After numerous false starts and retracted predictions of an imminent ground-breaking, Solidere’s much anticipated 100,000 square meter Souks project in Beirut Central District (BCD) finally shifted out of neutral in early June and into high gear.

For the skeptical observer, no less than seven towering yellow cranes now dot the site located just below Weygand Street, proof positive, it would seem, that a formidable retail complex will in fact be constructed on top of the long-finished underground parking.

“This project will surely boost the profits of Solidere as more investors are showing an interest in the BCD,” said one Beiruti broker quoted in the local press.

Of course, while such a bullish estimation may eventually prove correct, at least for the time being, things are very much still in a kind of wait and see mode for possible retail tenants.

“We have expressed our interest,” said Michel Abchee, Chairman and CEO of Admic, the parent company of BHV and Monoprix as well as the builder of City Mall in Doura.

“We were interested in the past… But today they are just testing the market.”

“There is a difference,” he continued, “between the construction and the commercial stages. They are still on the drawing board, in fact they are redrawing their plans given the changes in the marketplace since they first announced the project.”

Although the Souks project may offer some competition to other area malls when it is completed in 2006, Abchee seemed wholly unconcerned by the prospect that a competitor may eventually reside in the BCD.

“They are not competing at all… Each is going after a different clientele. For the Souks it is a downtown clientele.”

Either way, he added, “there is a definite place in the market for international retailers who want to find space that meets international standards. Beirut is lacking here and that is what this project and others are trying to address.

Ras Al Khaimah (RAK), among the UAE’s least developed emirates, is now positioning itself as a serious place for investment. To help promote this process, the World Bank is organizing an Investors Conference to be held in RAK 28-29 May. Under the heading “Invest and Live in Ras Al Khaimah” the conference aims to draw attention to RAK’s undoubted investment strengths. For a start, industries like glass, packaging, sanitary goods, pharmaceuticals, and tableware, which involve huge investments, are already exporting to more than 100 countries. Nevertheless, there is a lot of potential for more investments in manufacturing. RAK has also just begun to develop it tourism capability, and hopes to attract investors for constructing more hotels, golf courses and many forms of water based recreation and sport. All of this of course will act to promote other sectors, including real estate development, as has happened in Dubai. RAK’s public and private sectors launch a few weeks ago of the new real estate company, RAK Properties has thus been a timely move to promote real estate, leisure facilities and tourism.

RAK has considerable land that can be made available strategically for residential, commercial, and service industry development. A comparison of land prices between RAK and other emirates indicates great potential for this. Besides lower-cost land, RAK should be able to capitalize on its good environment and recreational facilities to attract investors. Strengthening of land use planning and management institutions is one of the priorities of the emirate. With the UAE Highway reaching RAK very soon, travel times to Dubai are being greatly reduced. This enhanced connectivity should make it increasingly feasible for people and businesses to locate in RAK and take advantage of the lower cost land there. More advanced transport such as high speed trains will eventually cut even these times down to make commuting to RAK even simpler. Travel from RAK to Dubai airport via the UAE Highway will be no more than 45 minutes. Success in this respect will establish RAK as a world-class investment destination in its own right.

Details of the coming “Invest and Live in Ras Al Khaimah” conference are available at investinrak.com.

Dubai-based magazine Arabian Business recently published a list of the ten richest Arab singers. Top of the bill was Egyptian heartthrob Amr Diab with no less than $37 million, closely followed by Fairuz with $34 million. Diab’s fortune stems from record sales, concerts and – a staggering $17 million – from advertisement deals among which most notably his contract with Pepsi.

Taking into consideration Diab’s worldwide reputation spanning a 20-year-career, $37 million is not an unlikely nestegg. The same is true for Fairuz, one of six Lebanese singers on the list. The diva does not do commercials but has been performing for over half a century and currently charges up to $500,000 for a concert.

Less convincing were the alleged earnings posted for Elissa and Nancy Ajram. Elissa, whose duet with Chris de Burgh brought her brief international recognition, makes the fourth spot with a staggering $31.5 million. Music insiders say that this is far too high a figure for a singer whose first of her four albums was released in 1999. Nancy Ajram has supposedly clocked up $16.2 million, not bad for a 22-year-old with only two albums under her belt and a $500,000 Coca Cola endorsement.

One notable absentee was starlet, Haifa Wehbe, who along with Nancy Ajram is Lebanon’s hottest selling artist and who was recently voted most popular Arab singer at the Lebanon’s Murex d’Or awards.

