Compared to the global insurance industry market, the MENA industry is characterized by a severe under-penetration. The demographics of the region are partly responsible for this, as the region’s majority Muslim population is hesitant to purchase insurance products for traditional, religious reasons. However, according to EFG-Hermes, “knowing that the region is under penetrated is not of itself very interesting, unless we understand some of the demographic, cultural, legal and institutional reasons for this under penetration.” The emergence of Takaful is aiding the industry in addressing the cultural issues of the regional market.

What is Takaful?

Takaful is the concept of Islamic insurance, and complies with sharia rules. Historically, various forms of Takaful have been around for over 1,400 years. In an article for Pak-Qatar Takaful Group, Muhammad Ayub writes that, “Takaful is not a new concept in Islamic commercial law,” and moreover, “contemporary jurists acknowledge that the foundation of shared responsibility or Takaful was laid down in the system of ‘Aaqilah’, which was an arrangement of mutual help or indemnification customary in some tribes at the time of the Holy Prophet.” According to leading provider of Takaful solutions, SALAMA Insurance, this system of aqilah laid “the foundation of mutual insurance” in the Muslim world.

The foundation of Takaful is based on the notion of mutual cooperation, assurance, protection, responsibility, and assistance between groups of insurance participants. It can be said that Takaful is a form of mutual insurance. Many insurance companies in the region are adopting Takaful methods as it is sharia-compliant and hence adds appeal to the insurance industry.

Takaful vs. Traditional insurance

SALAMA Insurance states that “the concept of insurance which simply means the pooling of common resources to help the needy is very much in line with the teaching of Islam which propagates solidarity, mutual help and cooperation among members of the community.” Further, SALAMA highlights that “[i]t is important to understand that Islam is not against the concept of insurance but the basis of operation of conventional insurance, which does not meet the requirement of Shari’ah.”

According to SALAMA, “The essence of insurance could be seen in the system of mutual help in the Arab tribal custom of blood money or diyah. Under this system, a victim or the injured party would be compensated by the members of the community whose action had resulted in the loss of life or impairment of the victim.”

Takaful insurance is “the Islamic alternative to conventional insurance products,” according to EFG-Hermes. As it is based on the principle of mutuality, EFG-Hermes finds that Takaful “emphasiz[es] (particularly for life) on co-operation, inter-responsibility, and assistance between groups of participants. In essence, the economic structure of a Takaful company can be seen as a hybrid between that of a mutual insurer and a conventional insurer.” The purpose of the Takaful system, as opposed to traditional insurance, is not to profit but rather to uphold the idea of “bear ye one another’s burden.”

Ayub notes that “[d]ifferent views have been expressed about the status of conventional insurance from the point of view of Islam. An overwhelming majority of the Shari’ah scholars believe that it is unlawful due to involvement of Riba (interest), Maisir (gambling) and Gharar (uncertainty). Takaful, the Islamic alternative to insurance, is based on the concept of social solidarity, cooperation and mutual indemnification of losses of members. It is a pact among a group of persons who agree to jointly indemnify the loss or damage that may inflict upon any of them, out of the fund they donate collectively. The Takaful contract so agreed usually involves the concepts of Mudarabah, Tabarru´ (to donate for benefit of others) and mutual sharing of losses with the overall objective of eliminating the element of uncertainty.”

One distinctive characteristic, according to Ayub, between Takaful and conventional insurance “is more visible with respect to investment of funds. While insurance companies invest their funds in interest-based avenues and without any regard for the concept of Halal-o-Haram, Takaful companies undertake only Shari’ah compliant business and the profits are distributed in accordance with the pre-agreed ratios in the Takaful Agreement. Likewise they share in any surplus or loss from the pool collectively. Takaful system has a built-in mechanism to counter any over-pricing policies of the insurance companies because whatever may be the premium charged, the surplus would normally go back to the participants in proportion to their contributions.”

SALAMA Insurance emphasizes that “the operational framework of conventional insurance is against the tenets of Shari’ah, but not the basic concept of the insurance. Takaful which means ‘the act of a group of people reciprocally guaranteeing each other’ – is based on the concept of mutual cooperative insurance.” Evidently, Takaful is simply a culturally altered form of traditional insurance.

