such as the annual global risk assessment published by the Cambridge Center for Risk Studies (CCRS) in the UK. In the 2019 global risk index by CCRS, a human pandemic is the fourth-largest threat in a list of 22 modeled risks that threaten the economies of urban centers around the world. These urban productivity hubs collectively account for over 40 percent of the global economy by CCRS’ reckoning.

Reiterating a warning from previous editions of the index publication, “Whether it is due to the global nature of supply chains, urbanization or climate change, we see that the potential for epidemics to extend their reach is increasing,” CCRS noted, and stated further, “There is little doubt that a pandemic is due to occur again … but how it will unfold will remain highly variable and dependent upon emergency planners and the insurance community.”

Given that the study’s projected pandemic threat was quantified at $49.9 billion, accounting for 9 percent of the index’s total global GDP at risk of $577 billion, the conclusion imposes itself that the risk of a pandemic was known but thoroughly misunderstood and insufficiently modeled by leading risk experts.

Acknowledging the caveat that the unprecedented experience of the coronavirus crisis complex trashes existing conventional wisdoms of economic leaders and nullifies the risk modeling capacities that are based on historic data inputs, the question becomes what economic burdens insurance and reinsurance companies will be faced with during and after the pandemic? The current perspectives of analysts are mixed with some bright spots being projected but the longer term outlook is highly uncertain with swathes of darkness.

For the immediate physical threat perspective of the coronavirus risks, insurance companies and insurance professionals are generally not in the vision line when compared with audience-facing economic activities during the pandemic. In an assessment of physically risk-prone professions during the coronavirus crisis in the United States, data visualization site and online publisher Visual Capitalist listed occupations with high risk exposure. The 40 most risky jobs in that list are top heavy in healthcare (with dentistry-related occupations taking up half of the lead group in riskiness), but also include flight attendants, bus drivers, kindergarten teachers, supermarket cashiers, municipal firefighters, food preparation supervisors, hairdressers, and supervisors of correctional officers.

In this context of coronavirus risk which does not include economic exposure, financial services providers, including bank tellers, would expectedly not be showing near the top of risky occupations, and teleworking insurance professionals are decidedly not considered to be in a high-risk occupation. But even when the attention turns to economic exposure, remoteness from the immediate risk landscape is generally perceived to apply to the insurance industry. Specialized agency Fitch Ratings said in April that it revised its general outlook to negative for all insurance companies/regions globally and specifically mentioned negative outlooks for the life insurance sectors of developed markets and the health insurance sector in the US. However, the agency kept its ratings outlook stable for global non-life, general reinsurance, and title insurance sectors.

Also notably, the world’s two largest reinsurers by premiums, Munich Re and Swiss Re, announced that their dividend payouts this spring would be as projected (and generous looking) as earlier in the year. The companies presented themselves optimistic but nonetheless acted cautiously, by postponing a share buyback program in case of Swiss Re, while Munich Re said in a press release it would not retain a projection of annual profit of €2.8 billion.

In the outlooks of insurance analysts, the issue of burdens on insurance and reinsurance companies actually has become a global concern. Health insurance is the obvious insurance line that comes to mind when thinking about immediate insurance implications of the coronavirus. In this regard, however, the cost of the pandemic to health insurers is from a global perspective not yet assessable. This is because of the large differences in healthcare systems and insurance components between countries and also because of uncertainty about treatment requirements, mortality and morbidity rates of the diseases, and their associated costs, writes Laura Hay, the global head of insurance at KPMG International.

The possibility of billions of dollars in short and medium-term costs for health insurers and reinsurance companies notwithstanding, Hay notes that the outlook for health insurance does not entirely exclude positive scenarios, pointing out that the shock of the pandemic will translate into a significant leap in health insurance awareness and demand, especially in developing countries with underinsured populations. A temporary spike in demand for critical illness policies occurred in Asia after the SARS epidemic, and a parallel phenomenon would be possible post-corona, “with rising sales of health insurance, critical illness, and even life cover around the world,” Hay speculates.

Similarly, consultants Bain & Co wrote in early April that health insurance payers of COVID-19 covers face risks of long-term respiratory care costs, medical loss ratios, and weakening of returns on financial markets and assets. However, the expectations by Bain also entail upside risks. “In an overstrained clinical environment, most non-Covid patients will have challenges gaining access to care,” write Bain partners Joshua Weisbrod and Vikram Kapur. “From a financial standpoint, payers will face significant pressure on their medical loss ratios. That shift will be offset by a severe decline in high-cost elective surgeries.”

Moreover, increased health awareness can also, according to Bain, be anticipated under the pandemic’s trigger effect. “In emerging markets such as China, we already see a significant rise in insurance penetration above and beyond the levels that followed previous pandemics such as SARS,” the consultants observed.

