Abdul Jessani is reveling in newfound

independence. “Any profit

or loss is now all ours,” says the

confident first chairman of Unilever

Levant. Jessani came to Lebanon two years

ago to set up a regional subsidiary of

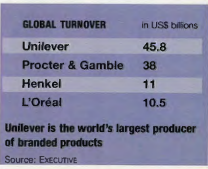

Unilever, the world’s largest producer of

branded products, including Lipton tea,

Signal toothpaste and Lux soap. Global

revenues totaled $45.8 billion last year.

Jessani’s arrival followed a massive corporate

restructuring of the company.

Decisions concerning international markets

were moved from the European

boardroom to the regional headquarters.

The UK-based Export Division, previously

responsible for handling regional markets

through a myriad of local distributors, was

dismantled. Today, Unilever supplies the

capital, key human resources and global

brand strategy while the local outfits are

responsible for marketing strategies and

turning profits in their respective territories.

Jessani now sits at the helm of Unilever

for Jordan, Syria and Lebanon, where he is

responsible for the performance of 16 key

brands. The firm’s rise or fall in this part of the world is his responsibility and Jessani

relishes the challenge. His sales target for

the Levant is $150 million by 2003, up

from less than $20 million in 1998, a very

ambitious goal considering that the region

is in the midst of a recession. That figure is

based on expectations of grabbing at least

25% of the $600-million Levant market

for product categories where Unilever

competes here. So far he is on target, having

increased sales by 200% in the first

two years.

How did he do it? Jessani reduced

Unilever Levant’s portfolio of brands from

44 to 16, to focus on brands that have the

greatest potential for growth. Products like

Ragu spaghetti sauce, Timotei shampoo

and Gibbs Sport aftershave were dropped.

The move preceded a similar restructuring

by the mother company. Over the next five

years, Unilever will reduce its brand portfolio

from 1600 down to 400.

“Our experience has shown that, when we

focus on a more limited number of brands,

we excel. If you have big brands, then you

have an advantage of scale in terms of production

and marketing costs and an advantage

in distribution. If you look at our big

brands, you notice that they are more profitable,”

says Jessani.

Unilever has boosted local manufacturing

for specific ‘champion brands’ products,

thereby reducing import costs. Some new

products have also been added to the local

manufacturing line-up.

Two years ago, Unilever manufactured

from one factory in Lebanon producing

only Lifebuoy soap. But since Jessani’s

arrival, the company acquired a second

factory. Now the company produces Lux

soap, Comfort fabric softener, Jif, Sunsilk

and Organics shampoo. In Syria, where the

company manufactures Sunsilk shampoo,

Omo and Surf laundry detergent and

Signal toothpaste, it has increased its production

of Sunsilk from 200 to 1000 metric

tons in the last two years. Unilever has

a total of six factories in the Levant.

Jessani has also streamlined the manufacturing

operations by reducing the number

of work shifts, changing the plant layouts

and machinery, designing systems

that reduce wastage and reorganizing loading

and unloading procedures. “We have cut a lot of costs at the factory and from the supply

chain,” says Jessani. With manufacturing

costs reduced, the company has been

able to reduce prices on brands like Omo at

a time when sluggish economies have cut

into people’s purchasing power. In Syria, the

shop price of the 2.7kg pack of Omo laundry

detergent was cut to 235 Syrian

pounds, just 10% more than local brands

and 20% cheaper than the only other foreign

brand produced under license in Syria,

Obegi’s Persil. But Jessani stresses that

price cutting must be selective so as not to

harm brand image.

Unilever Levant has also begun offering

more affordable options. About a year ago,

it started importing Good Morning, an

olive oil based soap, which is manufactured

at its sister company’s plant in Egypt

and is 40% cheaper than Lux. According to

Jessani, the brand has proven to be a strong

performer in Syria because it is less expensive

and superior to local competitors.

The company is also reorganizing its

imports, which include Dove soap,

Impulse deodorant, Close Up toothpaste,

Lipton tea and Vaseline. The breadth of

Unilever’s network can make imports a

more viable and cheaper alternative than

manufacturing. “We went through our

inventory across the world and checked

which brands were the most relevant for us,

which would suit our requirements best,”

says Jessani. For example, he found that the

cheapest way to supply the Jordanian market

with Organics shampoo was to import it

from Saudi Arabia, where it is manufactured. A trade agreement between those

two countries means that tariffs are near

zero. Unilever has also changed the marketing

strategy of some key products, like

Lipton tea and Vaseline.