Current growth trends and industry watchers point towards a US$ 10 to 15 billion industry (in per annum contributions) within ten years, but not without addressing critical factors…

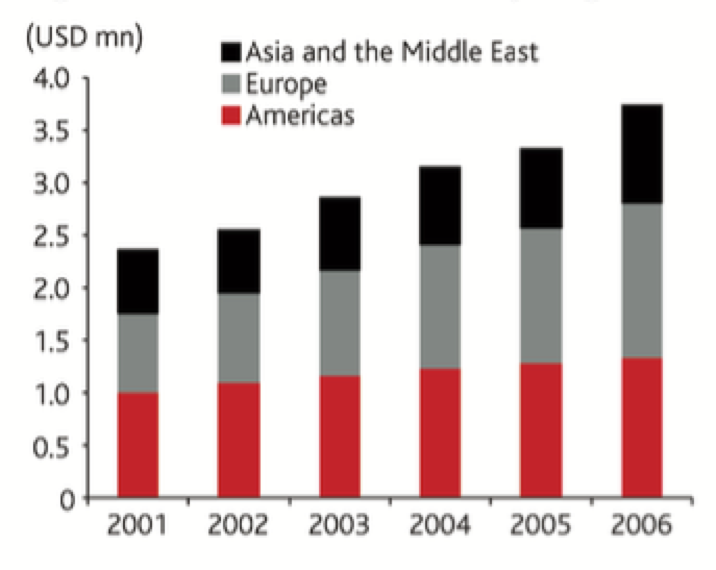

Insurance market influences

Source: FG-Hermes

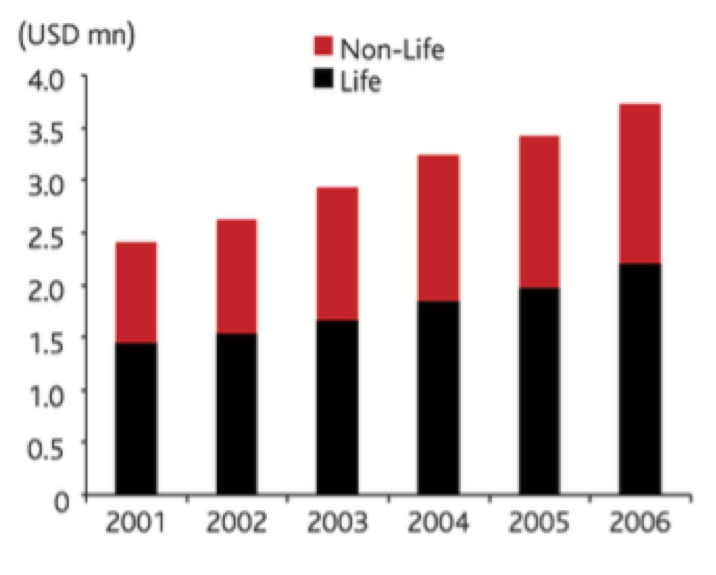

Family Takaful vs. Life Insurance

The cultural characteristics of the MENA region have created obstacles for traditional life insurance to penetrate the regional insurance industry. EFG-Hermes holds that “while life insurance was seen to be problematic initially, scholars looked at Islamic principles of mutual insurance and providing a social safety net. This eventually matured into the concept of Family Takaful, which provides insurance for the loss of family members.”

Interviewed by EXECUTIVE, Dr. Saleh Malaikah, CEO of Dubai-based SALAMA Insurance, said that “the biggest potential for growth is in the life Takaful segment. It is the most interesting and exciting area right now in this part of the world.” Family Takaful, and Takaful solutions in general, are currently gaining momentum in the region, especially in the GCC countries.

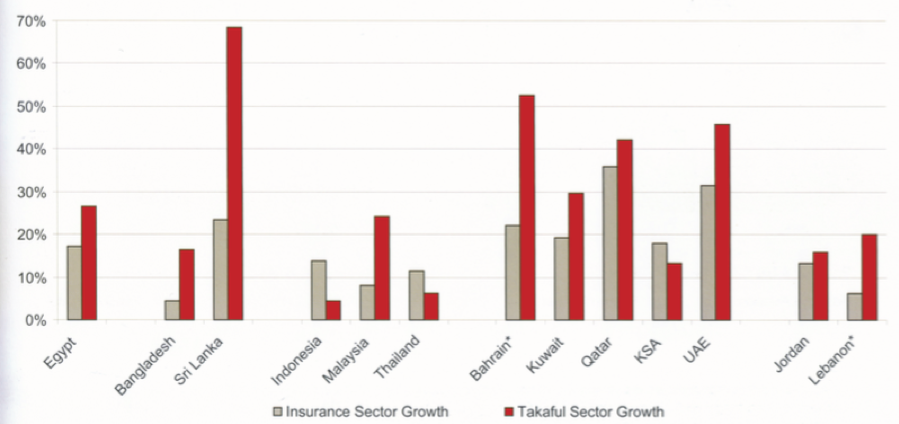

Growth in the Takaful sector has largely outpaced that witnessed in respective insurance sectors…

