Basel III and you

On September 12, central bank governors along with the 27 bank regulators on the Basel committee finalized the draft of the long-awaited Basel III regulations on bank capitalization. The rules are meant to better fortify banks against a financial crash so that they may survive crisis without government support. The regulations contain the following requirements:

- Raise tier one capital from 4 percent to 6 percent by 2015.

- Maintain a capitalization buffer of 2.5 percent by January 2016, with the penalty for noncompliance being restrictions by regulators on payouts such as dividends, share buybacks and bonuses.

- Maintain common equity or loss-preventing capital buffer of 2.5 percent as soon as possible.

- Define tier one capital as mainly common equity and retained earnings — deferred tax assets, mortgage-servicing rights and investments in financial institutions may be counted no more than 15 percent of the common equity component.

- Cap overall leverage based on standards of each country.

- Set common liquidity requirements for first time ever, mostly comprising sovereign debt.

Following the announcement, several regional central banks expressed their compliance with the regulations, which will be voted upon at the G-20 meeting in November. Speaking about Lebanon’s preparedness to meet the regulations, Riad Salameh, governor of Banque du Liban, Lebanon’s central bank, said in a September 27 speech at the Standard Chartered Thought Leadership Bankers’ Conference: “Our banks have an average [tier one capital] ratio of over 6 percent. And therefore meeting the 7 percent [requirement] into the coming four to seven years as scheduled by Basel III. It is not going to be a problem for our banking sector.”

US probes Mideast money moves

A United States government investigation into possible money laundering between US and regional institutions began on September 27 in the US House of Representatives in a hearing entitled “A review of current and evolving trends in terrorism financing.” The House Committee on Financial Services will be investigating the movement of $1 trillion between institutions in the Middle East and the US taking place of the last six years. Financial institutions connected with the al-Gosaibi family will be included in the investigations as well as elements of the Saad Group, both of which defaulted on their debt last year and have been enmeshed in claims of fraud and theft against one another, according to The National. Bank of America is the only US institution yet to be mentioned as included in the inquiry. The bank is thought to have been the facilitator of transfers between the al-Gosaibi family and Maan al-Sanea of Saad. Judges in both the US and the Cayman Islands have ruled that the disputes between the two parties must be resolved in Saudi Arabia. But this hearing could result in a US Justice Department investigation into transactions between the two. A source close to the al-Gosaibi family told The National: “In this investigation there will be three big questions: Where did the money come from? Where did it go? And where were the red flags? So much money moved through the US financial system from the Middle East and no one took any notice.”

Lebanon fuzzy on Iran sanctions

Conflicting information about statements made by Riad Salameh, governor of Banque du Liban (BDL), Lebanon’s central bank, regarding the most recent sanctions against Iran circulated through various media outlets last month. On September 7, Salameh told Bloomberg that “it is up to the Lebanese banks to act in accordance with their interests and be sure, if they have to make an operation, that it’s an operation that can’t be contested internationally.” He continued to say that the latest UN resolution “is very clear and we will respect it and make sure it is respected.” This contradicts a September 26 report from the state-owned Iranian IRNA news agency. According to the agency, Salameh told Iranian Ambassador Ghazanfar Roknabadi that BDL has no problem with continuing business between Iranian and Lebanese banks. Currently, Bank Saderat Iran is the only Iranian bank operating in Lebanon. “We welcome business with Iranian financial institutions,” IRNA reported Salameh as saying, with the agency adding that the comment first published by Bloomberg had been “distorted” to say that he was in favor of implementing sanctions when that is not the case.

