“The existing dual exchange rate is not suited for the long-term recovery of the Lebanese economy, because of its distortionary nature and the limited availability of FX-resources in the parallel market.”

The Lebanese Government’s reform program, April 6 draft

Chained to the dollar for the longest time under a policy favoring partisan interests—but not Lebanon’s socio-economic best interests—the Lebanese lira has broken loose from its peg. The rate of LL1,500 to the dollar, an automatic beacon in the Lebanese economy for over 20 years, has been partially replaced by a parallel market rate that has been dancing and twirling all over the place, from LL1,800 to LL2,200 and back, and up again to within spitting distance of LL3,000 to the dollar. But it is not a happy sort of freedom. According to a new assessment that was produced as part of a nameless rescue plan for Lebanon—and leaked in draft form soon after its internal release on April 6—the emergence of a parallel market has done no good and this market has no future beyond the middle of next year.

In principle, the paper argues, the widening gap between Lebanon’s official and parallel rates of exchange is prone to be the source of “social inequalities.” The gap could have a rentier effect of leading to economic rents for accessing dollars at official rate, which would be “prolonging an already inefficient system.” And adding to this economic burden of the parallel market that has existed for the most turbulent six months in the past 28 years is the scarcity of foreign hard currency. This scarcity is due to unofficial but increasingly stringent bank-imposed capital controls that have been in place from last October and are continuing to this date. These distortions of capital flows are preventing the emergence of a functioning parallel market and drive parallel rates to excessive highs, the paper argues. But what is the story with the dollar peg, and why is this peg officially still in existence?

One can think of a peg as a form of partnership, a marriage of currencies in which one currency follows the other for better or worse. However, since the business of following is 100 percent one sided—it is always the pegged currency that follows slavishly, and never the currency that it is pegged to, usually the US dollar—these partnerships, at least for larger economies, rarely last more than a few years or even a few months accompanying a promise of fundamental economic reforms. And when the promises are not kept the consequences are often spectacular, as seen in examples from Mexico and Turkey in the 1990s to Argentina and Egypt. In the better cases where a peg has been engineered, it was often done for a limited time and was designed as support tool to overcome a financial crisis, allowing a pegged country to stabilize its currency.

Pegs have been perceived by economists as limited because they come with a conceptual downside known as the trilemma or the impossible trinity—the practical impossibility to simultaneously have a fixed foreign exchange rate (peg), free flow of capital (no controls), and an independent monetary policy. Since amounts of capital behave like profit-seeking missiles, recent financial history shows that whenever the interest rate environment in a pegged country with no capital controls opens wide doors for capital to profit from carry trade, the central bank of a pegged country cannot make its own interest rate decisions to stabilize the domestic economy. It has to copy the other country’s prevailing interest rate, the hypothesis goes and practical experience of the past 40 years has corroborated.

To get away from economic deserts full of narrow triangles, one can compare a currency pairing perhaps to generic partnership. Productive partnerships have consequences. Short-term exclusionary partnerships involving individuals, enterprises, and even currencies that begin with common interests tend to yield shared outcomes but can also produce divergences. These divergences can be curtailed by dissolving the partnership—or they end in a disingenuous breakup.

Open-ended productive partnerships with solid foundations and processes, such as mutual/shared ownership of equal-value assets, agreed principles, and dynamically developing joint interests under adherence to proactive and transparent internal information policies, can generate continually improving superior outcomes as well as intensely align the stakeholders in the partnership—like a couple in a marriage that finishes each other’s sentence or is so in tune with each other’s intentions that they appear to read each other’s minds.

Such intense and mutually beneficial alignments can emerge not only in social and economic partnerships of equal individuals, but also in asymmetric partnerships of senior and junior business partners, in and between enterprises and stakeholders in long-distance enterprises. But the downside risk of such uneven partnerships is immense. Total dependency can develop into hell for the weaker partner. The one-sided, open-ended, and overlong currency partnership of Lebanese lira and US dollar lasted for over two decades, in which it seemed to defy the impossible trilemma and survived many external stresses, episodes of capital outflows, and pressures of divergence.

