The subprime problem is now snowballing into a global recession. Banks are hesitant to even lend to each other. Central bankers are panicking. Yet the prospects for private equity in the Middle East and North Africa (MENA) region remain bright, despite increasing challenges.

The next few months will be difficult for all financial players, including private equity companies operating in MENA. However, economic fundamentals remain strong and are supported by aggressive fiscal policies and high oil prices. Governments’ reserves will continue to trickle down to the rest of the economy — sustaining corporate profits and public investments. A sober market will offer better valuations, and hence better returns for private equity. Although the increased attention the region enjoyed in 2007 may be disrupted, we expect such disruption to be temporary. In fact, the robust economic performance of the region is likely to attract additional interest from international institutional investors over the medium term.

The take-off of PE

Starting 2002, oil prices began their continuous climb from $20/barrel, rising around 30-40% annually. Liquidity from petrodollars was compounded by the repatriation of capital from the west following the 9/11 events. The excess capital was first directed toward the capital markets, which appreciated 100% annually between 2003 and 2005. Liquidity then filtered into real estate, which in the past few years witnessed a flood of announced mega real-estate projects (for example, the Palm, DubaiLand and King Abdullah Economic City). In 2005, some of the excess liquidity moved into private equity, jump starting the industry.

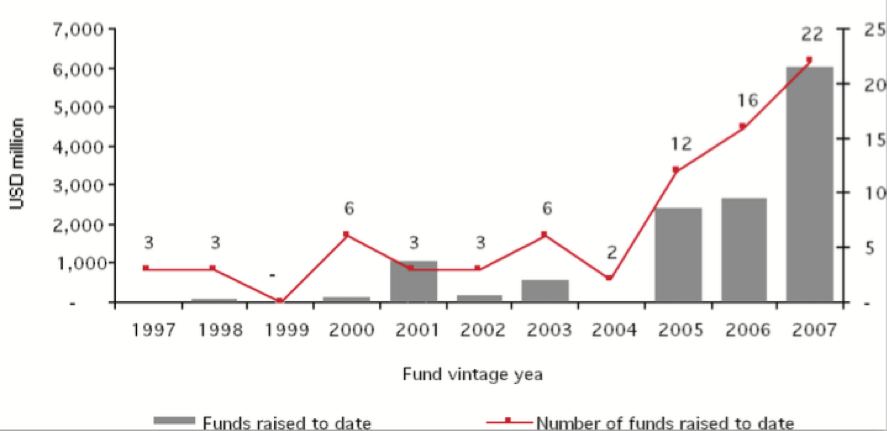

Private equity funds closed over the last decade

The PE industry in the GCC in particular and the MENA region in general ended 2005 with a record number of PE funds launched and announcements made. Over 12 funds with a total of around $3 billion of commitments started their operations in that year. International PE funds, including The Carlyle Group, 3i, and CVC, for the first time started to look for deal flow from the Middle East after having considered the region solely as a source of limited partners in the past.

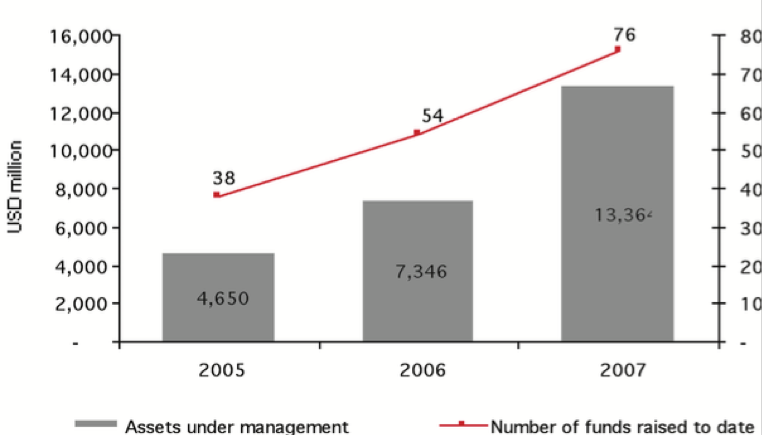

Since then, the industry never looked backed. By the end of 2007, funds under management in MENA increased to 76 funds managing $13 billion. This sudden take-off can be attributed to many factors within the context of the global prominence of PE as an investment class. Economic growth, high oil prices, increasing economic liberalization, reduced restrictions on foreign investment, privatization of state-owned assets, and greater liquidity of regional stock markets have all been put forward as stimuli for the impressive growth of PE in the GCC.

Private equity funds (cumulatively) over the last decade

Fuelled by the increasing oil prices and production, GCC economies have witnessed stellar growth in the past three years. Future economic growth is expected to be maintained in the short and medium terms and to surpass global economic growth of 5%. Aggressive fiscal policies and economic restructuring by the GCC governments will ensure that growth in the non-oil sector will be over 5% and relatively isolated from the volatility of oil prices.

Despite the windfall from higher oil revenues, the GCC governments have started selling state owned assets at an increasing rate. This is in light of the increasing economic benefits from private sector management which have led the governments to restructure their economies during a period in which a favorable environment exists. Airlines, power stations, desalination plants, industrial assets, postal services, banks, stock exchanges, telecom operators, and ports are some of the assets that have been or will be sold to the private sector either partially or fully. The value of the assets in all GCC privatization programs is in the hundreds of billions, and some estimates put it as high as $1 trillion.

