As recent international attention on Iran has focused on domestic unrest and talks over the nuclear program, the government now faces a major economic challenge.

Change is in the air. Inflation is at its lowest in many years, the Tehran stock exchange has handled its biggest ever privatization and parliament is discussing the phasing out of universal subsidies on everyday items like electricity, bread as well as medicines.

In a highly politicized country like Iran, commentators will assess such changes in terms of the country’s vulnerability to further international sanctions and whether they bolster or undermine the government of Mahmoud Ahmadinejad.

But the deeper issue, according to Djavad Salehi-Isfahani, economics professor at Virginia Tech University and an expert in development economics, is whether the government can channel resources away from consumption, including costly subsidies, towards the investment needed for economic growth.

To benefit more fully from having the world’s second highest combined reserves of oil and gas, Iran must resist popular pressure for “redistribution.”

Promises of a revolution

But this is far from easy. A “lack of transparency in government activity and the public’s naïve view of how the economic system works” means “the politics of redistribution trump those of growth,” Salehi-Isfahani wrote earlier this year.

Ahmadinejad famously promised in his 2005 election win to put oil money on the people’s sofreh [dining table]. But pressure to distribute oil wealth has long been fostered by the 1979 Revolution’s commitment to the mostazafin (the dispossessed) and has led successive governments to keep everyday items priced as low as possible.

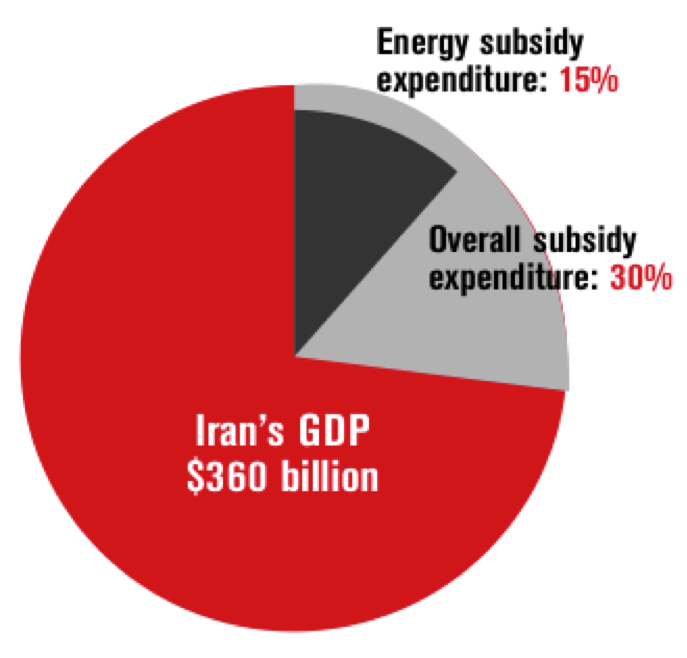

As a result, subsidies of gasoline and other forms of energy amount annually to $50 billion, or 15 percent of GDP. Overall subsidies are as high as $100 billion, or 30 percent of GDP.

The effects on growth are clear. While the Iranian economy has grown faster than most developing countries, it has not met the ambitious 8 percent target set by the country’s five-year plans.

Growth averaged 5.4 percent from 1996 to 2006, reached 7.8 percent in 2007 and then fell back with the world recession and weaker oil prices to 2.5 percent in 2008. The International Monetary Fund last month projected 1.5 percent growth this year and 2.2 percent in 2010.

This is not enough to provide jobs for all the baby-boomers, born in the Revolution’s early years, coming into the employment market. Officially unemployment is 12.5 percent, but many analysts say the real figure is much higher.

Salehi-Isfahani told Executive he was disappointed this year’s presidential election did not confront the challenge of increasing investment.

“I feel that redistribution has a greater hold on large sections of Iranian voters than I realized,” he said. “I had expected that after his [Ahmadinejad’s] failure to deliver [in his first term as president] that more people would turn away from populism. Instead, I heard many people say that he would have delivered on his promises [to redistribute wealth] had he been allowed to by the powers that be.”

For some years, there has been a consensus among Iran’s political class in favor of greater investment of oil revenues and the development of the private sector, especially through privatization. But in practice, politicians’ support has been lukewarm.

The previous government of Mohammad Khatami established a ringfenced Oil Stabilization Fund to collect windfall revenue, but both Khatami’s government and the parliament soon dipped into the fund to finance pet spending projects, often with an eye to elections. Under Ahmadinejad, the fund’s coffers have diminished further, to the point where its level is kept confidential.