The partnership might have continued as it had, with the knowledge that the freedom to set its own interest rate policy is something of an illusionary freedom for a small country embedded in webs of international trade. After all, no theorem in economics is unshakable, many very small countries have a fixed exchange rate policy without drawing undue attention, and there is a polar counter-perspective to every presumed truth. But the end result of the long dollar partnership—first adopted to accompany nation building, reforms, and private sector’s recovery after the Lebanese Civil War—was disaster for the Lebanese, largely due to the establishment’s perpetual failure to enact lasting reforms.

According to the above cited draft rescue plan, the lira was increasingly overvalued during the last few years. Notable ratios of overvaluation included estimates of 6 percent in 2008, 15 percent in 2012, 18 percent in 2014, 12 percent in 2016, 19 percent in 2019, and 33 percent in 2020. Other signals of alarm have exacerbated the problem. As confidence in financial markets evaporated and the long accumulating economic imbalances came to erupt, the relationship of currency dependence turned into hell for central bank, Banque du Liban (BDL), the suddenly incapacitated banking sector, and all Lebanese. The peg of the lira to the dollar is broken in principle and for most practical purposes with it the hopes for reforms toward an efficient and functional Lebanon.

Now, with economies and financial interests that could be not more dissimilar, and finding themselves in a totally untenable currency relation on top of a totally untenable economic hole, the question of the Lebanese is how to survive after the divorce and how to save any monetary integrity. For more than five months, this problem of the factually broken peg has become increasingly exacerbated although the nominal parity was supposedly maintained. What to do in this quagmire, one of the many life-threatening and chronic conditions of which the almost comatose Lebanese economy has for months been in need of intensive care?

Plans long overdue

This problem has been no secret. At the Executive roundtable series just before Lebanon’s Independence Day last November, the lira peg and its future was one topic on the agenda, with a plurality of discussants expressing views that the peg in the long run would not be defensible. Some participants at the table argued for a crawling peg, others saw a need to stabilize the exchange rate at the official level before carefully revising it.

While this type of discussion has been repeated many times since—for example, in the public squares during the thawra (revolution) and via online meetings under coronavirus conditions—efforts on part of official Lebanon to disambiguate the picture of the two diverging rates until very recently were foggy. Unequivocal statements on the peg’s need for replacement were scarce both before the appointment of a new government in January this year and since that theoretically pivotal moment.

In the early days of the mother of all crises in Lebanon, assurances that the peg would not be touched were made from the side of the monetary authorities and its highest representative, BDL Governor Riad Salameh. Even in late March, the issue of having to change the exchange rate policy was not clearly stated and the unfortunate bipolarity of the lira was only alluded to by Minister of Finance Ghazi Wazni.

When Wazni went before a video conferencing setup on Friday, March 27, he had something to say to bond holders. Those were the people who have financial claims on Lebanon and who have hardly been happy campers since the country’s announcement in early March that they would not settle what was due in regard to the then-outstanding eurobond on March 9 (an announcement from the Ministry of Finance [MoF] later in that month had confirmed that Lebanon would not be making its payments for any of this year’s maturing eurobonds in foreign currencies).

But what the minister told these finance professionals with regard to the schizophrenic reality of the Lebanese foreign exchange (FX) rate in his opening speech (as published on the MoF website) was only a fleeting mention of the “critical level of available foreign currency” at the central bank, after which Wazni went on to acknowledge, equally vaguely, that one of the problems facing Lebanon was the “FX liquidity crisis, including the depreciation of the parallel exchange rate.”

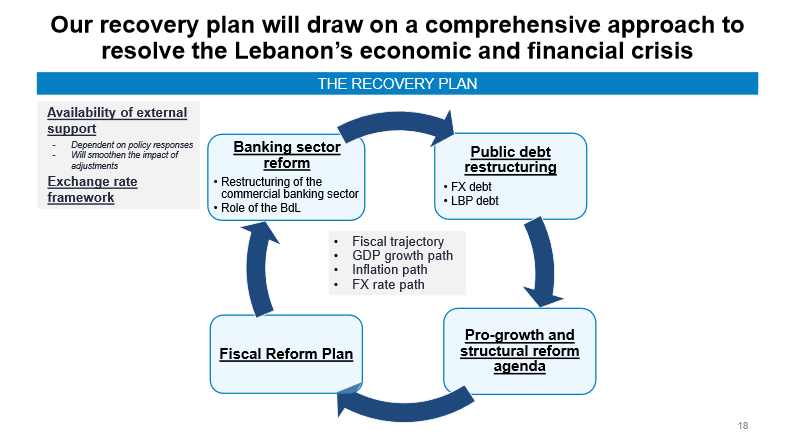

As several stakeholders in the challenge of realizing a national economic recovery plan for Lebanon—which includes everyone in the country—noted in the days following the MoF investor presentation, the provided content was on the light side. “Big on words and small on deliverables or plans,” as one entrepreneur put it to Executive.

