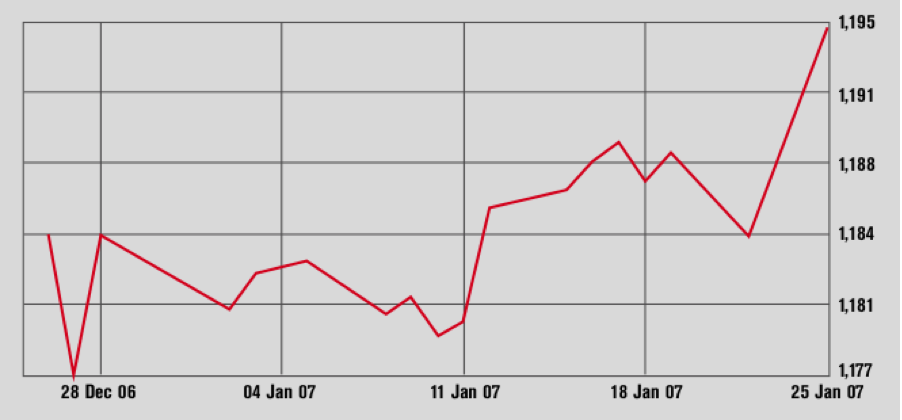

In early January, the Abu Dhabi Securities Market (ADSM) signed a cross-listing agreement with the Muscat Securities Market (MSM), reflecting its will to attract foreign investors, improve its performance and strengthen its links with regional markets.

The agreement between the ADSM, the MSM and the Muscat Depository & Securities Registration Company allows for the listing of Omani companies in Abu Dhabi. Oman and Emirates Company will be the first Omani company to list in the UAE.

According to Abdullah al-Nabhani, the general manager of Muscat Depository & Securities Registration Company, the establishment of an electronic link between the two Gulf markets has fostered greater interest in the UAE markets. “Since MSM established the electronic link with ADSM, we have seen a huge increase in demand for UAE securities in Oman. We hope this agreement will help to not only meet this demand, but also offer investors the opportunity to diversify their risks by having more choice.”

The ADSM currently has 54,000 Omani investors registered making up 7% of the total and contributing $62.62 million to the market. The agreement with Muscat is part of a wider strategy on behalf of the ADSM to broaden its investor base and the number of foreign companies listed on the market. According to Rashed al-Baloushi, the ADSM’s acting director general, “As long as we continue to bring international companies and more diverse investment opportunities to the UAE local markets, we are helping investors to spread their risks, contributing to long-term market stability and ultimately furthering economic growth in the UAE.”

Similar agreements

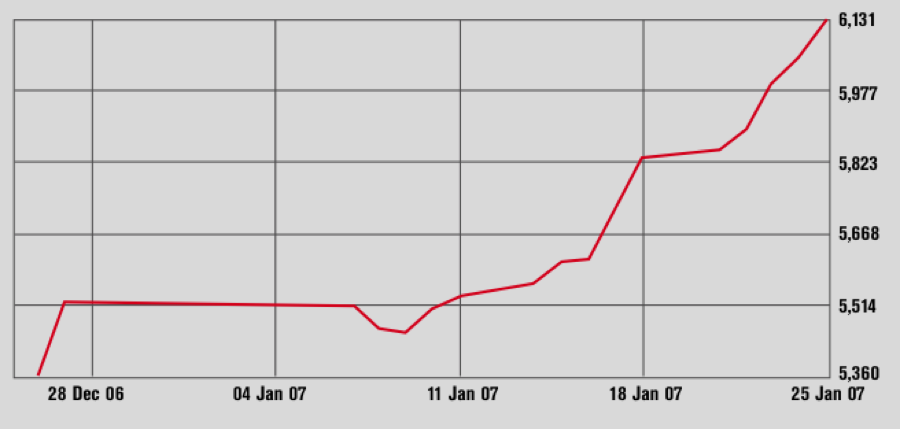

Qatar, Pakistan and Jordan already have similar agreements with the ADSM, facilitating cooperation and dual listing on their respective markets. Pakistan was the first non-Gulf country to sign such an agreement with the Abu Dhabi market. As a result of the memorandum of understanding between the ADSM and the Central Depository Company (CDC) of Pakistan, 10 Pakistani companies have already received approval for cross listing.