Growth of the Insurance Sector and Takaful Sector by Country (CAGR % 2004-2006)

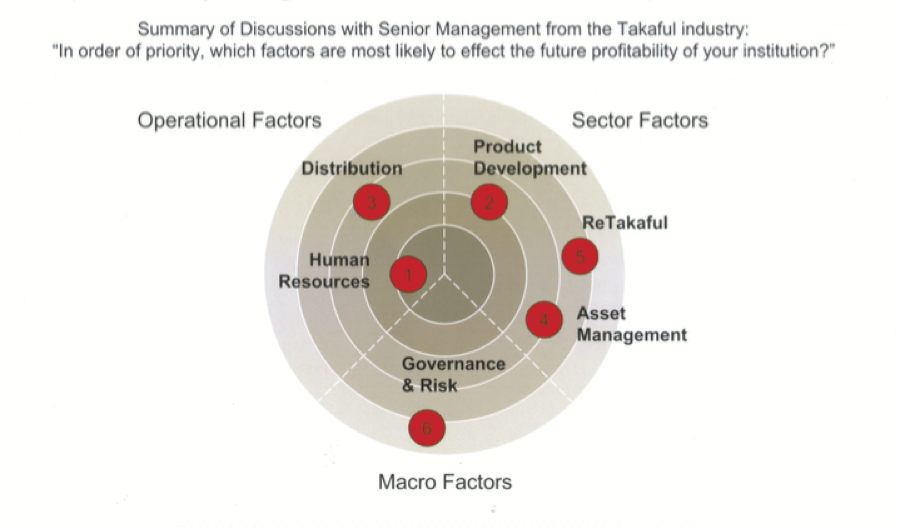

Industry experts have highlighted six areas which are most likely to affect future profitability and growth…

ReTakaful vs. Reinsurance

EFG-Hermes defines the difference between reTakaful and reinsurance rather simply, stating that “Just as a primary Islamic insurer can accept primary business from both an Islamic and a conventional customer, a reTakaful company can reinsure both an Islamic and a conventional insurer. The main difference lies in the management of its investment portfolio: a reTakaful insurer must ensure that it makes only Shari’ah compliant investments.”

Cultural context and ethical appeal of Takaful

EFG-Hermes notes that the “most important feature of the GCC markets, and to a great extent all markets where Islam is an important religion, is the injunction on traditional insurance products from Islam. This injunction is, however, not total: In pre-Islamic and early Islamic society, there was little concept of risk-transfer beyond that of a social insurance obligation.”

Thus, continues EFG-Hermes, “when it is said that there is a conflict between Islam and the construction of insurance instruments, this is an inferred injunction and not a direct one. In fact, the Islamic injunction against some types of insurance is really an injunction against gambling, although in the case of life insurance, there are additional factors.”

EFG-Hermes goes on to importantly accentuate “the fact that these are derived injunctions means that there is considerably more ‘wiggle room’ than there would be otherwise.” This “wiggle room” means “that there has – in most places – been an insurance market operating perhaps unofficially, for a significant amount of time. [And] this has resulted in a section of the population taking out insurance. Nevertheless, clearly the injunctions themselves, as well as the lack of a properly regulated insurance market which is a natural by-product of these injunctions have been strong contributors to the underpenetration of these markets.”

Oussama Kaissi, General Manager of Abu Dhabi National Takaful, noted that because Takaful is sharia-compliant, it acts as “one of the main drivers behind the growth we are witnessing, but its penetration into the western market should remain humble due the demographic distributions.”

Ghassan Wazen, Managing Director of ACE Insurance Egypt, thinks that “people will feel more comfortable when they buy Takaful insurance than any other traditional insurance,” due to its compliance with Islamic law. He also feels that because Takaful has been rather successful in areas like Malaysia and the GCC, he sees “no reason for it to not have the same success here in Egypt.”

