The Messiah?

Chafic Muharram, former vice governor

of the central bank, has been asked to

take over the helm of the faltering Banque

Libanaise pour le Commerce (BLC) by the

bank’s general assembly. As chairman and

general manager, it is hoped that he will

steer the financial institution out of what has

been an almost unending series of troubles.

First came the nasty break-up of the

Byblos Bank–BLC merger. Then, what

seemed like a flawless marriage between

BLC and the United Bank of Lebanon

turned into a disaster when the central

bank demanded that Safi Harb, the bank’s

new chairman and the mastermind behind

the merger, get the boot after he was implicated

in illegal money lending.

Confidence has been waning on BLC, a

listed bank on both the GDR market and

the Beirut Stock Exchange (BSE). This comes not only

from the botched mergers. Analysts have

also become disgruntled over the BLC’s tardiness

in reporting its yearly results. They

claim that the bank lacks transparency,

with very little in the way of public access

to the consolidated financial statements for

the recent merger.

According to one analyst, “The appointment of Muharram is what

BLC needs today. He has experience in

the central bank, is conservative and the

bank needs stability. This may bring confidence

back to the bank.” He adds that the

major shareholders were put to the test:

The central bank requested a $40 million

raise in capital and a $50 million subordinated

loan to the central bank, and they complied.

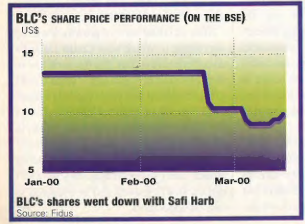

But, throughout the Harb fiasco,

the performance of the bank’s shares has

been dismal, with stocks plummeting 27%

on the BSE and 28% on the GDR market so

far this year.

Holding on

The only closed-end investment fund listed

on the Beirut Stock Exchange suffered

a second disappointing year in 1999. The

value of Lebanon Holding’s portfolio

dropped 13%, from $45.8 million in 1998 to

$39.7 million last year. It started at $50 million

when it was launched in August 1997. Its net

asset value fell from $9.16 to $7.99.

The fund, which invests strictly in local

companies, got hurt the most by its stake in

two industries. Liban Beton, a leading

ready-mix cement company, has been hit

hard by the paralysis in the construction

sector and has suffered heavy losses.

Lebanon Holding also had to write off its

$4.4 million investment in the pipe maker

Eternit, which is filing bankruptcy after

several years of losses.

The bulk of the fund’s portfolio is in listed

banks – such as Banque Audi, Byblos Bank

and Banque du Liban et d’Outre-Mer. But,

despite their solid fundamentals, the banks’

shares, like the remainder of Lebanese

stocks, have been performing poorly.

Lebanon Holding is trying to buck the downturn. In the fourth

quarter, the company increased its stake in

Société des Grands Hotels du Liban

(SOHL), owner of Vendome and Phoenicia

Hotels, and First National Bank. Phoenicia

just opened last month, and, says Khalil

El-Khoury of Lebanon Holding, “It is the only

five-star hotel with five-star service in Lebanon. It

will have excellent cash

flow in the future, and its

stocks will probably

surge.”

But the future of the

fund and its shares, which

dropped 21% in 1999,

remain doubtful. According to one analyst,

“It can only see brighter

days when there is peace.”

A new Bou

Bou Khalil Markets (BKM) will be

adding a fifth supermarket to its chain,

this one in Ras Beirut. The new store –

smaller than the others at 2,800 m² –

is the second

to open in the last five months, following

the opening of a 4,000 m² Bou Khalil in

Tripoli last October. More are planned during

the next five years.

Sales, in the meantime, have been on the

rise for the supermarket chain, increasing to

$15.47 million by June 1999, 17.25%

above sales figures for the same time in

1998. But earnings have been declining,

dropping to $602,000 during the first half of

1999, 17.3% below earnings for the first

half of 1998.

“The chain is undergoing

heavy expansion, bigger than expected,”

says Walid El Khalil, head of the investment

firm Tulip Investments, who helped take

Bou Khalil public when he worked for

Banque Libanaise pour le Commerce’s

capital markets division. “Expenses shoot

up more than revenues during expansion.”

Bou Khalil’s shares have also suffered in

1999, down 17.6%.