Wehbe’s manager, the alluringly-named Cynthia, defended her client’s pulling power by reminding Executive that Haifa, who charges $40,000 for a private concert, has just released her second album and will soon sign her first major advertising deal that would propel her into the big league. With an average of two concerts a week in the summer season, Haifa has to work quite a bit before she sings herself into the top earners list, which is propped up by Zahleh’s favorite daughter Najwa Karam, who has to make do living on $13 million.

Danny Richa, managing director of Impact BBDO in Beirut was elected President of the Lebanon Chapter of the International Advertisement Association (IAA) on March 30.

Richa is confident that, if Lebanon’s political situation changes for the better over the next few months, the sector as a whole will, despite the political setbacks, be able to match last year’s ad figures, which showed growth for the first time in years.

“Lebanon has been here before,” he said. “In any other country the consequences of the crisis would have been much more disastrous.”

Richa believes that Lebanon’s leading advertisement agencies have been spared the current economic and political crisis. “We mainly work with international clients and brand builders who plan their strategies months ahead and so far all kept their promises,” said Dani Richa. “Unfortunately, it is the smaller agencies that suffer.”

Advertisement expenditure in Lebanon has been in gradual decline since 1999, when it peaked at $105 million, falling to $80 million in 2003. According to Stat Ipsat, TV advertisement expenditure decreased from $56 million to $33 million, press advertisement from $36 to $24, while only outdoors increased from $12 to $18 million over the same period.

“Last year we crawled back into the low eighties” said Richa. Hopes were high that growth would continue in 2005. According to some experts however, the 2004 figures did not signify a structural change for the better, but were boosted by the massive multi-media campaign for the Dubai Palm Island resort.

The IAA is a tripartite association representing the interests of advertisers, advertising agencies and the media with over 3,500 members in 89 countries.

In yet another testament to the continuing violence ravaging parts of Iraq, for the second year in a row, the country’s main trade show, dubbed “Rebuild Iraq,” was forced to kick off April 4th in a foreign capital.

In one sense, however, the setting for the four-day conference and expo in nearby Amman could not have been more appropriate: Jordan and last year’s host Kuwait have become the undisputed gateways for a deluge of consumer and industrial goods currently flooding the Iraqi market.

Unfortunately, for many Iraqi producers, the import binge has come at precisely the moment when they are least able to compete, leading to fears and impassioned complaints by some that Iraq’s productive sector is in danger of collapsing altogether.

In a sign of the frustration, one conference participant, who identified himself as “ one of the 25,000 Iraqi industrialists who are out of work,” upbraided an (inexplicably) bemused William Lash, US Assistant Secretary of Commerce, for having been more concerned with implementing a near zero tariff policy than supporting the already fragile domestic industrial sector.

In separate interviews after the conference, both Lash and Dr. Mehdi Al-Hafedh, Minister of Planning in Iraq, defended the Iraqi government’s ultra laissez faire approach to the country’s fragile post-war economy.

“All of our colleagues,” said Lash, “Ambassador Bremmer and all of his team spoke with the private sector and the interim government… When you are trying to attract capital in a very challenging environment you need to be as open as possible. The long-term future for Iraq is for opening her markets and opening her doors to capital, technology, ideas and partnerships, not restricting it.”

For his part, Al-Hafedh was less diplomatic in his assessment of the industrialists’ complaints. “Their problem,” he said, “is to always depend on the state, which is over now. We are in need of goods from outside in order to satisfy the needs of the local market. [Our policies] might be reviewed in the future, but the current need is to encourage imports from outside.”]

Cedars, the second biggest-selling cigarette brand in Lebanon, has witnessed a drop in market share since February 2005, with some shop owners reporting a decrease of up to 50% in sales. The national brand which shot through the ranks of best selling cigarettes in the country largely due to its low price (LBP 750 per packet) is understood to be the smoke of choice for the country’s estimated 400,000 low-wage Syrian workers.

“Between 2000 and 2005, we experienced a 100% increase in sales,” says Antoine Madi of the Regie Libanaise des Tabacs et Tombacs, which produces the brand. “We did no marketing, nor any promotion. Sales went up due to the quality of the brand and its low price.”

Until January 2005, Cedars averaged annual sales of 80 million packets, giving it a 20% share of the Lebanese market, estimated at 7.5 billion “sticks” a year. It by-passed sales of leading international brands Winston, Viceroy, Gauloises and Gitanes, and briefly challenged Marlboro as the country’s leading brand. Since February however, perhaps as a result of many Syrian workers returning home, Cedars has slipped to second place.

“We see two reasons for this,” said Madi. “An increase in counterfeited products on the Lebanese market, which is challenging our product, and the mass departure of Syrian workers in the country since the assassination of former Prime Minister Rafik Hariri.”