A better ease of access

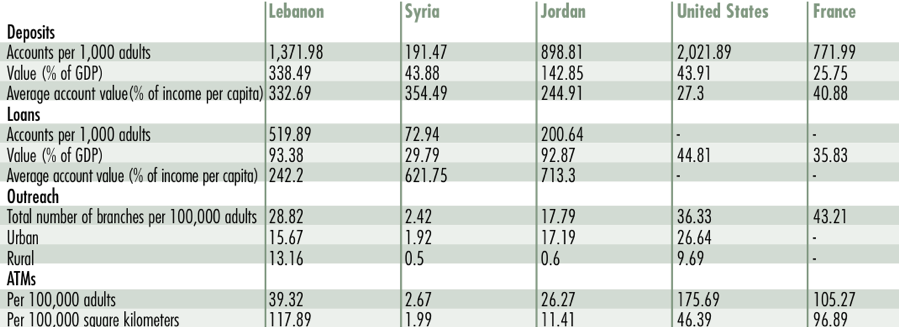

In a World Bank study of access to financial services entitled “Financial Access 2010,” Lebanon ranked highly in most parameters. In depositor accounts per 1,000 adults, Lebanon ranked 36 out of 142 countries studied, with 1,371.98 accounts per 1,000 adults. Deposits to GDP reached a ratio of 338.49 percent. In terms of loans, Lebanon ranked even higher at 17th with 519.89 accounts per 1,000 adults. The report also noted that Lebanon succeeded in 2009 in granting access to finance to small and medium enterprises by implementing consumer protection efforts. Per capita income worldwide saw a decline in 60 percent of the 142 countries covered. Both the deposits to GDP ratio and the loans to GDP ratio also dropped by 12 percent and 15 percent, respectively. The report noted that the number of ATMs has increased across the board due to the replacement of many branch operations with machines as a reaction to the global financial crisis.

Financial access

Dubai’s credit drag

Once a leader in credit growth, Dubai is now accused of being a drag on the credit recovery process of the GCC, according to Adnan Yousif, chairman of the Union of Arab Banks. The banker told The National that Dubai’s credit growth forecast for next year has fallen behind the GCC’s expected 10 percent, with Dubai’s lending growth expected to be 8 percent in 2011. “Dubai cannot grow continually at a fast pace,” Yousif said. “What they achieved in five years in Dubai many countries can only do in 50 years.” Dubai’s spot as number one in the credit race will most likely be taken by Saudi Arabia, where the government is currently planning to spend its way out of the financial crisis with large and expensive infrastructure projects in the works. Dubai’s previously high credit growth rates, such as 44 percent in 2008, are the mark of an immature market and a developing economy. “It will be more mature than the accelerated highs of the past,” said John Tofarides, a banking analyst at Moody’s Investors Service to the newspaper. “It will be naturally below 10 percent.”

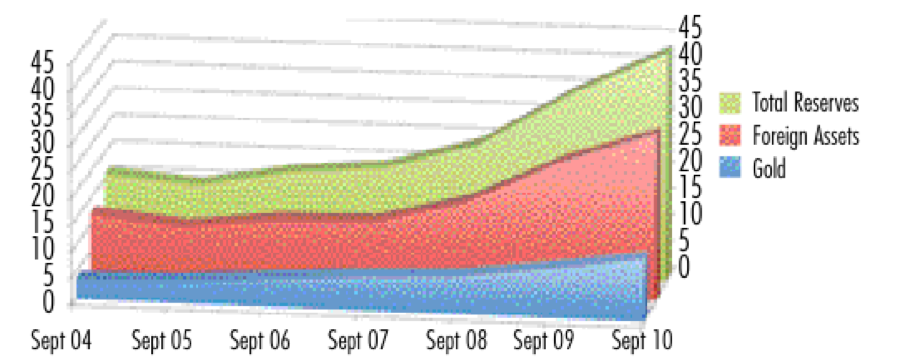

Reserves still climbing

The reserves at Banque du Liban (BDL), Lebanon’s central bank, reached record highs in the first half of September, growing to $43.01 billion, up from $34.72 billion at mid-September last year. This sum is comprised mostly of $31.31 billion in foreign assets, up 22.77 percent from late 2009’s $25.5 billion. Credit Libanais attributes this growth to the increasing preference of Lebanese banking customers for the Lebanese lira, due to attractive interest rates on deposits and most loans, allowing BDL to absorb more US dollar liquidity. Dollarization of deposits in Lebanese banks stood at 62.17 percent at the end of July 2010, down from 65.77 percent one year earlier. The other factor making up the reserves is BDL’s stock of gold, as of mid-September estimated to be worth $11.7 billion, up by 26.93 percent.