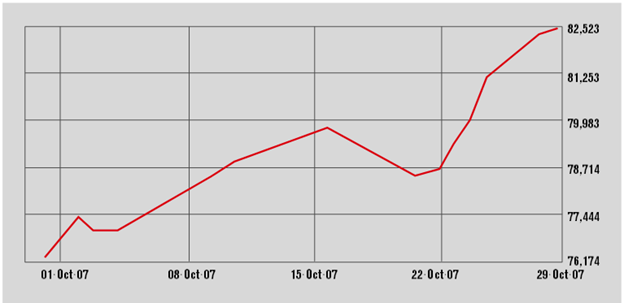

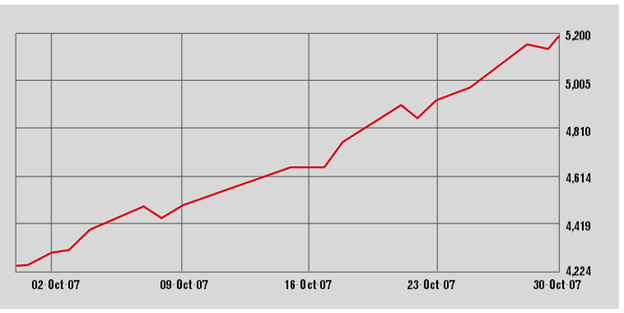

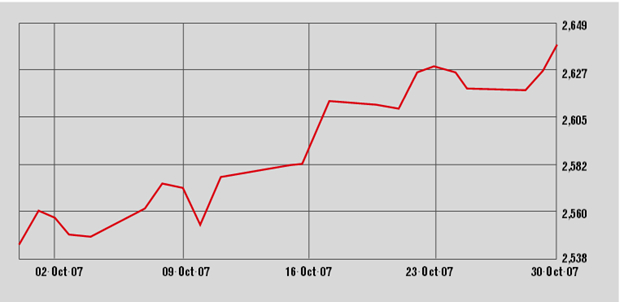

The Beirut Stock Exchange closed its fourth trading week in October with the year’s best index showing as the BLOM stock index reached 1373.636 points on Oct 26. Banking shares were the force behind the upwelling of optimism; the market buzz centered on talk of an acquisition offer for BLOM Bank. The bank’s GDR shares closed at $90.70 on Oct 26, its listed shares at $77.10. Bank Audi also pulled up, its GDRs reached $71.65 and its listed shares, $68. With some hopes emanating from political talks, Solidere also firmed further and closed at around $19 on Oct 26. Total value of shares traded on the BSE in the third quarter of 2007 was $257.4 million. A new run at auctioning two mobile phone operator licenses for the two existing cellular networks is scheduled for February, with distant hopes for broadening the activities on the BSE by listing part of the government’s stakes in the two operators.

Beirut SE: Blom (1 month)

Current Year High: 1,526.31 Current Year Low: 1,168.36

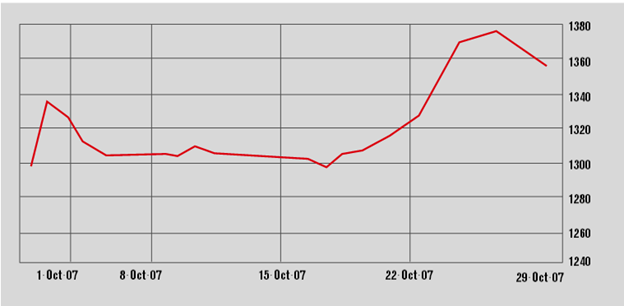

The Amman Stock Exchange was the region’s Ramadan racer. It slowly rose from months of slumber in the mid-5000s at the beginning of the fasting period. In October, the ASE Index pulled up in a steep ascent to close at 6,713.02 points on Oct 25, its 17.3% gain for the month measuring near the top in the MENA region. Arab Bank, the bulky force behind many ASE developments, rallied by 29% between Oct 1 and Oct 25. It was the first time since February that the bank’s stock was quoted above JD 27 ($ 38.14) and the climb came ahead of its quarterly results announcement, in which the bank disclosed a 15.6% increase in net profit for the first nine months of 2007. After banking, the industrial, financial services and insurance sectors moved up on the ASE in the week to Oct 25. Noteworthy in the real estate sector was the IPO announcement by Damac Jordan for Real Estate Development with subscription in late October and early November.