Precedents for the catalytic effect of major disasters and man-made catastrophes on insurance demand reach from historic examples such as the Great Fire of London in the 17th century and the San Francisco earthquake at the threshold of the 20th century to contemporary examples. The latter, while not unilaterally positive from a business point of view, triggered a rethink of correlated catastrophe losses and terrorism insurance as issue of national concern after 9/11 or narrow/transitory demand increases for property and business interruption protection after flood events and changes in demand, risk, and claims of political violence insurance after occurrences of civil disturbance or popular unrest.

In contrast to a mixed outlook of highly probable near-term costs and possible long-term opportunities in health insurance lines, insurance experts from various organizations have rattled off warnings about the pandemic’s impact on insurers and reinsurers, which could reach far beyond the cost of health insurance and life insurance claims. Thomas Wade, the head of financial services policy at the American Action Forum, a conservative advocacy organization in the United States, warned in mid-April against governmental attempts to make insurers pay claims for business interruption insurance that comes with exclusions for incidents related to pandemics. The expert argued that forcing such steps in legislation would be damaging to contract law, run counter to the fundamental business model of insurance as an instrument of risk mitigation by risk sharing, and altogether could kill insurance. “Were insurers to have to pay business interruption claims, it is likely that this would bankrupt the industry,” Wade darkly augurs.

Citing risk modeling studies from the last few years, Joy Langford, a partner at international law firm Norton Rose Fulbright, warns that the pandemic could unleash a casualty catastrophe for reinsurers, meaning a scenario that extends across different geographies and involves claims from multiple policyholders across different insurance categories. In anticipation of years of needed clarifications and legal disputes over insurance covers on the global mega-event of the pandemic, Langford says that impacts of claims related to the coronavirus recessions could hit reinsurers not only in business lines of health, life, and pension insurance but also have significant general insurance impacts on liability, travel, credit, business interruption, workmen’s compensation, and a number of lesser business lines. She refers to a hypothetical scenario paper produced for the CCRS (not part of the official threat assessment), which projected possible insurance losses of hundreds of billions of dollars in a pandemic. “What can be confirmed by the events of recent months is the accuracy of CCRS’ hypothesis that a global pandemic could present the insurance industry with the type of casualty accumulation capable of rising to the level of casualty catastrophe,” the lawyer points out.

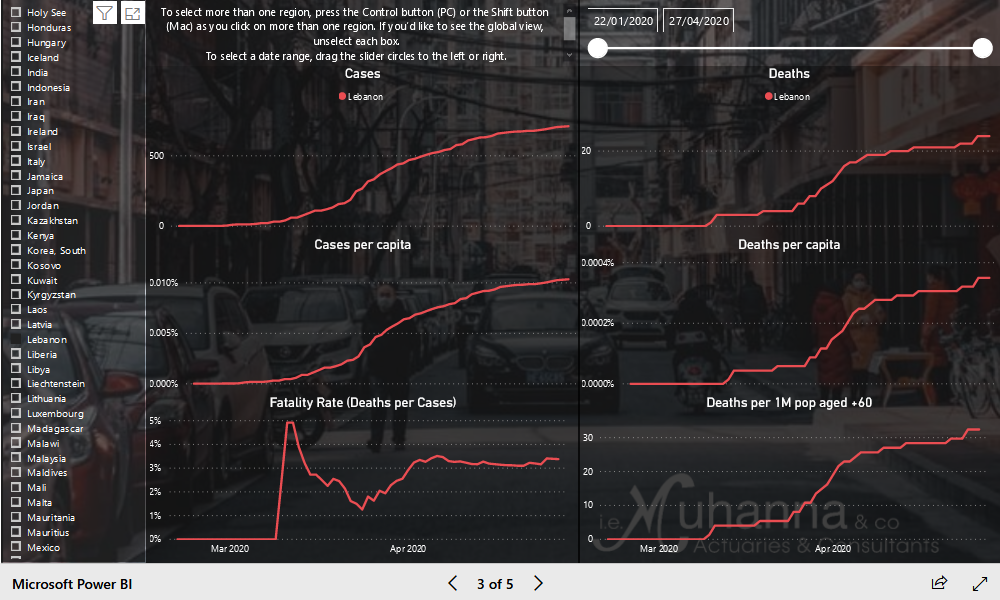

i.e. Muhanna & co COVID-19 data analysis tool

Part of a growing scene of coronavirus visualizations and tracking tools created in intellectual hubs around the world, a research tool developed by Lebanon-based actuarial firm i.e. Muhanna & co looks at the coronavirus impact through the lens of social policy-making.