Illicit trade and counterfeited products remains a significant problem in Lebanon and the region. “It’s a big issue in this country,” said Naushad Ramoly, head of Corporate and Regulatory Affairs at British American Tobacco’s Levant and Yemen operations. “It’s a lose-lose situation for everybody: the consumers get products of poor quality, the country loses tax income and the tobacco companies suffer a drop in revenue.”

Habib Abdel Massih, the owner of a grocery store located next to a construction site in Gemmayzeh, says his shop has witnesses a 50% drop in sales of Cedars.

“The Lebanese prefer smoking Marlboro, Winston or Lucky Strike,” he explains. “They don’t trust the Regie to provide a quality product. Cedars is predominantly smoked by Syrian workers and the Lebanese living in the mountains.”

Beirut was nominated first city in the Middle East for human resources (HR) by FDI Magazine, a publication of the Financial Times Group. Lauded for the standard of its schools and internationally recognized universities, the survey assessed the Lebanese capital to have the highest proportion of graduates among any city in the region, and came first for the quality of its academic institutions.

According to FDI, Lebanon’s 41 universities and 377 technical colleges have made it a center for regional learning.

“The educational sector has benefited from the country’s democratic institutions, and the fact that there has been no state interference in higher private education,” said Samir Makdisi, professor in economics at the American University of Beirut (AUB).

The survey indicated that Beirut’s high skills pool was a contributing factor in attracting foreign direct investment (FDI), which reached $2 billion in 2003.

“I haven’t seen the empirical evidence tying the level of education with the country’s FDI, but there is no doubt about the fact that a higher level of education contributes positively to economic growth and development,” Makdisi noted.

A high level of education combined with affordable wages by regional standards, make Beirut a city of choice for recruiters.

“All Arab countries like to recruit in Lebanon, especially Saudi Arabia, Qatar, Dubai and Bahrain,” said Dominique Safa, recruitment manager for the Beirut-based HR company Recruiters.

Makdisi painted a more nuanced picture. “Salaries aren’t necessarily lower across the board, there is a disparity. At the top level in businesses such as banks or private institutions of higher education, salaries are higher, making Lebanon more competitive with regards to other Arab countries, but not with the Gulf.”

Beirut was followed by Haifa in Israel, Doha in Qatar and Jubail in Saudi Arabia, as part of the survey designed to select the Middle Eastern Cities of the Future for 2005-2006.

Providing safe mooring for the growing number of floating toys is almost a by-product of Lebanese marinas. More important, even for the showpiece Beirut marina, is the added value they give to the surrounding area. In Dbayeh, the Joseph Khoury Marina cost $70 million to build and provides a much smaller return on the investment than stashing the money in a bank, even at today’s low interest rates. The 700 berths are less than one third occupied. Downtown, the numbers look better – Beirut marina is 60 percent taken up – but the project is seen less as a commercial venture in its own right than as a mega magnet for the rich and the not-so-rich to spend their money in the immediate surrounding areas.

Just as the establishment of the Jbeil campus of the Lebanese American University had the subsidiary purpose of seeking to increase the attractiveness and value of the adjacent hilltop land, so in their own slightly different ways marina operators are trying to follow the same principle.

The Khoury marina is the sexy starlet to attract interest and massive investment in the construction of what virtually amounts to a mini city, immediately to the east and south of the site. Plans include the almost inevitable five-star hotel, three major shopping malls, restaurants and a mass of apartment and bungalow complexes that can be marketed as “overlooking the marina”.

If strolling along the seafront and eating in the waterside restaurants of Cannes or Nice brings with it the bonus of viewing with envy the sleek millions of dollars worth of floating luxury, so Lebanon has adopted the principle with enthusiasm.

Added value

Even the smaller marinas are seen as being commercially more important for enticing customers to the adjoining beach resorts than for generating significant income of their own. If all 35 berths are occupied for the season, the slots at the marina at the Riviera Hotel on the Corniche bring in gross revenue of $75,000 a year. Since the entire coastline is owned by the state, nearly half of this goes straight to the government for leasing the requisites amount of seafront. When another $20,000-$25,000 is deducted for staff and maintenance costs, the bottom line comes in only marginally above break even.

Yet it is viewed as contributing as much to filling the restaurants, bars, pool and sunbathing area as that other prized Riviera asset, its reputation for having more examples of bikini-clad beauty per square meter than most other places in the country.