Within this positive environment, the PE industry has risen quickly in the GCC. Not only is it viewed as an outperforming investment class, but also more importantly, governments and economists are preaching its positive role in developing the private sector and creating strong, globally competitive local corporations. Whenever an investment by a PE fund is announced, the local media has consistently praised the announcement.

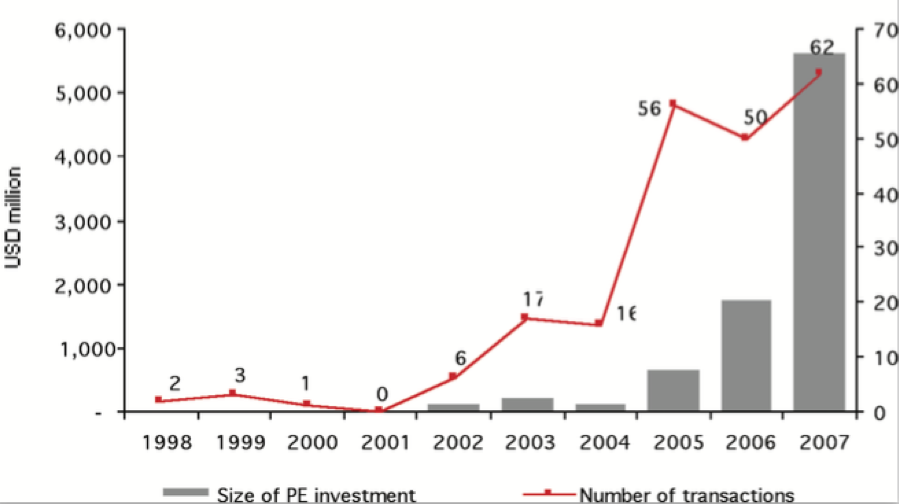

Industry experts keep on reiterating whether the industry has grown too fast on the back of the excess liquidity. Although the value of investments has risen considerably in 2007, the number of transactions has stagnated to an extent. Moreover, the largest three transactions have been all in Egypt, whilst the GCC has only witnessed transactions mostly smaller than $100 million, as the flow of privatization transactions in the GCC has not yet materialized.

Private equity investments between 1998 & 2007

The quality of deal flow continues to improve, influenced by favorable macroeconomic factors. Corporate Arabia profitability is increasing steadily, and this will create bigger companies that will sooner or later need serious capital injection to maintain their growth trajectory. Banks reluctance to extend additional lending against a backdrop of a global credit crunch will also increase the chances of opening capital to private equity funds.

Egypt has emerged as the leading destination for private equity money in 2006/2007. The size of the Egyptian economy, its need for capital, and the government’s liberal policies have all contributed to Egypt’s attractiveness. The UAE, traditionally the leading destination, remained at No 2. Saudi Arabia is rapidly increasing its share, albeit from a lower base. Jordan has also maintained its attractiveness at the 4th position, despite the small size of its economy.

It is interesting to note how sensitive private equity money is to macroeconomic policies. Countries like Kuwait — third largest economy in the GCC — attracted less investments that Jordan — fifth the size of Kuwait’s economy. Saudi Arabia share of private equity investments increased only after government policies became more investment-friendly. The PE industry quickly completed the investment cycle, and the number of exits soared in value in 2007 to more than $1.5 billion. The IRRs achieved by these exits have ranged between 31% and 348%, very healthy returns for a nascent industry.

Exits were split between IPOs, trade sale, and financial sales. Despite the robust activity in the IPO market, IPOs as an exit route are decreasing in importance as trade and financial buyers are becoming more active. Naturally, private equity players find trade and financial sales less complicated, and hence, are exploring such exit routes more aggressively than before.

Challenges and trends facing the PE industry in GCC

Robustness of economic growth: As the subprime crisis snowballs in 2008 into a global economic slowdown (or recession), the impact of such a negative turnaround in the world’s economy on growth in the GCC cannot be clearly assessed. However, it is expected that the GCC will be one of the least affected regions given the huge reserves supporting an aggressive fiscal policy. Nevertheless, the next few months will be difficult for all financial players.

Entry of international players: The previously timid interest of international players in the region was suddenly emboldened when The Carlyle Group announced its plans to raise a MENA fund for up to $750 million by 2008. The Carlyle Group is following the footsteps of many international players, like 3i, TPG, Deutsche Bank, Credit Suisse, CVC, Ripplewood, HSBC, and EMP. The entry of The Carlyle Group will definitely entice many other global heavyweights to establish funds for the region. The GCC is a region they cannot ignore, particularly as many of their LPs are keen to see their money invested locally.

Larger funds: The PE industry surpassed the $100 million per fund milestone in 2003, the $500 million in 2005, and the $1 billion in 2006.

Track record: As regional fund managers start exiting their investments, their track record is being established — in most cases showing 30% plus net returns. The window of opportunity for new fund managers is starting to close, and 2007 has seen some fund raising efforts being aborted.

Deal flow: Business and social habits, limited opportunities in the private sector, and delayed privatization programs have made good deals hard to come by. Proprietary access and extensive deep business networks are essential for succeeding in the region. Regional dynamics have not allowed intermediaries to play a significant role in maturing deal flow, and hence made deal sourcing process a competitive edge for some and a frustrating issue for others.

Imad Ghandour is the director of Gulf Venture Capital Association.