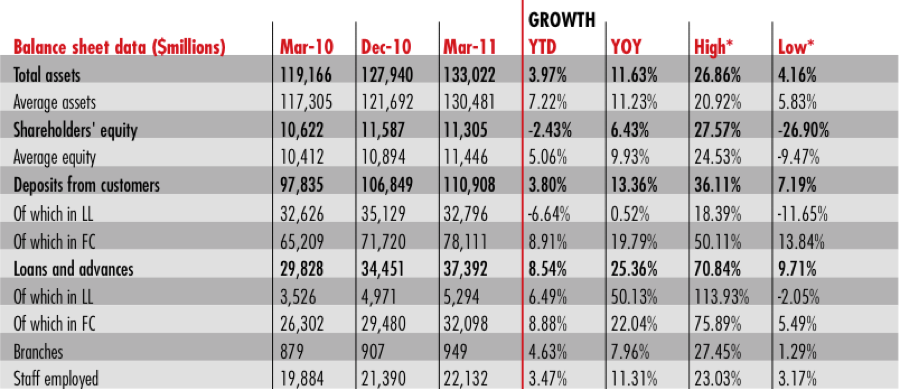

Lebanese banks have shown resilient results amid the relatively tough operating environment that characterized the first quarter of 2011. The ‘Alpha Report’ — a detailed performance synopsis of the top 12 Lebanese banks, issued by Bankdata Financial Services — showed that total assets grew by almost 4 percent over the quarter and 11.6 percent year-on-year (YoY). In parallel, customer deposits grew 3.8 percent over the quarter and 13.4 percent YoY, representing a sustained healthy performance although at a lower pace than had been registered over the past couple of years. Evidently, given the market pressures at the beginning of the year, the rise was almost fully accounted for by foreign currency components.

The most significant development of the quarter rests in the 8.5 percent growth in loans over the quarter and 25.4 percent YoY. This bears witness to the continuing lending activity of Lebanese banks benefiting from strong liquidity levels, in addition to the success of the central bank’s initiatives encouraging lending in Lebanese lira (LL). The latter grew twice as much YoY as loans in foreign currencies, at 50.1 percent and 22 percent respectively. Consequently, loans to deposits rose to a record high of 33.7 percent. Loans to deposits in LL continued their ascending path to reach 16.1 percent in March 2011, while loans to deposits in foreign currencies registered 41.1 percent.

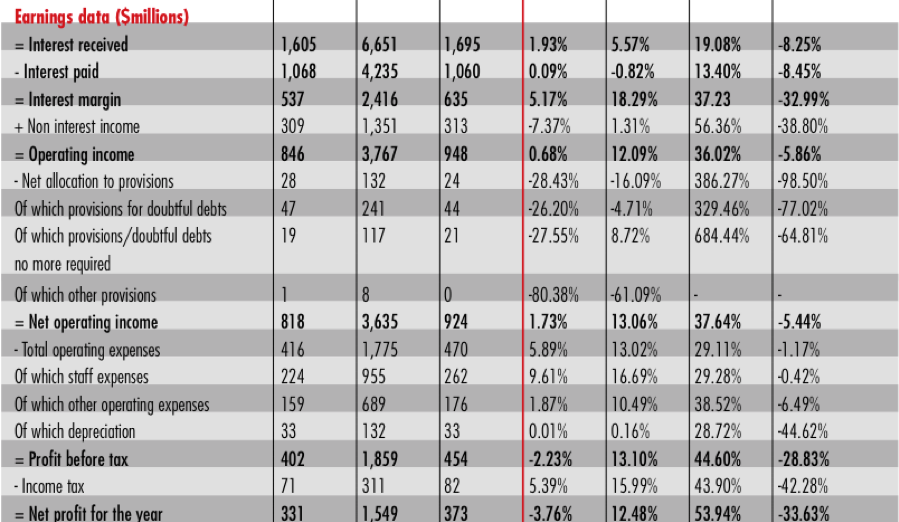

The rise in bank lending contributed to the improvement of bank spreads by 12 basis points YoY, despite a slight drop of 4 basis points compared to year-end 2010. In fact, banks’ interest margin reported a rise of 18.3 percent YoY driven by both volume and price effects. In parallel, net allocations to provisions decreased by 16.1 percent YoY. The outcome was a sustained improvement in banks’ net operating income (13.1 percent YoY). The mild growth in non-interest income (1.3 percent) reflects the slowing economic conditions, as non-interest income is a reflection of aggregate spending in the economy.