First down the slipway

Among the first people to appreciate the sex appeal of boats were the operators of Holiday Beach nearly 20 years ago. As part of its progression and conversion from a hotel to a chalet and beach resort complex, the owners, Dog River Holiday and Tourist Center, decided to plow back part of the proceeds from selling chalets and apartments to constructing the marina. It cost LL15 million but that was in the days when the value of all those zeros added up to around $5 million. Some 75% of its capacity of 150 boats is taken up with mainly Lebanese-owned and domestically registered craft. Even so, it attracts some foreign vessels and last month (for lack of space) diverted to Aquamarina a few miles higher up the coast at Tabarja a dozen visiting sailboats that had crossed to the Eastern Mediterranean from Canada, the US, England and Belgium.

Part of the deal for boat owners is the option for an extra $350 a year of five passes into the resort. Although Holiday Beach marina charges are much lower than those further south, this sum is still a relatively insignificant item on the total bill. A ten-meter boat costs around $2,500 a year, just over half what it would cost in Joseph Khoury, Beirut or the Riviera. The rule of thumb is that moorings north of the Nahr El Kalb tunnel are much cheaper than those nearer to the capital.

Follow my leader

A decade later the Riviera followed suit and spent the same amount as Holiday Beach. Cost increases over the years ensured that the Riviera received only 25 percent as much marina for their $5 million. Its more easily accessible location – for Beirutis anyway – allows it to charge $400 a meter, almost the same rates as the much larger Beirut and Joseph Khoury marinas.

In common with most other operators, the Riviera offers free daytime mooring for visitors. In any case, whatever few dollars might be charged pale into insignificance compared with the potential spending power of a boatload of people intent on eating, drinking and enjoying themselves in the resort.

The marina, like the hotel, is owned by developer George Zakhem and his brothers and Nizar Alouf. Although there is potential for some expansion, there are no plans to do so. A bigger space may slightly increase the number of boats but the investment wouldn’t add anything extra to the current glamour quotient.

Aquamarina, another product of the post-war era, cheerfully admits that it doesn’t make a penny out of parking boats. The two-phase chalet and cabina complex was a product of wartime and was built as shells rained down in 1978 and 1984. Construction of the marina brought its own problems too, especially as the choice of following the line of a natural sheltered site incorporated sea depths of up to 15 meters, several times the figure actually needed. Dealing with such deep water increased the costs of developing the adjacent jetties. And in the realm of ‘it’s a small world’ whatever the depth, Aquamarina was built by Joseph Khoury, the contractor who owns the marina that bears his name in Dbayeh.

In at the launch

Seeing the established examples and success as a marketing tool for their companion resorts, the Mővenpick Hotel and Resort in Raouche had the complex designed to include a marina from the outset. When it opened in July 2002, it did, however, reintroduce a different concept of how it gets an income from the moorings. They are sold on 99-year leases rather than being made subject to yearly rental charges. The smallest, 2.5 meters wide by nine meters costs $32,000. The largest is five meters by 20 meters with a price tag of $105,000. In addition, maintenance charges starting at $800 a year for smaller boats cover electricity and water charges, as well as security and assistance from the marina staff in mooring. Before that, Aquamarina had been marketing “berths for life” and succeeded in ensuring that around 60 percent of the marina occupants also have either a chalet or a cabina in the complex.

Up to last month, 85 of Movenpick’s 140 berths have been sold, with the vast majority being bought by clients who similarly have also taken a chalet or a cabina in the resort. Ownership of berths adds to the place’s exclusivity but it also puts restrictions on allowing external boats to visit the marina. They are allowed in only by invitation of an existing owner and do not gain access to the resorts facilities. At Aquamarina, visitors are welcome to moor during the daytime and gain access to dining facilities but like Movenpick the pool and the other facilities are off limits.

Unusually the marina entrance faces south, which makes a part of the anchorage more vulnerable to the ravages of winter weather from the prevailing southwesterly winds. It does, however, have the advantage of keeping the approaching boats well away from the beach area on the opposite side of the complex. Even so, the operators say the innermost sheltered areas are suitable for boats to be left there in the winter.

Although most marinas of all sizes advertise themselves as all-year-round, the unpredictability of winter storms, especially in the past two years, has reduced the only winter moorages confidently deemed safe to Beirut Marina, where $150 million was spent on sea defenses, and Joseph Khoury at Dbayeh.

License to spend money

Winter or summer, the bottom line for the owners is that buying a boat is the same as acquiring a license to spend money. Calculating the first expense – the cost of a berth – does not depend solely on the boat’s length. There has been a military debate for years about the respective merits of having short, fat warships or long thin ones, with each having staunch defenders. In leisure boating that doesn’t apply. Although it doesn’t take a technical expert to figure out that as boat get longer they also get wider, marinas have their own methods of calculating how much space in total a boat occupies. At Aquamarina, it’s the beam, or width of a vessel, that determines the cost of moorage, not the length.