Analyzing 66 days of data in the January to March 2020 period, the actuarial firm first released a policy note in early April to show that four research variables—confirmed infections, nominal GDP per capita, total number of hospital beds per 1,000 inhabitants, and age structure of the population—all had significant impacts on the development of country-specific trajectories of mortality rates connected to the COVID-19 disease.

Upon encountering follow-up inquiries from clients, the firm subsequently made the tool accessible on its website to interested researchers and the general public, to enable analysis by region, age group, health sector capacity, and the economic condition of individual countries or country groupings.

According to Ibrahim Muhanna, the founder and CEO of i.e. Muhanna & co, the firm’s actuaries and data experts invested more than 100 hours of pro-bono work in development of the tool and initially published the policy note on their findings to open the eyes of policy-makers to the correlations of different factors that can help in decision-making during the coronavirus crisis.

Reliance on numbers is very dangerous when driven by only one pertinent angle among several, Muhanna pointed out, such as lockdown or social distancing policy decisions made irrespective of national specificities in countries with very young populations and large informal sectors where up to 80 percent of working people survive on daily incomes. “Are policy-makers trying to save lives at the expense of killing the economy?” he asks. “What is the right balance? We found interesting correlations looking at the health sector, the economy, and the age [structures] of countries and observed moving trends.”

As the early April policy note observed: “Simple cross-country regressions show that, all other things being equal, death rates decline with the level of GDP per capita and the number of [hospital] beds per capita and increase as a function of the average age of the population.” It confirmed the strong correlation between new infections and mortality rates, which makes the number of infections per capita the main predictor for the observed number of deaths and controlling the number of cases the main instrument by which countries can reduce the future number of deaths, but followed this observation by warning that, “Because policies that control the number of cases – social distancing – also have impact on jobs and labor productivity, the optimal [strategy] might not be to suppress the virus but to mitigate the contagion.”

According to the policy note, 4.6 billion people, or 62 percent of the world population live in countries where the median/average age is in two age brackets between 30 and 39 years but lockdown decisions are heavily influenced by countries with a high share of people above 60. Countries where the average age is higher by five years see additional 3.5 deaths per one million inhabitants, Muhanna tells Executive. This group of 37 countries with average age above 40, which has an aggregate population of 821 million (11 percent of world population), is driving policy decisions on coronavirus together with China (a country in the 35-39 bracket for average age), whereas global coronavirus policy trends appear to not at all be driven by countries with average populations aged 20 to 29 years or even less, which are 50 plus countries in Africa and South America.

The tool that facilitates analysis of coronavirus trends with actuarial techniques is updated continually and has been made freely accessible here (but is best accessed in desktop environments).

Under pressure

In a picture that is getting increasingly complicated, insurers in recent weeks have been facing mounting pressures—up to the level of American presidential pressures—that they should honor claims irrespective of their validity under existing policy stipulations. At the same time insurers were operating in environments that led several providers to support emergency workers by giving them privileged protections and also issue rebates on motor insurance premiums in lockdown periods. On the other hand, windfalls were pocketed by health insurers due to reduced numbers of elective surgeries, not to mention that the expectations regarding reinsurance are of protracted legal disputes over the coverage of non-life claims that are part of recession events.

In business concepts of insurance, the downside question is how badly the industry will be impacted and driven down by weakened financial markets and elevated losses in multiple lines from life, health, and pension insurance to general lines including business interruption, workmen’s compensation, credit, liability, and specialized lines. As far as the upside, the question is if and how profitably insurance companies will be performing as high-power players in the rescue and resuscitation of the global economy.

In considering these polar questions, one can disagree if the insurance industry is systemically important for the function of the long-term financial system of a capitalist society. Or, when taking account of insurance stereotypes and thinking in terms of urban dictionary-type utility, one can wonder if insurance is just boring and thus superfluous for society, or if it is boring on the surface and sexy beneath—like the proverbial accountant or librarian whose hunky or voluptuous qualities are very well concealed.

For more serious aficionados of the purpose of insurance, a reasonable assumption globally might be that the coronavirus crisis and deep worldwide recession will add to already existing pressures. These business-revolutionary pressures have been building throughout the last ten to 15 years toward reinventing the way in which this industry addresses digitally enabled economies, how it responds to changing behaviors of millennial generations in terms of things such as personal mobility and the sharing economy, and to new cyber risks. Insurance companies’ recent behaviors during the crisis in this sense have been hinting at changes in the sector’s culture and need for further changes.

The prospects of changes in international insurance culture notwithstanding, it is an unanswered and unanswerable question if such a hoped-for global insurance revolution and adoption of socially more harmonious modes of operations would infuse new life into the Lebanese insurance sector. In the past 20 years, the local culture in insurance was more neighborly than if it was solely determined by paradigms from international markets but the sector was also marked by less innovativeness than one would expect, given the quality of insurance talents in the country. However, ignition of digitally innovative thinking and alignment with a reborn global insurance culture is, in any case, not an immediate concern that Lebanese insurers can afford to ponder. The challenges of demand destruction and the immediate to mid-term financial future are much more pertinent concerns on the tables in the approximately 50 corner offices and boardrooms of Lebanon-based insurers.