Reducing subsidies

Progress has been slow on a privatization program launched under Khatami and given impetus by two rulings, in 2005 and 2006, from Ayatollah Ali Khamenei, the supreme leader, that 80 percent of the state sector be privatized.

Last month parliament began discussing the phasing out of subsidies. The move would be inflationary and will need careful management even though inflation fell to 9.3 percent in September this year — down from the 30 percent range topped in October 2008.

The discussion marks a shift from last year, when parliament threw out a similar plan from the Ahmadinejad government. Salehi-Isfahani feels the “political emergency” of unrest after June’s election has given the president more leeway. “The conservatives in the parliament are less likely to oppose him while he is under pressure from the reformists,” he said.

But liberalization and privatization are never straightforward in a country weaned on oil income with a powerful state and quasi-state sector.

The introduction of petrol rationing in 2007 was a state-led approach. Faced with escalating import bills — at the time, gasoline imports were 40 percent of consumption — Ahmadinejad avoided a market solution and chose to allocate motorists a set amount, through a smartcard, at a subsidized price equivalent to 10 cents a liter.

The move has been a relative success. “It has not reduced consumption in my judgment, but it has at least stopped a rise in consumption,” said Heydar Pourian, editor of the Tehran-based monthly, Iran Business.

Imports have fallen from 200,000 barrels per day (bpd) in 2007 to around 130,000 barrels bpd — making the economy less vulnerable to the gasoline sanctions touted in the United States and Europe.

But reducing the costs of subsidies on electricity, bread and other items cannot be done through rationing, at least not without a costly expansion in bureaucracy. Hence, the government plans to replace subsidies with targeted benefits for the poor.

Middle class discontent

Whatever the longer term benefits for the economy, it will be a huge challenge for Ahmadinejad to manage the political fallout as everyone other than the poor faces the resulting price hikes.

Another problem with liberal economic reform is that it strengthens a middle class whose numbers are already swollen by the expansion of higher education under the Islamic Republic. Iran’s middle class is largely disenchanted with the government and was the backbone of the protests against June’s presidential election results.

“In the last 10 years the middle class has doubled in size while the ranks of the poor have shrunk by two thirds,” said Salehi-Isfahani. “Now the government finds itself in an adversarial position vis-a-vis the middle class, it may adopt policies inimical to their growth and transformation into a productive class. I can see the government move more in the direction of greater control of the economy with more policies aimed at redistribution, which generally hurt growth.”

Privatization is a massive test. Iran’s capital markets are weak, while foreign capital is restricted both by domestic law and US banking sanctions. And yet quasi-state bodies, buoyed with oil revenue, are relatively liquid.

The sale in late September of a 50 percent plus one share in the state-owned Telecommunications Corporation of Iran (TCI) was the largest in the history of the Tehran Stock Exchange (TSE) and raised eyebrows given the economic slowdown.

Iranian subsidies as a portion of 2009 GDP

Islamic revolutionary shareholders

The winning buyer, Etemad-e Mobin, is a consortium of three Iranian firms with varying degrees of experience in the sector. But government critics attacked the sale as an extension of control by the Islamic Revolutionary Guard Corps (IRGC).

After the IRGC’s role was raised in the Iranian parliament, it emerged from parliamentary speaker, Ali Larijani, and Finance Minister Shamseddin Hosseini, that some shares of the three companies were held by IRGC retirement funds.

The TCI sale illustrates how politics make economic reform harder. Iranian telecoms are a potentially lucrative market — cellular penetration is relatively low, for example, at 70 percent — but foreign investors are wary, because of sanctions and the suspicion of foreigners in Iran.

At the same time, IRGC pension funds hardly relish investing abroad, given the corps is targeted by sanctions and was designated a “terrorist” organization by the US Treasury in 2007.

The privatization program has tended to transfer assets from state ownership to quasi-state ownership or to powerful interests with links within the state sector, including social security funds. The IRGC is part of the mix, with its engineering arm already expanding in construction and energy.

“It’s hard to establish whether the growing economic role of the IRGC reflects a central plan or is the result of disparate groups, many with links to the IRGC, jockeying for position,” said David Butter, senior Middle East analyst at the London-based Economist Intelligence Unit.

A sign of how things might develop will come in November as Iran launches a $1.4 billion bond offer to meet a funding shortfall for the South Pars gas field. Despite the rich potential takings on offer in South Pars, international energy majors and western banks are shunning it because of US and UN sanctions.

The Iranian media has reported the bond will offer a 9 percent interest rate. If the bond finds takers domestically, or from Asia, then Iran will have cleared, or at least not fallen at, one of the many hurdles it faces.