At the downtown marina, every boat over 10 meters long is charged on the number of square meters the vessel occupies. This is calculated by multiplying the length by the width at its widest point. Thus everything afloat is assumed to be a rectangle.

Joseph Khoury operates a slightly different system. Its price range for mooring runs from $350 per meter of length for small boats all the way up to $750 for the super-yachts. In round terms that translates into around $4,000 (including VAT) per annum for a ten meter boat and just under $50,000 for a 65-meter ocean going vessel.

Getting big and bigger

It is those big, big boats that are increasingly concentrating the mind at both Beirut and Joseph Khoury, the only two marinas in the country capable of handling them. Beirut has completely recast its internal mooring layout to cater for these big boats and the guys at Dbayeh, while already capable of receiving vessels up to 90 meters, also have contingency plans for redesigning their interior. Removal of some of the wooden pontoons currently dedicated for smaller craft would increase the capacity for vessels of 25m-30m. Beirut’s capacity was more than halved as far as the number of vessels was concerned, although the surface area covered by boat remained the same.

Still, many mariners take convincing. At Beirut, the Greek captain of a Saudi-owned 65-meter boat was lying outside the marina entrance, determined not to enter because he said there was not enough room. No amount of persuasion from marina officials could convince him. Eventually the owner ordered him to dock the boat despite his reservations. It has since returned more than a dozen times and on one remarkable occasion Beirut hosted four boats of this size at the same time.

The millions flow in

The principle of allying a land home to a mooring spot is operated at Beirut, Holiday Beach and Movenpick and, when the land is developed, will also underpin the Joseph Khoury strategy. Downtown many of the berths have been leased by Gulf Arabs who are awaiting delivery of a luxury apartment in one of the blocks currently under construction facing the marina. Some of them do not even have boats yet but want to make sure they have somewhere to put it.

Joseph Khoury denies access to the public because it wants to maintain the exclusivity of the place for the day when it, too, will be able to offer luxury homes overlooking a guaranteed berth. The management in Dbayeh sees the market for marina use expanding by around 70 percent in the next five years but also reckon that there is neither need nor room for further expansion to accommodate the increased numbers. Current slack will absorb foreseeable demand.

The same view comes from Beirut. A second marina, around half the size of the current 65,000 square meters, is scheduled to be built irrespective of demand. It is part of the overall Master Plan. However, the current operators foresee a demand anyway.

Both marina operators base this optimism on the premise of stability in both Lebanon and the region, as well as the continued switch in spending of Arab wealth from the West. The aftermath of Arab unpopularity in the West following the attacks of September 11, 2001, continues to bring their money back to the region.

Conclusion

The big money that comes along with the big boats is well on course for Lebanon – provided, as ever, there are no major political or security problems. The current slack represented by Joseph Khoury’s 30 percent occupancy and Solidere’s impending new marina will meet foreseeable demand at the high end. Lesser mortals with lesser boats are also well catered for on the northern half of the coast. The South has no marinas and, with ever-possible interference in all forms of shipping by the Israeli Navy, is unlikely to have any time soon. The South also, because of occupation among other things, is still underdeveloped. The emergence of beach resorts in the past few years may well be followed by adjoining hotels and other facilities, such as ‘glamour’ small marinas along the lines of the one that contributes to the success of the Riviera in Beirut. But like every other idea for enhancing the country’s resources and prosperity, it depends on the ‘situation’ being as calm as the sea.

Formality footnote

There may be a good reason why some sizeable floating gin palaces around these shores carry exotic ports of registration far away from Lebanon. If, as Shakespeare maintained, the evil that men do lives after them, the Lebanese have retained a wartime reputation for using boats to smuggle weapons, drugs and people. According to experts in Beirut, this almost guarantees extra checks and time-consuming searches in foreign ports.

However, entering Lebanon with a boat registered abroad is not without its problems. Having completed the formalities to enter, say, Beirut, a vessel must undergo the whole process of leaving the country and re-entering, even if its passengers wants only to go off for lunch in Batroun.

Sizing up an economic sector where few reliable statistics are available is never an easy task. When it comes to real estate though, it can be an even more frustrating endeavour given that the force of rumour and speculation often drowns out the relative paucity of regularly reported, objective indicators.

“Booming Properties,” “Lebanese Real Estate on the Verge of a Boom” … “Boom Time Underway” – these are the headlines that crown the public consciousness, even after the “operational pause” of the post-February 14 period.

Indeed, over the past year, the local press has seen so much “Boom,” that one could easily get the impression that the real estate market as a whole is, well, booming across the entire country.

While this may be true for luxury residential and tourism projects, when it comes to office space in Beirut, the reality on the ground is far removed from the over-generalized, over-hyped headlines: Office space has been, and still is, the soft underbelly, the (literally) half-empty core of Beirut’s so-called real estate revival.