To give an example, the country’s sole specialized insurance provider for trade credit insurance, LCI, is by default on the daily pulse beats of trade and also an operator of an insurance line that is highly sensitive to local and international fluctuations in the real economy. As CEO Karim Nasrallah confides, LCI took drastic measures already in October and November of 2019 because of the erupting economic crisis. These measures proved efficient for the situation but will not provide indefinite relief. “We took very drastic measures in terms of lowering exposures, cutting down on risks, and not taking on new business,” Nasrallah tells Executive. “Our business is also sharply down because it is based on sales by our customers. Thus in our Lebanese operations, we are working on a very, very slow pace. As you can imagine, this will trigger many payment defaults and issues, which are still manageable but we will have a big problem in the market here if the situation gets stuck for a long time.”

Like every business leader that Executive communicated with in the past six weeks, Nasrallah sees the dual economic and coronavirus crisis as a very heavy burden on Lebanon. The crisis massively includes the insurance sector and is in urgent need of a sustainable solution. “As a country, we are very much exposed; we have to hope for the best,” he says.

In the description of acting insurance commissioner Nadine Habbal, some immediate problems of the Lebanese insurance sector are being addressed, specifically the challenges which sector companies face with regard to executing international transactions for payments of their quarterly reinsurance dues. However, longer term issues such as the implementation of the upcoming IFRS 17 regulation, will require large investments in the sector and mandate massive consolidation of the overpopulated provider field, she tells Executive.

Due to the implications of the much debated haircut in the Lebanese banking sector, the highly banking-exposed insurance companies already face near-term prospects of asset write downs, says Lebanese actuary Ibrahim Muhanna (see Q&A). He explains that in a pessimistic scenario, the shareholders’ equity of up to 17 insurance companies would be completely depleted if insurers’ assets in the banking sector would be subjected to a 50 percent haircut on large deposits. Another 31 companies would maintain positive shareholders’ equity but would need to inject further capital, especially if they write long-term business.

Moreover, associated liabilities of insurance companies will have to be revalued in light of the new economic circumstances in Lebanon, which could leave some companies with increased liabilities and others with decreases, in addition to spelling bad news for small life insurance policyholders. “Insurers’ total earmarked assets for unit-linked life policies amount to around $700 million which match the companies’ associated liabilities,” Muhanna says. “Therefore the tens of thousands holders of these policies will be taking all the hit that comes as a consequence of any implemented haircut … In short, I expect a massive impact on the insurance sector in Lebanon and a large role for risk professionals and actuaries to play as they help navigate the upcoming systemic shocks.”

There is, in sum total of the accounting of the coronavirus crisis impact on insurance from a Lebanese vantage point, absolutely no certainty about the future incarnations of global insurance culture and still less certainty on the local market question how many insurance companies will still be active one year onward from what one might call the great Lebanese crisis of coronavirus, everything economic, and politics. Also the question how the local provider landscape will be composed and oriented in terms of companies that are independent local, bank-affiliate, or units of international firms, will only be answered with time.

However, a very pertinent question remains with view to the culmination of the coronavirus and economic crisis in Lebanon and elsewhere: Can insurance wisdom and actuarial risk assessment provide value to countries that are deciding on their path out of their respective medical and economic crisis scenarios? (See box above). As the ICC’s Habbal noted in a conversation with Executive, each country has a specificity that must be properly understood and addressed if the aim is to reach an optimum path of sustainability.

It emerged, as a generally agreed upon perspective during the coronavirus crisis, that lives count more than money. While, as IMF head economist Gita Gopinath noted in April, “there is no trade-off between saving lives and saving livelihoods” in the sense that countries need to enable health systems to cope with the disease as condition upon which resumption of economic activity can occur, however, countries also can ill afford to have their economies die and kill scores of people in the process while enterprises are waiting for the virus to be controlled.

This means that careful, balanced, and constructive navigation of the coronavirus crisis’ medical and economic cliffs is essential. As economic cliffs may loom very large in countries with overwhelmingly young populations and large informality in the economy, there may be urgent needs for immediate income as well as productivity gains. Such economically needy societies are not found in old Europe or among the two largest economies on planet earth, but they exist in places like Africa and South America—and, with a unique other specificity, in Lebanon. Adequately addressing these nations’ specificities and needs for recovery and new growth will need a lot of investment money, probably debt forgiveness too, but much more than that: smart policies, accountable politicians, and custom-tailored coronavirus solutions.