A quick and

efficient IDAL,

hopefully

The Investment Development

Authority of Lebanon (IDAL) is trying

to make Lebanon a little more

investor-friendly. The organization has

opened a special office called “One-Stop

Shop,” which will assist investors in

getting through what is seen by many as a

maze of bureaucratic procedures.

IDAL is also planning to set up an

“Investors and Business Information

Center” to provide statistics, economic

data and relevant information for starting

a business in Lebanon.

“It’s a great idea because it will

reduce a lot of the bureaucratic difficulties

and red tape that investors have to go

through in order to invest in Lebanon,”

says Nassib Ghobriel, a Lebanon Invest

research analyst. “The real question,

however, is whether they will be able to

follow through with their intentions.”

IDAL recently announced that the long

delayed Linord project to rehabilitate

Metn’s northern coastal highway, from

Antelias to the Beirut port, will be relaunched

by summer. The project

requires the reclamation of 2.4 million

m² of land, the construction of a new

sewage plant, the development of an oil

storage facility, a marina and a small harbor

at an estimated cost of $550 million.

Last year, when the project was first proposed,

IDAL had trouble finding

investors. It remains to be seen if any of

them have changed their minds.

Top of Form

Gobbled up

Bank of Lebanon and Kuwait SAL

(BLK) may have a new owner.

Jordan’s Al-Ahli Bank, which has five

branches in Lebanon and has been operating

here for 39 years, signed an agreement

to acquire an 85% stake in the financial

institution for $22 million.

The deal, part of

the bank’s strategy to expand in Lebanon,

Jordan, and throughout the Arab world,

will create a medium-size bank with 11

branches, total assets of $250 million and

customer deposits of $200 million.

“When

a foreign bank wants to expand in

Lebanon, the best way is through acquisition;

they won’t be allowed to get a license for more than two branches a year,”

says an analyst at Lebanon Invest.

The

owners were looking to sell at a time Al-Ahli

was shopping around. “After studies

were done, we chose BLK because it’s a

clean bank, with a clean loan portfolio and

high capital,” says Rafic Aramouni, Al-Ahli’s

general manager. “Based on the

bank’s ratios we don’t expect any surprises,

unlike many other banks, and the size of

its staff and the number of branches were

appropriate.”

The bank’s aim, Aramouni

adds, is to become one of the larger financial

institutions in the country. The central

bank has given its preliminary approval to

the purchase and final approval is expected

within weeks.

Bottom of Form

Canning them

kindly

When your business starts suffering

losses, the first thing to do is cut

costs. That often means making the tough

decision to let go of workers. Société des

Ciment Libanais, Lebanon’s largest cement

producer, had plans to lay off 300 employees

after the company’s net income fell

from $14 million in 1995 to a net loss of 1.1

million in 1998.

The news, obviously, was

not greeted kindly by the company’s labor

union, which promptly intervened to try

and stop the move. After a six-hour meeting,

a compromise was reached between SCL’s

management and staff. Instead of layoffs, the

company would offer a cushy early retirement

package to hundreds of its employees,

giving them 36 months’ salaries in addition

to end-of-service indemnities they would

receive from social security.

“There are already nearly 100 people who accepted

the offer,” says Antoun Antoun, head of the

SCL employees’ union.

SCL invested in a

$165 million furnace before discovering

that demand for cement was below expectations.

With construction grinding to a

halt, demand for cement nose-dived, with

deliveries dropping 25%, from 4 million tons

in 1995 to 3 million in 1999. Insiders feel

that the company’s losses in 1999 will be

much higher.

Cyber trading

A new online trading website called

myTrack.com was recently introduced

in the Middle East by Dot-LB, the

agent of Net2Phone. The company is marketing

myTrack in 9 countries: Lebanon,

Syria, Jordan, Kuwait, Egypt, the United

Arab Emirates, Saudi Arabia, Cyprus and

Turkey.

The website requires users to download

special software (5 MB) and open a

minimum cash account of $500. Non-US

citizens are exempt from a tax on profits, but

they are required to open an account at

the Bank of New York for trading on

Nasdaq and over-the-counter (OTC).

Commissions will cost $15.95, and customers

will have to choose between three service

plans ranging in price between $20 and $80

a month. According to marketing manager

Ibrahim Choueiry, Dot-LB’s revenue

will depend on the number of clients it signs

up. So far, the company’s client base has

grown to 200 in 50 days, mostly Lebanese

and Lebanese expatriates in Arab countries.

“We expect to break even in about five to six

months,” says Choueiry.