And it is this fact, above several other competing indicators, which provides yet another powerful indicator of Lebanon’s deeply rooted economic woes.

“The residential market bottomed out two years ago and is in a phase of expansion while the retail sector is at the latter end of bottoming out,” explained Karim Salameh, who heads up Lebanon’s Eagle One real estate investment fund that was the first, and still only such fund to invest in performing (i.e. already tenanted) office space.

“But the commercial real estate market in Lebanon, from the office market perspective, is still bottoming out due to an oversupply and the lack of vibrant economic activity that would fill that supply fast enough.”

According to Raja Makarem, managing partner for the real estate advisor group RAMCO, Salameh’s overall estimation is right on target.

“There is a great demand for residential projects but we do not see the same demand for office space…Really there is very little demand at the time being.”

According to Makarem, even as prices have dropped precipitously since Solidere began offering its large stock of centrally located, modern office space, demand has failed to pick up mainly because of that all too familiar Lebanese bogeyman: Politics.

“You did have a large amount of office space that came onto the market in Solidere, so prices dropped…from $450 per meter squared to sometimes as low as $150 in some of the top locations. But it is the political climate of the country that has prevented international companies from coming here and taking up the office space that does exists. That’s the big problem”

Of course, as with many aspects of Lebanon’s political-economy, such is not the case in other competing environs of the Middle East.

In fact, in mid-June, Reem Al Mahmood, the general manager of the Dubai International Financial Center (DIFC), told the El Etihad newspaper that the Center had already inked tenancy deals with 41 multi-national financial firms, including heavyweights like Bear Sterns, Merrill Lynch, Standard Chartered Bank, Credit Suisse and Barclays Capital.

More to the point: Fifty companies were awaiting licenses to take up space in the 4 million square feet development, (of which 65% is greenery)

While there are the obvious bright spots in Lebanon mainly centered around Solidere – more than 35 banks, 500 firms and a number of notable multinational companies are already located in the BCD – oft-quoted surveys that suggest Beirut is at the head of the high-end office market in the region fail to really capture the underlying dynamic that characterizes the sector as whole in the city.

“In absolute terms,” explained Michael Dunn of Michael Dunn & Co, “We do not have expensive office space. In London, [office] rents cost approximately $1,200 per meter squared per annum compared to Beirut which is at $250.

“Dubai,” he continued, “is almost double the cost of Beirut and I know that Kuwait has recently seen some big growth.”

Of course, even the $250 figure, which does not include the overall occupancy costs of taxes etc, is deceiving since that figure mostly applies to the best Solidere buildings like An Nahar and Atrium and the few other high-end office developments, like Gefinor in Hamra, that have relatively modern infrastructure (mainly parking, a large floor plate, fire control and telecommunications) to attract and retain major anchor tenants.

“In the old commercial centers of Beirut, in Sin e Fil and Hamra for example,” said Makarem, “where you saw quite a bit of migration when Solidere came with its new stock, most of this old stock is now rented as it was before the War.

“This means,” he added pointedly, “that rents are sometimes as low as $20-30 dollars per meter squared per year.

Not surprisingly under the circumstances, few owners see fit to refurbish their old office stock.

And because pre-1992 leases are set in depreciated Lebanese Pounds, many tenants of office space, even if their company is no longer operational, decide to hold onto their leases, paying, in effect, peanuts each year for tenancy rights.

The vicious cycle means that although occupancy rates may be high in Beirut, the true occupancy rate, as measured by tenanted space and not just rented space, is exerting a significant, market-distorting drag on the economy.

“I can assure you that nothing in Lebanon is 90 percent occupied… An [occupancy] figure more like 55 or 60 percent may, may seem appropriate,” said Salahme.

“Some owners of empty buildings are non-Lebanese who are ill advised,” he explained. “But the main problem is that some tenants, in Hamra for example, date back to the 1960s. Because of the structure of the contracts, these buildings are not attractive investments – the yield is low and it is not possible to evict current tenants.”

On top of all this, some building owners also intentionally keep buildings unoccupied in the hopes of holding out for better rents down the line.

Although, on its face, such a strategy might seem ill-advised, according to Salameh there is generally little rush to enter an already depressed marketplace because many owners are free from the pressures of debt financing arrangements

“Ownership of real estate was not traditionally debt financed so there is little pressure by banks and others to rent out a building.

“You know the American adage,” he added, “that time is money? Well that’s not true here. Its an inefficient marketplace that is also not transparent insofar as sharing information about rentals or having mechanisms for trading properties.”

For Diab Chidiac, fund manager at Middle East Capital Group, all of these complications amount to a clear strategic imperative: Steer clear of investing in office space.