Amman SE (1 month)

Current Year High: 6,764.93 Current Year Low: 5,267.27

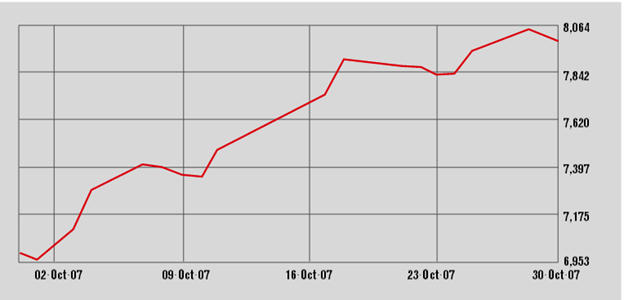

The Abu Dhabi Securities Market displayed an even better mood than the Dubai bourse as far as fasting induced index gains. It soared 12% after Eid to close at 4,269.4 points on Oct 25, bringing its gains for the month to 22.2% and to 42% since the start of 2007. During Ramadan, Abu Dhabi’s key real estate stocks ALDAR and Sorouh set the pace for bullishness on the ADSM but banking and energy values also went strong. Energy company Taqa gained 17% from Oct 1 to Oct 25; banks First Gulf and NBAD moved up 25% each. Etisalat, which traded up just over 25% during the period, attracted attention on rumors that it would open its share ownership to foreign investors but denied late in the month that it would takAbu Dhabi SM (1 month)

Current Year High: 4,291.22 Current Year Low: 2,839.16

Fasting is good for the soul and it also looks to clear the mind with leanings for optimistic investment decisions nowhere in the GCC more than on the UAE bourses. The index moved to 4969.82 points on Oct 25, up about 17% from the first of the month. No more Mr. Sluggish, the Dubai Financial Market appears to have determined in introspection and even the weight of still lackluster Emaar with an unexciting third-quarter profit statement could not hold the DFM down. Between Oct 1 and 25, Deyaar (up 15%), Arabtec (up 22%), Air Arabia (up 24%), DFM Co (up 33%), and Amlak Finance (up 39%) were among the stocks that drove the positive market sentiment. While the end of the month saw some expected profit taking, analysts started talking about the index scaling the 5,000 points and further by end of 2007.

Dubai FM (1 month)

Current Year High: 5,192.29 Current Year Low: 3,658.13

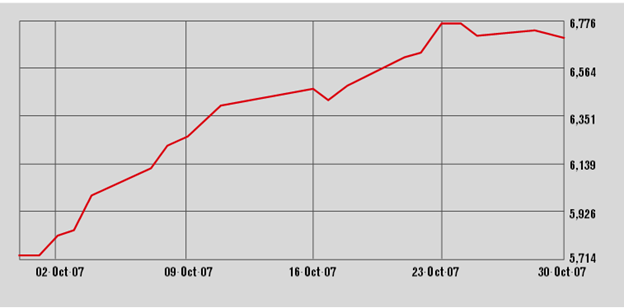

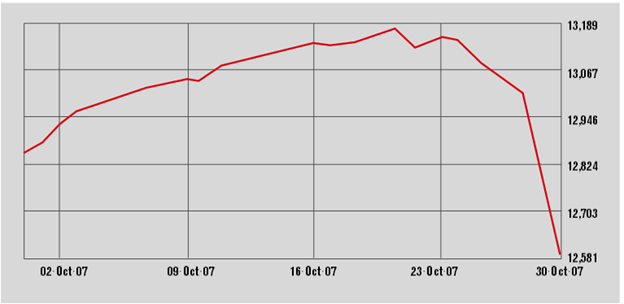

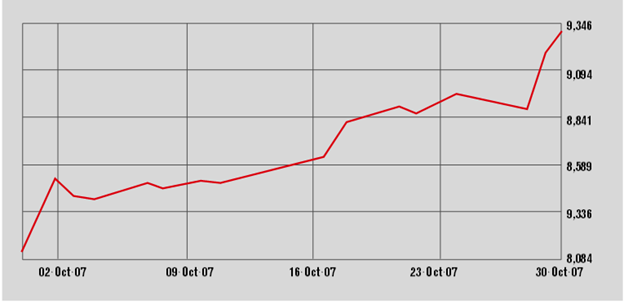

The Kuwait Stock Exchange embraced a new valuation level as its index closed above 13,000 points Oct 7 and stayed in record territory by its close of 13,096.4 points October 25. In peer comparison, however, the KSE paid a modest price for having been the year’s top artist in escaping from the hesitancy that held the UAE and Saudi markets in its grip in the second and third quarters during which the northern exchange soared ahead. In the one-month period from Sep 25 to Oct 25, the KSE index advanced by just under 2% while four of its neighbors took flight with increases above 10%. But since mid-October, the ratio of market cap to GDP in Kuwait exceeds two to one, far above this ratio in other GCC countries. The bourse’s oversight authorities made new attempts at increasing transparency by toughing up regulations in October but the initiative met with a backlash of criticism from major market players. Kuwait’s capital markets draft law is still under discussion in parliamentary committees.