Indeed, the minister’s observation was not followed in his opening speech by a rectification formula or outline of practical steps for dealing with the Lebanese exchange rate. Nor, according to content displayed on 27 presentation slides presented subsequently during the event, was such a formula made concrete there. One slide (see below) mentioned an exchange rate framework, but did not provide hints to any intended FX rate path or plan for an exchange rate framework.

To crawl, to float, to leave well alone?

Seeking for deeper understandings of the overlong ongoing currency conundrum, Executive asked economists for their opinions on the lira peg’s sustainability and their perspectives on a devaluation—meaning a decision to revise the currency exchange rate downward from the decades old existing rate and of ca. LL1,500 to the dollar to a specific net level—or a depreciation—meaning a relinquishment of the official peg in favor of letting market forces determine the overvalued lira’s trajectory.

For economist Marwan Mikhael, it makes no practical sense for the government to embark on a redesign of the exchange rate regime at the moment. “The issue is that there are no advantages from devaluing the official exchange rate right now. As long as you have capital controls, the parallel market will depreciate more if you devalue the official exchange rate,” he tells Executive at the end of March. “There is thus no point of devaluing the official rate at this time. [Only] if you are lifting capital controls, can you devalue. This is my opinion.”

According to Mikhael, the theoretical increase of competitiveness of Lebanese goods in international markets after a devaluation is hampered by the highly dollarized cost structure of Lebanese companies that can even include their payment of salaries in US dollars. A market with a single exchange regime could be realized on fresh money (money transferred into the country after November 17 last year), he adds: “For everything in fresh money, there should be a unified rate.”

In his perception, Lebanon should move toward a crawling exchange rate peg—one that allows for gradual adjustments and envisions minor down and up moves of the exchange rate, even as some overshoot of the rate is to be expected in the early stage of a transition to a crawling peg via an intermediate free float decision. Describing the IMF program that has been implemented with a similar process in Egypt as successful, he advises that it would likely be beneficial to allow the market in this way to provide an indication on the rate at which to position a crawling peg. “This is why you perhaps will first float it and then get the right price that you can defend,” he explains.

Seasoned economists Elie Yachoui and Roy Badaro (speaking separately to Executive prior to the March 27 investor presentation), both point out that the opposition to a fixed exchange rate peg in Lebanon has almost as long a tradition as the peg itself. “I am totally against pegging and have been so since the beginning [of the policy in the 1990s],” Yachoui says. “Market forces have finally overcome Banque du Liban’s policy of pegging. We are a free market economy and have to operate according to market dynamics in a monetary market and all other markets.”

Yachoui tells Executive that he favors depreciation as the more market-compliant path over a governmental decision to devaluate, and also that he prefers a free float of the currency as opposed to a crawling peg or managed exchange rate regime in any form. “It is high time to see free float of exchange in Lebanon after 27 years of fixed rate,” he says. “I am against a devaluation to a new and lower peg or a managed exchange rate regime because I am against the central bank committing the same error again.”

In Badaro’s perspective, the decision for a fixed exchange rate regime in the 1990s was linked to international policy preferences at the World Bank level, in line with what was then called the Washington Consensus (as defined by economist John Williamson, not to be confused with the later usage of the term). The peg might have succeeded as monetary Lebanese policy of the early 1990s if peace in the Mashreq would have been achieved then, but as peace was but a dream by the late 1990s, the policy should have been changed back then. “They stuck to it and we are paying the consequences of the decision,” he says.