“We are staying out of the office market for now… We just don’t see that there is a real demand because of the slowdown in the economy over the last ten years really.

“There is demand in Solidere,” he added, noting the estimated 350,000 plus square meters of office space already built by the company and the 1.58 million square meters of total office space that will eventually be built out across the BCD. “But it is for a limited amount of modern office space; the demand is just not big enough to allow you to do a fund.”

And indeed, even as bank BEMO announces an HQ projects downtown, and prime buildings like Atrium and Starco near 100 percent capacity, the reality is that across the whole of Solidere, the office occupancy rate stands at just 65 percent.

Although, according to Makarem, that figure has risen by about five percent since the last time his company conducted a survey almost a year and a half ago, the old list of major unoccupied sites hasn’t changed significantly in the intervening months. In fact, of the top 25 largest unoccupied buildings in the BCD, at least 18 still remain unoccupied, representing almost 43,000 square meters of space.

So even though many observers were pleasantly surprised when the initial occupancy rate of almost 60 percent in Solidere was first published, looking back now the figure seems to stand as a sobering reminder of just how far the sector, and Lebanon as whole, must go in order to rebuild the country’s economy.

“Multinationals are just not rushing to Beirut,” said one prominent local economist who asked to remain anonymous.

“And, as we all know, we don’t have a modern set of laws and practices governing the sector… we don’t even have a modern set of indicators which are vital for a functioning market. Add to that the significant economic problems that exist here and you can understand why the office market is underperforming.”

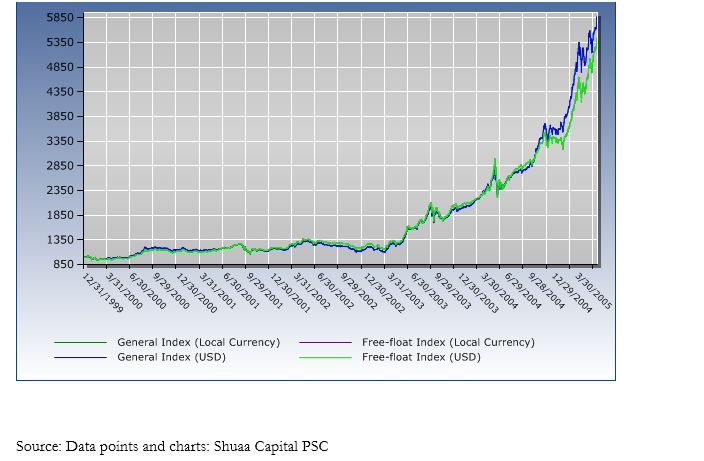

A most fundamental characteristic of speculative gain is that it goes away as smoothly as it comes. So whenever it’s very easy to make money, one must be reconciled to the possibility that it can be lost without much effort or notice. Nowhere is this truer today than in the Gulf stock markets. For just over two years, while most global markets have been mired in single digit action and the tensions in Iraq continued, very few would have bet on a massive rise in the fairly underdeveloped markets of the Gulf. Yet, this is exactly what has occurred. The stock markets of the region have witnessed staggering rises, bringing with them a whole slew of new issues. What fueled the rise and what lies ahead?

The simple truth about Gulf stock markets is that oil has gone from below $10 per barrel in the last couple of years of the 20th century to near $60 per barrel today. This has created a tidal wave of petrodollar-driven liquidity in the coffers of Gulf governments. A recent study by Saudi Arabian Monetary Agency (SAMA) reinforces this notion. The premise of the report shows how domestic spending of “high-powered money” (net domestic expenditure from oil revenues) can create liquidity several times its size (the multiplier effect), demonstrating that, in Saudi Arabia, each new oil riyal of government spending has the power to create up to SAR 16.6, or over sixteen times in additional liquidity. Between 2002 and 2004, net government spending totaled approximately SAR 575 billion, which have had the potential to generate new liquidity up to SAR 10 trillion.

When analyzing this precept, it becomes more comprehendible why GCC markets have spearheaded the world in terms of market growth. Liquidity injected into value creating businesses will raise values in the long term but in the short term inflates and accentuates stock prices.

This scenario has been replayed in the UAE, Saudi, and Qatar. But what stands to be the determinant of how market value will adjust lies in the sustainability of earnings growth, which is set to be put to test in the third and forth quarters of 2005.

As the post 9/11 environment dictated less investments abroad and more cash staying in the region, investors, both sophisticates and neophytes, rushed into stocks. Institutions were only happy to oblige by floating a staggering number of companies. It would be too complex to review the suitability of all Initial Public Offerings (IPOs), suffice it to say that not all the companies that went public would have passed the scrutiny in a more mature market, such as Europe.