Kuwait SE (1 month)

Current Year High: 13,175.20 Current Year Low: 9,164.30

The Tadawul Index on the Saudi Stock Exchange closed at 8,364.51 points on Oct 27, an improvement of 517 points for the month. In its year-to-date performance, the gap between the SSE and GCC peers last month widened in favor of the latter, however, as the Tasi is trailing neighboring indices by between 12 and 37 percentage points. Analysts named banking and electricity as two sectors that contributed significantly to the subdued development. STC, seen as telecoms underperformer, closed Oct 27 up 4.2% on the month but third-quarter and nine-month results couldn’t impress even as the state-controlled company announced the third 12.5% quarterly dividend for 2007. The SSE led the region as far as time off for the Eid celebrations with closure from Oct 11 until Oct 20 but the exchange used the period to switch to a new trading system with wider capacities that debuted successfully on Oct 21.

Saudi Arabia SE (1 month)

Current Year High: 9,717.89 Current Year Low: 6,861.80

The Muscat Securities Market rose 13.1% in October to a close of 7,942.94, a new record high. The market is up 42.3% since the start of the year. According to research by a Kuwaiti investment firm, the Omani market last month reached a price to earnings ratio of 15.50, behind Kuwait (20.20) and Qatar (19) but ahead of Saudi Arabia (15.40), the UAE (14.60) and Bahrain (13.70). BankMuscat, the sultanate’s largest bank, traded sideways with a 1.3% gain for the month; however, it reported a 40.7% increase in its nine-month profit. Debutant Galfar Engineering shot up 67% in its first two days of trading Oct 24 and 25. Telecoms operator Omantel, for which a partial sale of the government’s 70% stake to a strategic investor is expected in 2008, soared by 43.5% upon news of the planned sale. The UAE’s Etisalat is said to be among the companies interested in the stake.

Muscat SM (1 month)

Current Year High: 8,051.92 Current Year Low: 5,399.29

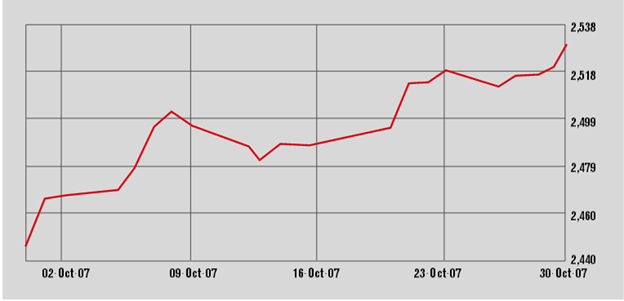

The Bahrain Stock Exchange index closed at 2,615.85 points on Oct 25, its 2.8% rise on the month making it October’s second slowest index gainer after the Kuwaiti bourse and, after it was overtaken by the Dubai Financial Market, dropped to being the year’s second worst performer after the Saudi Stock Exchange. Banking stock played a mixed role, with a diverse showing of positive and negative profit growth in the third quarter. Gulf Finance House, which showed a 49.4% improvement in third-quarter profit, rose 12% from Oct 1 to Oct 25. Bank of Bahrain and Kuwait, which undertook a 15% rights issue on Oct 16, dropped 12% during the period. Telecoms firm Batelco closed 7% higher compared with the start of the month after retreating from a year high the stock reached on Oct 17. Newcomer Seef Properties, in its third month of trading, climbed 15% in October.

Bahrain SE (1 month)

