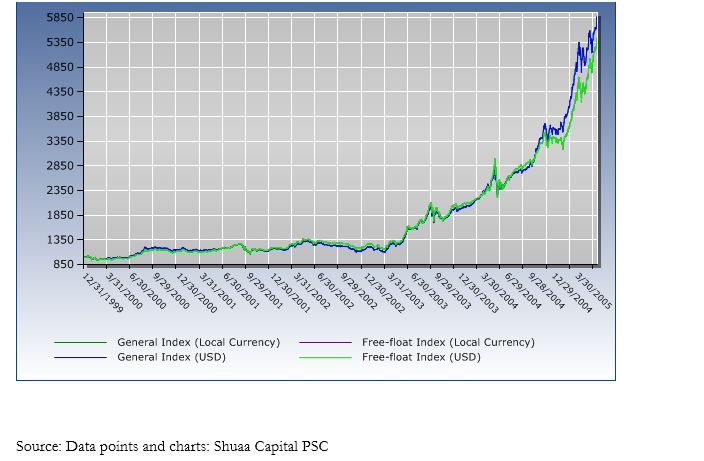

A most fundamental characteristic of speculative gain is that it goes away as smoothly as it comes. So whenever it’s very easy to make money, one must be reconciled to the possibility that it can be lost without much effort or notice. Nowhere is this truer today than in the Gulf stock markets. For just over two years, while most global markets have been mired in single digit action and the tensions in Iraq continued, very few would have bet on a massive rise in the fairly underdeveloped markets of the Gulf. Yet, this is exactly what has occurred. The stock markets of the region have witnessed staggering rises, bringing with them a whole slew of new issues. What fueled the rise and what lies ahead?

The simple truth about Gulf stock markets is that oil has gone from below $10 per barrel in the last couple of years of the 20th century to near $60 per barrel today. This has created a tidal wave of petrodollar-driven liquidity in the coffers of Gulf governments. A recent study by Saudi Arabian Monetary Agency (SAMA) reinforces this notion. The premise of the report shows how domestic spending of “high-powered money” (net domestic expenditure from oil revenues) can create liquidity several times its size (the multiplier effect), demonstrating that, in Saudi Arabia, each new oil riyal of government spending has the power to create up to SAR 16.6, or over sixteen times in additional liquidity. Between 2002 and 2004, net government spending totaled approximately SAR 575 billion, which have had the potential to generate new liquidity up to SAR 10 trillion.

When analyzing this precept, it becomes more comprehendible why GCC markets have spearheaded the world in terms of market growth. Liquidity injected into value creating businesses will raise values in the long term but in the short term inflates and accentuates stock prices.

This scenario has been replayed in the UAE, Saudi, and Qatar. But what stands to be the determinant of how market value will adjust lies in the sustainability of earnings growth, which is set to be put to test in the third and forth quarters of 2005.

As the post 9/11 environment dictated less investments abroad and more cash staying in the region, investors, both sophisticates and neophytes, rushed into stocks. Institutions were only happy to oblige by floating a staggering number of companies. It would be too complex to review the suitability of all Initial Public Offerings (IPOs), suffice it to say that not all the companies that went public would have passed the scrutiny in a more mature market, such as Europe.

The move up in the Gulf IPOs started to resemble, in many aspects the Nasdaq mania of the year 2000, prior to the crash. Shares would double and even triple in the days following the float, and soon, everyone wanted in on the action, so much so that central banks in the region have had to step up oversight, as many financial institutions began lending to speculators, often with reckless abandon. During the float of a large telecom company for instance, it is said that a couple of mega banks lent billions to its most exclusive clients so they could “play”. This environment has led to overvalued markets, trading at well above their acceptable valuation parameters, and pricing themselves in what will eventually prove to be unrealistically ambitious expectations.

