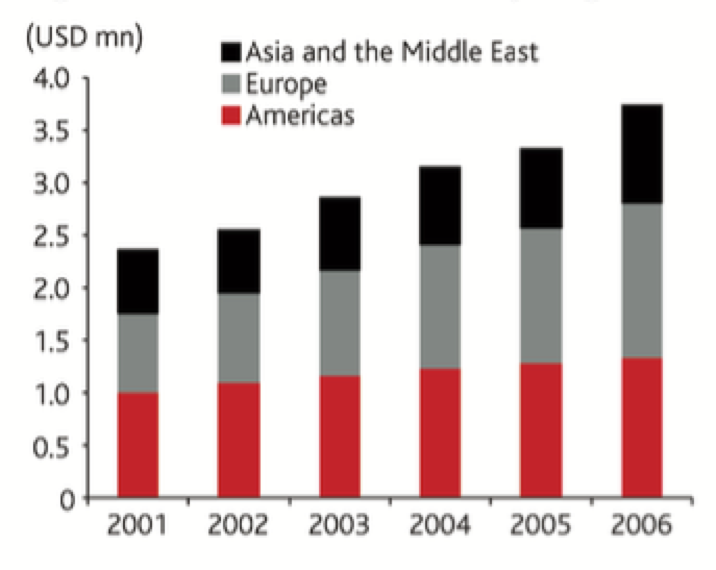

Bancassurance is a sector that has been growing steadily in Lebanon in the last few years. After all, the country is known for its thriving banking sector. The consolidation of the industry has translated on the local level in a simplified basket of products, targeting the mass made available in the far regions of the country through a sprawling network of branches.

“Bancassurance was launched in Lebanon about six years ago. Currently we tend to identify two main types of products, which are investment and protection insurance plans,” said Rima Rached Baz, head of the Non Credit Product Unit at Bank Byblos. Under the first family of products featured are retirement and educational schemes, while the second type of insurance includes products such as income insurance, obligatory and third party insurance. According to Baz, the advantage of income insurance resides in a flexible payment plan approach, with installments starting as low as $2, and providing a 12-month income coverage for clients who were fired by their employer.

What’s in the basket?

Naturally, mandatory insurance such as all risk, car and property insurance are also provided by all financial institutions and applied to all loan applicants. Pierre Talhami, Manager of Beirut Brokers, a Bank of Beirut (BoB) subsidiary, underlined that the bank boasts some 11 products, ranging from life, to medical, home owner, travel, personnel accident and saving plans. Expatriate medical insurance plans are among the many products that are offered by Fransabank through Bancassurance SAL, while their non life insurance type is provided by AXA.

Banks tend to depend on various marketing strategies to attract clients. BoB’s strategy relies on the use of brochures placed on bank counters, while depending also its network of personal bankers. “In addition to our existing network of client we also target institutional clients, by making direct calls,” explained Philippe El-Hajj, head of retail banking at Fransabank.

“The main objective of bancassurance products is to reach out to the mass. Insurance is therefore standardized, made more affordable and flexible. Payments are also made through smaller installments. The process becomes easier to understand and less time consuming, most clients who purchase insurance at the bank will be immediately insured,” said Baz.

Although they are sold through the banks’ branch networks, issuance of insurance contracts remains the prerogative of insurance companies. “The major advantage that is inherent to bank assurance is the smoothness and easiness of the service, which is thus streamlined. In addition to reminding their clients of payments deadlines banks also offer lower rates than conventional insurance companies due to the law of economies of scale,” El Hajj said. By adding insurance to their basket of services, banks morph into one stop shops where clients can settle electricity bills, their car loans and buy insurance in one single step. “Insurance services also contribute to the cross selling of all other bank products,” he added.

Selection of insurers

According to Byblos’ manager, insurance contracts bought at Byblos are issued by ADIR, a subsidiary of the Byblos holding group. This partnership allows the company to utilize the bank’s network of 73 branches, Baz explained. BoB’s approach to the insurance industry has been to acquire its own insurance brokerage firm. “Through the alliance of BOB and Beirut brokers, clients have access to a varied basket of products through a careful selection of the best insurers available on the market,” said Talhami.