Differing in this from Yachoui, Badaro is in favor of a gradual freeing of the exchange rate and recommends a crawling peg. “I think that before October, [2019], the equilibrium rate was around LL2,300 [to the dollar],” he says. “[Adopting it] could have brought trade balance, but nobody would listen [to such advocacy].” He points out that neither the MoF nor BDL have a policy addressing the way in which the parallel market’s existence impairs lives of vulnerable population groups.

“Many take advantage of [the black market] at the expense of the poor population,” Badaro says. “I would be in favor of freeing [the exchange rate] but at the same time of revising the minimum salary twice yearly, [so as to] catch up with inflation. There is a cost-push inflation [created by] the pass-through of the exchange rate but this inflation would decrease if we take measures of promoting a pro-competition environment, which means to abolish all the anti-competition regulations, exclusive agencies, and any monopolies.”

For Tamim Akiki, an entrepreneur and data sleuth with training in heterodox economics, the devaluation issue has to be dealt with as part of a larger context. Maintaining an exchange regime that is close to the status quo of a fixed peg would first require deep research and investigation of what benefits this could provide to a very small economy like Lebanon, and for how long and for what reason a fixed regime should be maintained. A new exchange rate policy that even considers a fixed peg should therefore first address questions such as: Do you want to maintain a fixed exchange rate for a year so that you can overcome a certain crisis?

Saying that rather than adherence to any fixed rate, a different regime should be pursued, Akiki tells Executive: “I think there is a general consensus that having a more flexible monetary policy can be very advantageous for Lebanon. So I don’t see why we would stick to the status quo. My view is that Lebanon should move to something like a managed float, which is what exists in most of the world. Everybody manages their exchange rates—it has never been a total free floating environment. I think we have to move to something similar so that we don’t have this buildup of instability over time.”

The top priority in his view, however, should be that a new exchange rate regime is integrated into a national strategy for the economy. “I think the devaluation has to be part of the rescue package,” he says. “My concern is much more related to seeing if this will be an opportunity to move to a modern sovereign monetary policy or will this remain a policy that has proven to be a mistake. What we need to do is start developing a master plan for the next financial system in Lebanon. This should include a floating exchange rate, which can always be influenced by the central bank [BDL].”

With devising a promising exchange rate policy being a major challenge in itself—let alone seeking to do so in combination with measures aimed at increasing the purchasing power in the population and fostering improvements in competitiveness that is based not on price competition but on increased reliance on skilled labor—it becomes clearer why the issue of adjusting the lira exchange rate appears to be viewed by many in government and even some in industry as a hot potato. This impression is heightened even further when one considers that economists generally agree that a traditional tradeoff between pricier imports and cheaper exports will not give a significant advantage to local producers, most of whom are a long distance away from being ready to tackle international markets with efficiency.

Economic rescue proposal

A positive flash on the thought horizon of proposing an economic rescue that incorporates a clear view on the lira reached Executive on April 1. Consultants Gerard Charvet and Ziad Hayek (who, like Mikhael, was one of the highly knowledgeable experts participating in Executive’s roundtable in November) published a plan that explicitly addresses the FX issue and lira devaluation under inclusion of inflation aspects. Stipulating that four core concerns need to be dealt with in the people’s interest, the plan lists the national debt, banking sector health, depositor protection, and the exchange rate of the Lebanese lira indispensable targets for attention.

The consultants propose as a second thematic focus of their plan—right after advocating for the establishment of a defeasance company that holds state assets by a new law—to reset the price of the lira at LL3,000 to the dollar. As the next step in a viable currency policy, they recommend letting this devalued lira “float at least for an interim period before installing a crawling peg policy,” and soon thereafter eliminate the lira’s tail of three zeros, which would mean targeting parity at three (new and rationalized) lira to the dollar.

In a financial projection, the Charvet-Hayek plan calculates the budgetary impact of their devaluation/float/crawling peg scenario on basis of their proposed ratio of LL3,000 per dollar rate. They say it would modify the central bank balance sheet from LL216,541 billion in assets and liabilities to LL302,981 billion. Charvet and Hayek advocate that their proposed economic measures ought to be brought on simultaneously in one comprehensive package, under inclusion of flanking measures to soften the plan’s social blows to average earners and argue: “The devaluation (free float) will restore competitiveness to the Lebanese economy, stabilize the exchange rate at a real level, and encourage depositors to return to LBP deposits.”