Holding that Takaful “is very well developed,” Wazen believes that it “will avoid the religious question because it will make people more comfortable with the idea of insurance.” He also goes further to shed light on the Islamic insurance market in Egypt, saying “there are six companies that are interested in doing this type of business in Egypt.”

Insurance industry leaders feel that Takaful holds an ethical appeal to not only Muslims, but non-Muslims as well. Kaissi finds that “Takaful products and investments in their nature are ethical and that has been proven to be a selling point with non-Muslims entities and individuals,” adding that “the examples are many, i.e. the assets of Christian churches in some Muslim countries are being insured with Takaful operators.”

Michael Bradford, Senior Reporter for Business Insurance Europe, also feels that “Not only will Takaful grow among Muslim customers, but some experts say marketers of the coverage are finding that non-Muslims also are interested in Takaful products. As long as Takaful providers put together dependable products and earn a reputation for quality service, their offerings will be in demand.”

Similarly, Malaikah believes that “Takaful has the potential once it hits a certain critical mass and credibility to really share into the conventional market for non-Muslims simply because it is rewarding from a financial point of view. Because Takaful is saying that this pool of insurance premiums belongs to the insured, and the excess is shared in a certain way between the insurance company and the insured. Logically and economically it is more rewarding to clients.”

If one looks at the actual statistics, one will see in a country like Malaysia, with its multi-ethnic population, unlike the GCC, most of the participants in Takaful companies are non-Muslims. Malakaih highlighted that “Takaful is definitely appealing to non-Muslims because of its economic model that makes it cheaper than the conventional model. Takaful has the potential to attract non-Muslims not only ethically but also economically.”

Osama Abdeen, Vice President of AIG MEMSA, also feels that “Takaful on its own, regardless of being Islamic or non-Islamic, has a certain appeal especially due to the concept of ownership. For example, in the past in Europe, there would be mutual insurance companies … these dealt with policyholders, which had more ownership of the funds, and if that fund performs well, those policyholders will be getting dividends or repays of the profits.”

Takaful is thus appealing because it is based on a cooperative approach, i.e. it is more evident that the policyholder will benefit from bringing good risks from the healthy management of that fund. From that point of view, outside the religion, it has a huge appeal.

“We do in fact witness some companies who are maybe not run by Muslims, and not really Islamic institutions… some of them do opt for Takaful covers,” Abdeen said, accentuating that Takaful “has some certain appeal, and that is the beauty of it. It creates a new concept for other segments to consider; it creates more options for the customer to consider.”

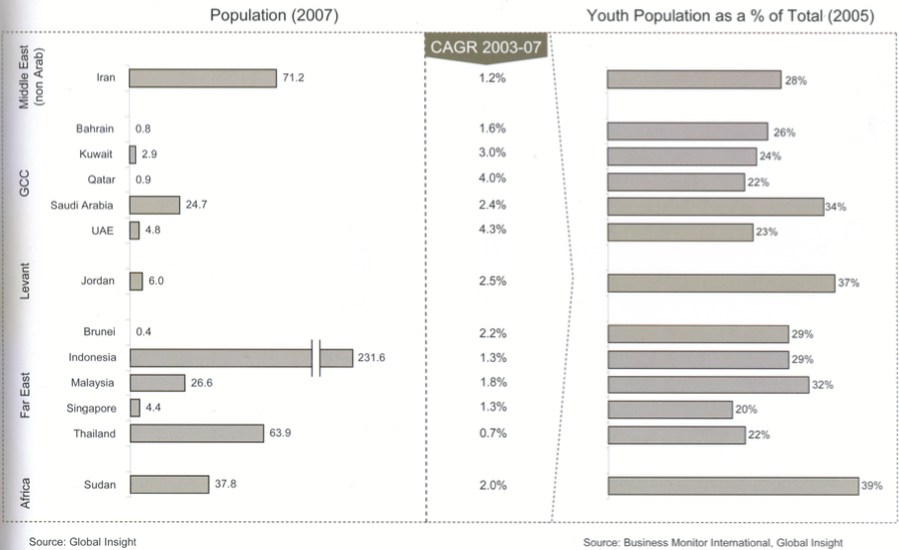

Demographic fundamentals infer significant future demand in many existing Takaful markets…

Current and potential growth of Takaful

Like the overall rates for the regional insurance industry as a whole, figures for Takaful growth rates are not very concrete and easily accessible. Most expect the Takaful market to grow at 20% per year. Ayub believes that “the Takaful business has proved its viability in a period of only two decades. It has been growing at the rate of 10-20% p.a. compared to the global average growth of insurance 5% p.a.”