Current Year High: 2,642.85 Current Year Low: 2,106.70

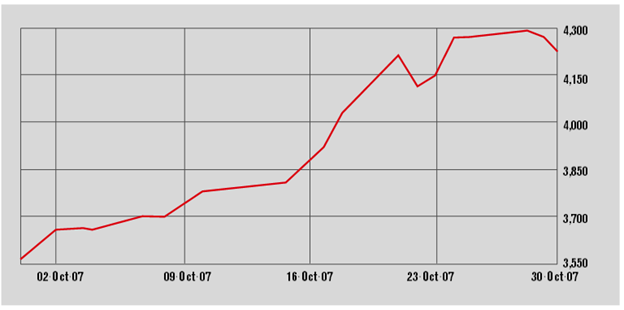

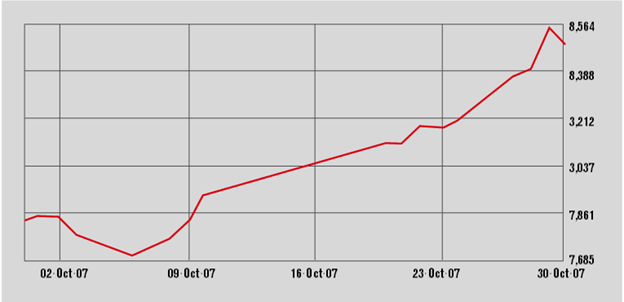

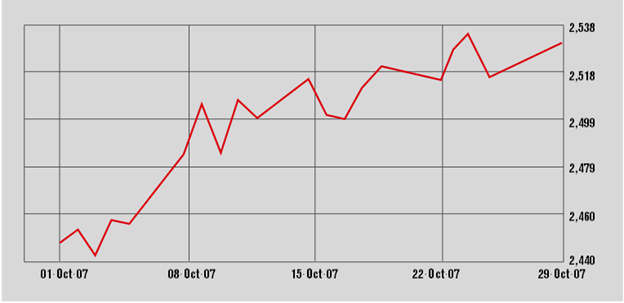

The Doha Securities Market was also in full upswing in October. It started the month with a 200-point jump and closed on Oct 25 at 8,947.7 points, representing a 13.6% index increase over 30 days. Among the winners: Industries Qatar closed Oct 25 up by 17.5% compared with Sep 30; Al Khalij Bank advanced 22%, Rayan Bank 25%. Third quarter earnings were strong to exceptional for a number of companies, including Rayan Bank and also Nakilat which gained 27.5% while Q-Ship traded up 11% but reported a 56% drop in third-quarter profit on Oct 25. Also down in third-quarter profit (by 16%) was Salam International, which had a 22.5% rally till Oct 23 before profit taking set in. A rise of Gulf Warehousing Company stock accelerated after the firm on Oct 17 announced a return to profitability in 2007; the stock doubled in price in October. The DSM became a correspondent member of the World Federation of Exchanges, an international trade organization of securities markets.

Doha SM: Qatar (1 month)

Current Year High: 9,331.88 Current Year Low: 5,825.80

The Tunisian bourse closed at 2,532.49 points October 26, up 2.6% from its index reading of 2,468.27 on October 1. It was 8.64% up from the start of the year. Market heavyweight SFBT advanced over 5% in the course of the month. Banque de Tunisie, the bourse’s number two firm by market cap, gained 4.3% between Oct 1 and its close on Oct 26. Tunisair stayed on a slope and closed the month down by more than 12%.

Tunis SE (1 month)

Current Year High: 2,712.33 Current Year Low: 2,294.38

The Casablanca Exchange stayed its mellowing course with a 2.3% gain to 13,184.17 points on Oct 26. Year-to-date, the index is up 39%. In terms of price to earnings ratios, the Moroccan bourse is in a steam bath with PE of more than 28 times, above Egypt’s 19 times and above anything in the GCC but its protected status continues to be fending off correction impulses. Market aing 21% of total market cap, moved at the rate of the index, while leading bank Attijariwafa Bank closed Oct 26 with a very slight drop when compared with the first of the month. Atlanta Insurance started trading on the exchange Oct 16 aCasablanca SE All Shares (1 month)

Current Year High: 13,506.29 Current Year Low: 8,431.06nd moved from its IPO price of MAD 1,200 ($152.7) the share to MAD 2,078 on October 26.

The Hermes Index of the Cairo & Alexandria Stock Exchanges vaulted over the 80,000 points line late October in post-Ramadan trading and closed at a record 81,062.75 points on Oct 25 on a single day jump by 1,200 points. Between Oct 1 and 25, Suez Cement pushed up 25% to a new year high; financial holding EFG Hermes moved up over 10% to a 17-month peak while Telecom Egypt moved to 20-month highs toward the end of the month. Real estate firm Sodic attracted buyers and continued to rise in October, adding 11%. Orascom Telecom rose 8%; Orascom Construction traded sideways but could announce it was awarded a $109 million contract to build Egypt’s first integrated solar power plant. On Oct 25 Egyptian authorities said the country’s new NILEX bourse for small cap stock (capital range $90,000 to $4.5 million) is assuming operations with modest first-year listing goals.

Cairo SE: Hermes (1 month)

Current Year High: 82,439.79 Current Year Low: 55,853.97