The manager believes that banking and insurance are two sectors that with time are becoming more complementary. With such partnerships, banks are promoting the creation of a new market, one which falls beyond the reach of conventional insurance and brokerage firms. “With insurance payments starting as low as 2$ per month, banks offer products that are too competitive for other industry players,” Talhami pointed out.

Another insurance specialist, who chose to remain anonymous due the sensitivity of the topic, underlined that rivalry is pitting brokerage firms against banks. “[Clearly], banks are invading the natural arena of insurance brokers and chipping away their client pools,” said the specialist.

In only a few years, the industry has managed to grow tremendously, as banks overcome progressively cultural barriers and are able to better educate clients. “We have noticed a positive change in the behavior of customers who tend to automatically inquire about insurance, which was far from being the case only a few years ago,” says El Hajj.

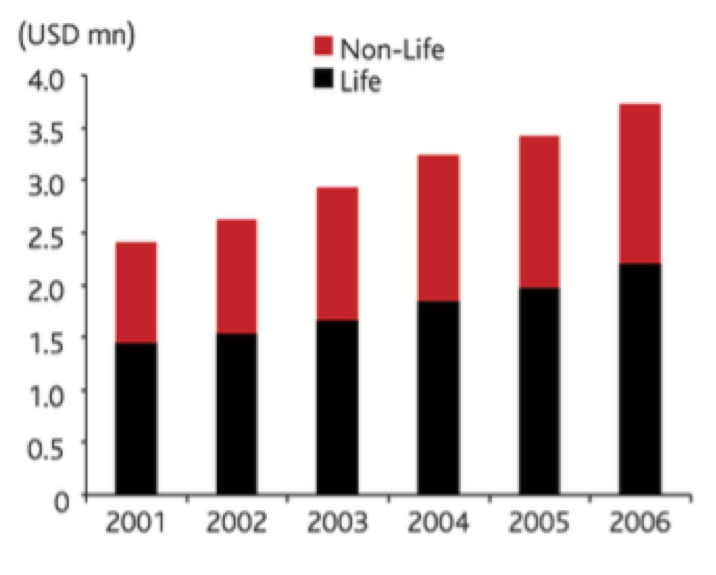

“Life and retirement insurance have also become increasingly popular. There has been more than a 30% to 40% growth in the bancassurance market, a growth that is spread equally over the country. The south and north regions have also witnessed positive growth levels,” according to Baz.

Talhami agreed that growth levels have been steady for some time, reaching a level of some 25% per year. On the other hand, while Hajj acknowledged that 2005 levels were estimated at around 30%, he believes recent figures will not exceed 18% due to product saturation in certain market segments, with Fransabank’s insurance client pool including some 200,000 individuals. “The younger generation is also more aware of and more inclined to buy insurance,” he said. Clients seem to also favor investment plans, as they become familiarized through their banks with the idea of safeguarding their future.

One of the industry’s main challenges remains the relative lack of clarity of the Lebanese legislative insurance environment, which is monitored by the Ministry of Economy. “The adoption of best insurance practices is progressively contributing to the development of the legislative framework,” said Baz. According to Talhami, a proper legislation remains to be developed.

In the current speculative environment, has the subprime crisis reflected on Lebanese life insurance market? Hajj reckons that the subprime crisis has indirectly affected the industry, although it has been subdued by the bank’s alliance with big players such as Crédit Agricole. Fransabank currently boasts some 40,000 life insurance clients .

All managers interviewed by EXECUTIVE agreed that insurance products allow reinforcing sentiments of loyalty among clients who find that their needs are satisfied at a single service window. Most identify culture as the main challenge faced by the industry, hoping that one day insurance will be viewed by customers as a basic need. “The long term objective of insurance companies is for penetration to attain a level of 70 to 80%,”said Hajj.