Ayub also pointed to the regional reach of Islamic insurance, as “[a] large number of Takaful companies exist in the Middle East, Far East, Iran, Turkey, and Sudan and even in some non-Islamic countries. There are over 60 companies offering Takaful services […] in 23 countries around the world. Malaysia has developed ReTakaful business as well. Takaful products are available to meet the needs of all sectors of the economy, both at individual as well as corporate levels to cater for short and long term financial needs of various groups of the society.”

Overall, forecasts regarding the growth of Takaful are rather subjective throughout the industry. Malaikah, for example, personally estimates that “the Takaful market in 2007 was somewhere around $7 billion. It has been growing in the last three years.” In contrast, Bradford finds that Takaful “is expected by some estimates to reach around $7.4 billion worldwide in ten years, up from $2 billion per year now.”

Evidently it is difficult to tell whether the Takaful market is already valued at $7 billion or will be valued globally at around that number in a decade from today.

Kaissi acknowledged this challenge saying, “There is a great potential for the Takaful industry, but the anticipated current and future size of the industry is highly debatable in the absence of empirical data, what we have are pure assumptions that are being based on the state of the economy worldwide and the growth of Islamic finance. There are models that need to be tested and proven and the burden shall be shouldered by all stakeholders, i.e. regulators, investors, board of directors, management and Shari’ah scholars.”

Abdeen added that “For Takaful to grow you need to have stronger capacity from the front and back ends, i.e. from the direct insurer to the reinsurer; we are not there yet on the reinsurance side. We still have small capacities from most of the players in Takaful … maybe we are one of the exceptions because we do have a large capacity at AIG, but other companies have smaller retention limits and they cannot find 100% Takaful reinsurance support. So there is an area for this to grow well to complete that circle.”

Malaikah gave his own estimate of what is happening in terms of growth of the Takaful market, saying “We know the global Takaful industry has been growing at an average of 25%-30%. The trend seems to continue growing at 25% or so. Conventional insurance, by comparison, is growing at around 5%. So if you take 2007, as [your] base year with $7 billion and you’re growing at 25%, it will take you three years to double, [and] six years to grow four times. The estimates of growing to $20 billion or more in five years are not that far fetched.”

Seemingly, Malaikah sees the possible growth of Takaful reaching $20 billion in the next few years as realistic and attainable. Kaissi presented a different take on the Takaful market and its future potential, stating “In the next few years, and with the lack of specific regulatory frameworks for the Takaful industry, the industry shall find itself to be highly fragmented, operating in very competitive markets and competing against well established traditional players. But, it is to be seen that the Takaful industry will prove to be much more receptive to the concept of mergers and acquisitions than its traditional counterpart and as such will consolidate within the medium to long term.”

Also commenting on the global potential for Takaful, Abdeen stated that “Takaful has been established in other parts of the world, like Malaysia and now it is in the UK; so it has a global spread…and it is capable of having this global spread.” He added that he sees Takaful “as more than just a local industry, but rather a global industry.”

Kaissi pointed out, however, that “we find the Takaful operators mushrooming but regrettably some with no clear vision and/or focus on the future. There are several challenges facing the Takaful industry and that while the Takaful industry grows fragmented, it should be able to prove itself as a strong contender in the local and regional markets in order for it to play its intended role.”

Abdeen carefully mentioned the negative aspects of Takaful, as he believes the sub-sector is “established not on a very strong ground with the right capacity,” adding that “at this stage the Takaful market is going into what I would consider the ‘green field operation’, at least within the Middle East; it has been well established in Malaysia and other countries in the world.”

Abdeen also recognizes the “mushrooming effect of Takaful companies,” that are “opening here and there. But there will be a point where service, capacity, and capability will start consolidating or competing. The next level of Takaful growth is extremely promising, and our company AIG has definitely done many studies and taken this route; this will give us more access to various segments. It’s a very exciting period for Takaful.”

In Osman’s view, “there is great potential for [Takaful to grow] because there is a demand from the clients and this can be noticed by the growth rate of Takaful premiums as well as growing number of Takaful companies” in the region.