Alpha banks pursued their firm cost control policies in the first quarter, restricting the rise in total operating expenses to 13 percent YoY and aiming at flat growth in this item in full-year 2011. Meanwhile, cost to income rose to 49.6 percent, similar to the ratio of December 2009, and up from its record low of 47.1 percent at year-end 2010. This rise was triggered by 42 new branch openings over the quarter, and a corollary rise in the number of staff by 742 employees since the beginning of the year.

As a result, banks’ net profits grew by 12.5 percent YoY, in line with the growth registered in their activity base. Consequently, both net return on average assets and on average equity were stable YoY (1.14 percent and 12.41 percent respectively).

It is worth noting that the first of the year is generally a slower quarter and as such, the performance confirms the capacity of Lebanese banks to manage the adverse impact of decreasing foreign and local interest rates and a troubled political and economic context. The positive results of Lebanese banks despite tough operating conditions bears witness to a new episode of resilience of Lebanon’s banking sector.

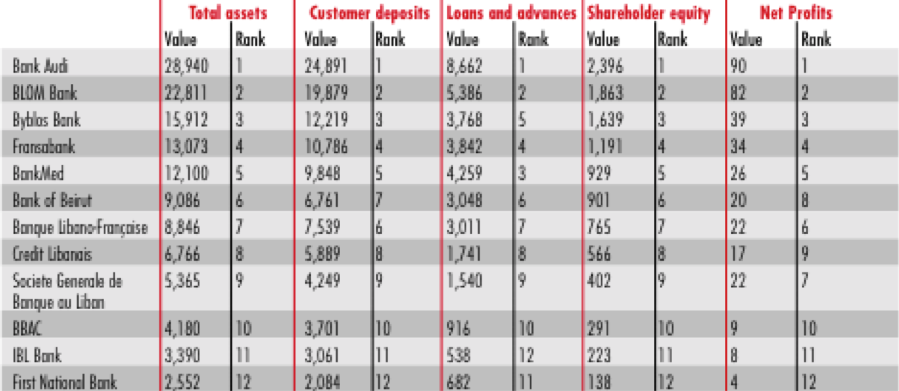

The ranking of alpha banks by assets, deposits, equity, loans and net profits in March 2011 showed that Bank Audi ranked first in all criteria followed by BLOM Bank, while Byblos Bank ranked third.

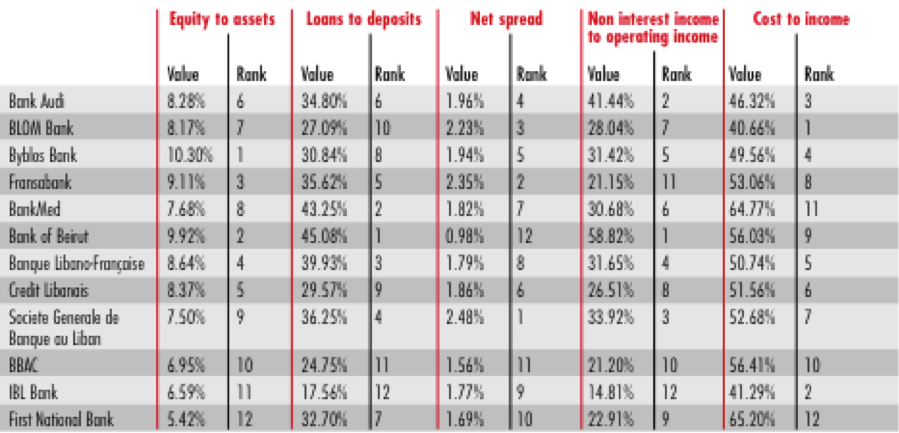

Finally, the ranking of alpha banks as per major financial ratios reveals that Byblos Bank ranked first in terms of capitalization (equity to assets ratio), while Bank of Beirut ranked first in terms of loans to deposits ratio and Société Générale de Banque au Liban (SGBL) ranked first in terms of net spread.

With respect to the ranking by non-interest income to operating income ratio, Bank of Beirut ranked first, whereas BLOM Bank ranked first in terms of efficiency (cost to income ratio). The following pages show the ranking of the 12 alpha banks according to major financial aggregates and financial ratios as of March 2011.

Consolidated balance sheet of Alpha group

*Refers to the superlative performing banks from within the group

Alpha banks ranking by aggregates as of March 2011 ($millions)*

*The Alpha group of 13 banks with deposits above $2 billion was recently reduced to 12 banks further to the upcoming merger/acquisition of Lebanese Canadian Bank by Société Générale de Banque au Liban (SGBL).