The move up in the Gulf IPOs started to resemble, in many aspects the Nasdaq mania of the year 2000, prior to the crash. Shares would double and even triple in the days following the float, and soon, everyone wanted in on the action, so much so that central banks in the region have had to step up oversight, as many financial institutions began lending to speculators, often with reckless abandon. During the float of a large telecom company for instance, it is said that a couple of mega banks lent billions to its most exclusive clients so they could “play”. This environment has led to overvalued markets, trading at well above their acceptable valuation parameters, and pricing themselves in what will eventually prove to be unrealistically ambitious expectations.

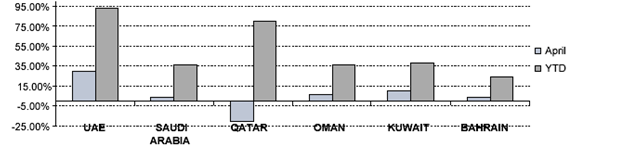

These expectations were further boosted by solid earnings growth by listed companies of over 40% in 2004 with even more robust figures for the first quarter of 2005. Still, a few shady outfits which have found their way on to the public market are trading at 500 times actual earnings. The UAE market, for instance, has gained 86 per cent so far this year. There are, however, question marks over its sustainability and it has been particularly exacerbated by violations in the primary market. Market observers have described the extent of over subscriptions in the local IPOs as “obscene,” prompting the Central Bank to act with unprecedented toughness.

In the case of the record-breaking Aabar petroleum IPO, the total cost per share was Dh5, out of which only one dirham went to the issuing company while Dh4 each was pocketed by the banks that financed the stock applications. This is quite unnatural by any standards. Although markets are generally irrational, they do have checks and balances that ultimately correct blatantly unnatural tendencies. It seems the time has come for these resistance mechanisms to come into play. There are already signs that the party in the stock market may be winding up. A four-day correction on the UAE stock exchange last month wiped off 13 per cent of the market value in one stretch.

There is almost too much public excitement and participation, and this creates a bubble environment. Many newcomers to the “game” will still crow that there is easy money to be made in the area. This attitude is a sure sign that at least some Gulf stock markets are entering bubble zone. There simply isn’t enough institutional money in the form of pension funds and the like, as is the case in developed markets, to sustain them in the medium-to-long term.

The Gulf markets have two major problems in my opinion. One is that they are too dependent on one commodity: oil. The other is that the fundamentals, especially in Saudi, are well behind the market euphoria. Whereas disposable incomes, on aggregate, are rising in the UAE, they are near $25,000/capita, they are stagnant in other countries. Saudi, in part due to Saddam, has seen its per capita income drop to $10,000. So there is not, as in Europe and Asia a well-developed Equity Culture, it is mainly, for now a speculative arena.

The growth in the Gulf is also too closely tied to oil, and while Saudi Arabia has made great progress in solidifying its non-oil activity, it is still mainly a one horse race. This poses great risks if the global economy, especially China decelerates, and oil crashes back into the $25-30 per barrel range, as stock markets will suffer greatly. The two most obvious factors in play in Gulf markets today, and the two most regularly cited as being the main driving forces behind the three-year rally in stock prices, are high oil prices, and low interest rates. The prolonged incidence of both factors has had a magnified effect on equity markets of the region, and is currently most pronounced in the markets of the UAE and Saudi Arabia.

The two seem to have priced in the permanence of both factors. A marked reversal of either one or both those factors would almost definitely have an adverse effect on the markets. In fact, interest rates today are no longer abnormally low, as they have tripled from their all time lows, and are higher today than their pre-9/11 levels. They are generally expected to gain a further percentage point by current year-end. This fact has yet to be reflected in the two markets. Oil prices on the other remain buoyant, although they have recently come down from their peak in April. The direction that oil prices may take from here is harder to predict, and analysts are mixed in their expectations. If the more pessimistic of them are proven right, then a steep correction may prove inevitable. The medium-term direction of interest rates is a foregone conclusion. Keep your eyes on oil.

All in all, the easy money has been made, as one can see in thee accompanying tables. Although the gradual development of capital markets will bring great benefits to the entire GCC area, they are currently in boogie-wonderland in terms of both valuation and excess public enthusiasm with a recent issue – are you sitting down? – 800 times over subscribed. There is too much money flowing into too few shares. With Kuwait’s infamous Souk Al Manakh crash and its consequences still not wiped off memory, investors can hardly be at ease with the current exuberance in the market. Watch out.

Returns: Year to Date, and April 2005 alone.

Saudi Arabia alone looks like mania waiting to deflate…