This agreement paves the way for further investment between the two countries. There are currently 2,200 Pakistani investors registered on the ADSM, with investments worth $13.61 million. However, investment from the UAE to Pakistan is seen as a key consideration in this agreement. Al Baloushi believes that this agreement will help to consolidate Emirati investment into Pakistan. “Abu Dhabi is a significant investor in Pakistani companies so it is important for us to cement close ties between our markets. We also look forward to working closely with the three Pakistan stock exchanges as we implement our best practice program and continue to improve the regulation and governance standards in the UAE financial markets,” he said.

Hanif Jakhura, the chief executive of the CDC, also pointed out that the agreement would facilitate investment from the Pakistani expatriate community into their home markets.

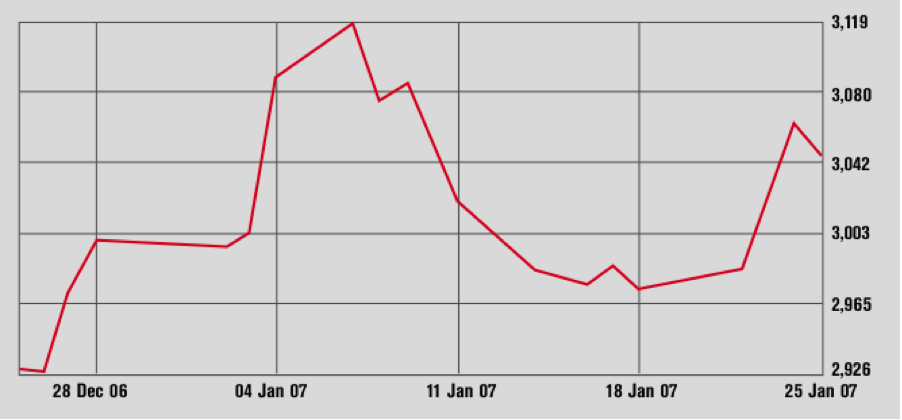

Similarly, the agreement between the Securities Depository Center of Jordan and the ADSM is a step forward for facilitating investment relations between the two markets. Arab Bank is likely to be the first Jordanian company listed on the Abu Dhabi market. The presence of Jordanian investors in the UAE is already well established with approximately 7000 investors registered and investments amounting to $168.8 million.

Seeking more arrangements

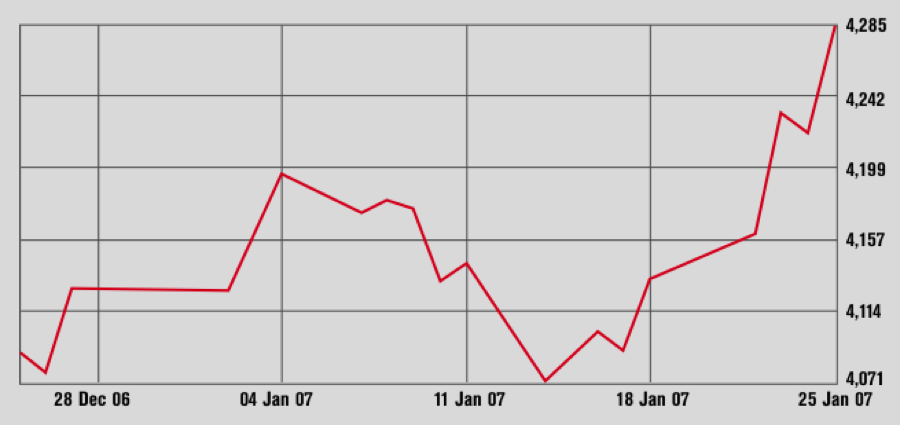

Al-Baloushi said that the ADSM is seeking out more agreements along the same lines. Khaled al-Suwaidi, the manager of ADSM’s listed companies department, also recently told a conference in Singapore that attracting foreign investment is a strong priority for Abu Dhabi’s stock market. He further laid out the measures taken by the ADSM to bring the market into line with international best practice. The ADSM has suggested a corporate governance code for all listed companies as well as a UAE trust and custody law.

These measures are seen as particularly important to attract foreign and institutional investors. Currently, foreigners can invest in 38 out of the 61 listed securities on the ADSM and account for 40% of investors in the market. Al-Suwaidi believes that this figure will increase because of the positive economic development prospects for the emirate.

In spite of the current slump in the market, al-Suwaidi believes the economic conditions of Abu Dhabi are conducive to investment. “Abu Dhabi’s progressive economic agenda, promoting diversification, liberalization and an enhanced role for the private sector, demonstrates that the long-term fundamentals for growth are in place,” he said.