Reasons to be wary

As the economic crisis is showing no intent to vanish—it is behaving to the contrary—it is welcome news that the government as of now has some numbers to discuss on the exchange rate. There is much to be said about the April 6 draft. Much of it can be shocking in good ways, for example when it states early in the text—which is all marked as “strictly confidential”—that the government is committed “to change its harmful practices.” But the plan also reminds of exercises where lip service to social care is juxtaposed with actions that dissolve social stability. Terminology such as “rationalizing public sector employment” and advocacy of efforts to “rein in” salaries and benefits in public institutions (e.g. universities) is not the kind of terminology that departs from neoliberal recipes which, when implemented, regularly fell short of humane successes. As Akiki notes, the plan seems neither ambitious enough nor creative enough and offers prescriptions that “are pretty much the same as in other countries and tend to perpetuate financial and debt crises.”

Justified criticisms on its general drift notwithstanding—and also despite some overconfident assertions on global realities in governmental treatment of systemic banks that sounded off even before the coronavirus pandemic changed every outlook on governmental support for vital economic entities—the draft plan has enticing aspect from the perspective of the need for a clear FX policy. Naming its program objectives and strategies, it declares one of eight pillars to be: “Moving to a more flexible exchange rate policy beyond the near term to lessen strains on BOP [Balance of Payments] and improve competitiveness.”

And it puts some exchange rate policy numbers on the table. As projections, these are debatable but at least they are numbers to debate, starting from an effective exchange rate of LL2,302 to the dollar in 2020—calculated by assuming that 80 percent of economic transactions are conducted at the parallel market rate and 20 percent at the old and still existing official rate. According to the table of numerical projections in the plan, the lira rate would move further from LL2,771 to the dollar in 2022 to just below LL3,000 per dollar in 2024. A parallel market would be tolerated by the central bank as long as absolutely necessary but the bipolar market of today is expected to be replaced with a unified official exchange rate by 2022, the draft plan says.

“The unification of the two rates and the formal depreciation of the official exchange rate require the prior stabilization of the economy and the restructuring of the banking sector,” the authors note, giving their rationale why the discussion over the devaluations and deprecation issue might not be incessantly sizzling on the front burner of governmental elaborations.

Authors of the plan are unequivocal when they declare in relation to the dollar peg that, in their view: “For years, the lack of competitiveness of Lebanese companies has prevented the emergence of a productive and diversified economic base in Lebanon and encouraged the consumption of imported goods through artificially inflated purchasing power.” They are also unmistakably clear in making a statement a few lines earlier that: “The peg to the US dollar that has been maintained over decades is now impossible to restore and must be abandoned as part of the Government reform program.”

For the foreseeable—and by their wording practically indefinite—outlook on the exchange rate, they say that a free float of the exchange rate is in their opinion not advisable as long as the economy has not reached a stable equilibrium but foresee, in the same vein as most economists that Executive inquired with, a managed float or a crawling peg as the best policy after a recalibration of the rate through an initial devaluation and successive depreciation driven by inflation differential.

In theory, a currency devaluation or depreciation is a trade-off affair that makes imports more expensive but exports more competitive. But as increasing competitiveness in export markets appears to be a long struggle in conjunction with an even greater struggle for economic sanity, the deterioration of the lira exchange rate—that is all over the short, medium, and long horizons—could very well be a lesser booster of the competitiveness of Lebanese goods and services than increased reliance on skilled labor and high value-added. For the moment, the question of devaluation and the future of the exchange rate is the monster in the large herd of our economic problems that has come out of the closet and is now waiting to be tamed.

For the credibility of the Lebanese government, the honest discussion of this monster can only be beneficial. Honest discussions and interactions with the Lebanese public, as the example of the devaluation shows, are still in need of improvement. In this sense, an open and transparent presentation of the draft plan to the public for discussion would have been vastly preferable over the emergence of a leaked copy—even if one can hardly imagine a more surefire way than the leaking of a document to whet the appetites of analysts and self-appointed finance watchdogs on social networks, or to honey-trap by definition lazy business journalists who might otherwise not bother with poring over an intellectually advanced document. But the plan did not have to be hidden. When truth comes, falsehood vanishes. Ignorance, as a saying goes, is the shadow of death where knowledge is the light of life.