So far, Jessani’s measures to boost sales

have had mixed results. On the positive

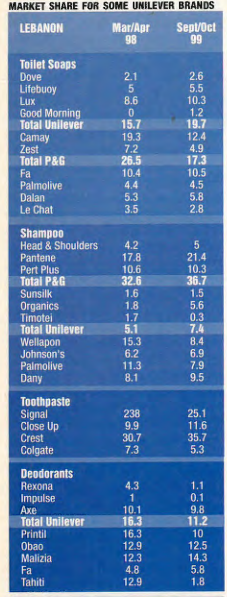

side, the market share of Lux soap has

increased in Lebanon from 8.6% in the

spring of 1998 to 10.3% by the fall of last

year, according to a retail audit conducted

by AMER Research. (AMER’s bi-monthly

retail studies were taken from surveys of

medium-sized supermarkets and did not

include statistics from hypermarkets or

cooperatives prior to 2000). The company

made this gain by keeping the price of Lux

down and hiring former Miss Lebanon,

Joelle Bohlok, to promote the product.

“They pushed Lux into the top three in the

soap category in Lebanon. They used to be

well behind,” says Georges Obegi, president

and CEO of Obegi Consumer Products. As

producers of everything from Persil laundry

detergent to Fa soap, the Obegis are one of

Unilever Levant’s main competitors.

Today, says Jessani, Unilever is the

Levantine leader in the sale of personal

wash products. With Dove covering the

premium market, Lux covering the middle

ground, and Lifebuoy and Good Morning

at the bottom end of the market (see table),

Unilever had carved out a 19.7% share of

the Lebanese soap market by October of

last year, according to AMER. This compares

with a 15.7% market share in early

spring of 1998. By contrast, the share of

Procter & Gamble (P&G), with their

Camay and Zest brands of soap, declined

from 26.5% to 17.3%.

In Lebanon, the company has also managed

to push up the local market share of

Comfort fabric softener from 48.5% to 56.2%

in the same time period. By manufacturing

locally, Unilever has drastically

reduced shipping costs, which were high

because of the bulkiness of the products. In

Syria, says Jessani, sales of Sunsilk shampoo

have increased nearly ten times while in

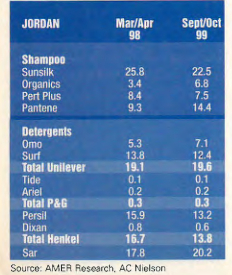

Jordan it’s the leading brand with a 22.5%

market share.

But in fact, not all

Unilever bets have

paid off. While demand for Sunsilk

in Jordan and Syria

has been strong, the

brand’s performance

in Lebanon

has been disappointing.

According to

AMER, the brand

controls just 1.5% of

the market. Results

were so poor that

Jessani was recently

forced to relaunch

the product.

Organics shampoo,

another major Unilever brand, has

made some gains in Lebanon and Jordan, but

is still struggling with less than a 7% share in

both countries.

“Organics achieved some market share

gains in Lebanon, but not as much as they

had been expecting,” says Nazar Najarian,

the general manager of Cosmaline, a Sarraf

Group company. “The brand’s message,

‘health from the roots’, is not unique.

Procter & Gamble has already used it. It

made Unilever look like imitators, not

innovators.” Locally, Unilever has a long

way to go if it wants to challenge P&G’s

near dominant position in the shampoo

market. The three Unilever brands of

shampoo, Sunsilk, Organics and Timotei,

control just 7.4% of the market, compared

to P&G’s 36.7% with Head and

Shoulders, Pantene and Pert Plus.

By its own admission, Unilever needs to

pay more attention to the lucrative detergent

business in Syria. It already cut the price of

Omo but it’s still not clear whether the

move has helped the brand retain its estimated

15% share of the market against a

strong push by Obegi to increase Persil’s

5%. In Lebanon, where a tiny number of well-established brands dominate the market,

Unilever has decided against entering

the race for the time being. “Unilever is not

a competitor. Persil, Ariel and Bold have

90% of the market,” says Nadim Tabet,

managing director of Transmediterranean

that distributes P&G products. Only in

Jordan has the company been successful in

marketing detergents.

Unilever’s

more middle-range brand Surf, with a

12.4% share, is the

third most popular

detergent, behind

Sar with 20.2% and Persil at 13.2%, according to AMER’s figures.

Coupled with Omo’s

7.1%, Unilever has

the second best selling

portfolio of detergents there.

Jessani might

introduce new products

to the market, though he declined to say

which ones. The Levant market for all

product areas where Unilever international

competes is about $1 billion, compared to

the $600-million market Jessani is currently

fighting over. Bringing in a few more key

products could provide a boost.

Despite Unilever’s strength as a multinational,

the future won’t be an easy ride for

Jessani. Competition in the region is getting

more fierce. L’Oreal has opened its own

offices in Lebanon and there are strong

rumors that Colgate-Palmolive will follow

suit. P&G reached an exclusive local

distribution agreement with the Joud trading

company in Syria six months ago.

Joud has assembled and trained a 100 person

sales and distribution team and has a

sales target of $10 million for this year.

Jessani is also looking east.

Unilever’s sales are divided about equally

between the three countries. But with a

population that is nearly double that of

Lebanon and Jordan combined, Jessani

feels that Syria really represents the greatest

potential for the future. All that is needed

now is for the economy to liberalize.

Jessani is betting it will.