These expectations were further boosted by solid earnings growth by listed companies of over 40% in 2004 with even more robust figures for the first quarter of 2005. Still, a few shady outfits which have found their way on to the public market are trading at 500 times actual earnings. The UAE market, for instance, has gained 86 per cent so far this year. There are, however, question marks over its sustainability and it has been particularly exacerbated by violations in the primary market. Market observers have described the extent of over subscriptions in the local IPOs as “obscene,” prompting the Central Bank to act with unprecedented toughness.

In the case of the record-breaking Aabar petroleum IPO, the total cost per share was Dh5, out of which only one dirham went to the issuing company while Dh4 each was pocketed by the banks that financed the stock applications. This is quite unnatural by any standards. Although markets are generally irrational, they do have checks and balances that ultimately correct blatantly unnatural tendencies. It seems the time has come for these resistance mechanisms to come into play. There are already signs that the party in the stock market may be winding up. A four-day correction on the UAE stock exchange last month wiped off 13 per cent of the market value in one stretch.

There is almost too much public excitement and participation, and this creates a bubble environment. Many newcomers to the “game” will still crow that there is easy money to be made in the area. This attitude is a sure sign that at least some Gulf stock markets are entering bubble zone. There simply isn’t enough institutional money in the form of pension funds and the like, as is the case in developed markets, to sustain them in the medium-to-long term.

The Gulf markets have two major problems in my opinion. One is that they are too dependent on one commodity: oil. The other is that the fundamentals, especially in Saudi, are well behind the market euphoria. Whereas disposable incomes, on aggregate, are rising in the UAE, they are near $25,000/capita, they are stagnant in other countries. Saudi, in part due to Saddam, has seen its per capita income drop to $10,000. So there is not, as in Europe and Asia a well-developed Equity Culture, it is mainly, for now a speculative arena.

The growth in the Gulf is also too closely tied to oil, and while Saudi Arabia has made great progress in solidifying its non-oil activity, it is still mainly a one horse race. This poses great risks if the global economy, especially China decelerates, and oil crashes back into the $25-30 per barrel range, as stock markets will suffer greatly. The two most obvious factors in play in Gulf markets today, and the two most regularly cited as being the main driving forces behind the three-year rally in stock prices, are high oil prices, and low interest rates. The prolonged incidence of both factors has had a magnified effect on equity markets of the region, and is currently most pronounced in the markets of the UAE and Saudi Arabia.

The two seem to have priced in the permanence of both factors. A marked reversal of either one or both those factors would almost definitely have an adverse effect on the markets. In fact, interest rates today are no longer abnormally low, as they have tripled from their all time lows, and are higher today than their pre-9/11 levels. They are generally expected to gain a further percentage point by current year-end. This fact has yet to be reflected in the two markets. Oil prices on the other remain buoyant, although they have recently come down from their peak in April. The direction that oil prices may take from here is harder to predict, and analysts are mixed in their expectations. If the more pessimistic of them are proven right, then a steep correction may prove inevitable. The medium-term direction of interest rates is a foregone conclusion. Keep your eyes on oil.

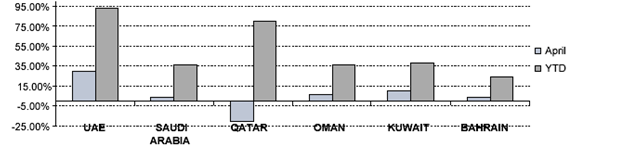

All in all, the easy money has been made, as one can see in thee accompanying tables. Although the gradual development of capital markets will bring great benefits to the entire GCC area, they are currently in boogie-wonderland in terms of both valuation and excess public enthusiasm with a recent issue – are you sitting down? – 800 times over subscribed. There is too much money flowing into too few shares. With Kuwait’s infamous Souk Al Manakh crash and its consequences still not wiped off memory, investors can hardly be at ease with the current exuberance in the market. Watch out.

Returns: Year to Date, and April 2005 alone.

Saudi Arabia alone looks like mania waiting to deflate…