To what extent Takaful will actually fulfill its predictions is hard to say at this point, as the Takaful industry remains to be quite a small market at present.

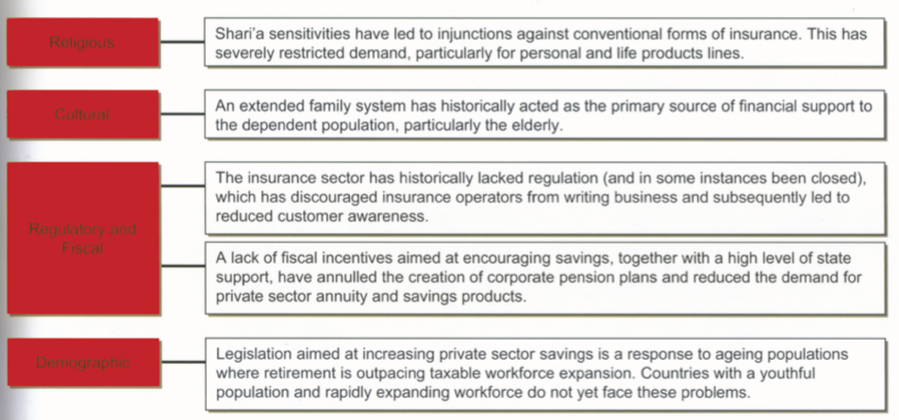

The underdevelopment of insurance in OIC countries can be attributed to a number of factors…

Foreign insurers

According to the industry leaders and experts interviewed by EXECUTIVE, the attitude towards the role of foreign insurers is of a varied nature.

Bradford says he “wouldn’t be surprised if there are further announcements from foreign insurers that new operations will be established in the region.” He also thinks that “[i]nsurers are locating there because there is business to be written in the Middle East and they have the capacity to handle it.”

As a reporter, Bradford believes – parallel to the top players in the insurance industry – that the role of foreign insurers is not one to be taken for granted in the MENA region, stating “foreign insurers are increasingly setting up operations in the region and that is good for insurance buyers. The arrival of foreign insurers can only stimulate competition, which will in turn bring the level of service from domestic companies to a higher level, another benefit for buyers.”

Nazer also thinks that “foreign insures have the expertise from working in the industry for a long time, and this definitely helps in bringing in expertise into the local market of the Middle East.”

In contrast to such opinions of foreign insurers’ prominent roles in the region, Malaikah opined that their role started early on, and since then they have run their natural course. “Foreign insurance has been the early influence in these countries. If you look at the early insurance companies working in the GCC, you will find that they are Western companies. However, local companies are taking over in terms of acquiring the market share.”

Western companies would thus become niche players. According to Malaikah, they had a role in introducing insurance in the market, but they never had the agenda to carry on developing the insurance market and the awareness and becoming the leader. Western companies have been looking at their insurance operations as arms or branches in the area, not as main business. Home grown companies, on the other hand, have been looking at their operations as the main business.

In Malaikah’s view, “It’s exactly like what happened with the banks. Yes, they introduced the service, but now they are niche players.” He went on to boldly state that “Now local companies have the full spectrum of insurance services, so I really doubt there is anything else to learn from the foreign companies.”

On the contrary, thus Malaikah, “the Takaful business is becoming the leader and it is the other way around now; we are seeing foreign companies copying Takaful products and combining them with their range of products.” Not many members seem to have considered this idea, as foreign insurers are coming into the region and finding the only way to penetrate the MENA market is to imitate local traditions and policies.

Abdeen still maintains that foreign insurers absolutely add benefits into the regional insurance industry, as they “bring competition, innovation, talent, replicating success stories of products which were launched in other parts of the world, etc. The whole world is becoming a small village. All these are positive things coming out of foreign insurance companies. I think foreign insurance companies who are committed to be on the ground, to provide the service, will definitely add great value to the most important aspect – the customers first, and to the industry as a whole.”

Contrarily, Kaissi said he “would like to see foreign insurers play a complementary role,” as there is “a lot that we can learn from the multinationals in the areas of IT, back office services and support, corporate governance and more. But, the local and regional players are not short on introducing new innovative products and services to their market and that has been tested and proven. Where we lack as regional players is on the distribution side, we are good at innovation but fail when it is time for execution.”

It seems that Kaissi hopes for foreign insurers to help improve the actual execution process throughout the MENA insurance industry.

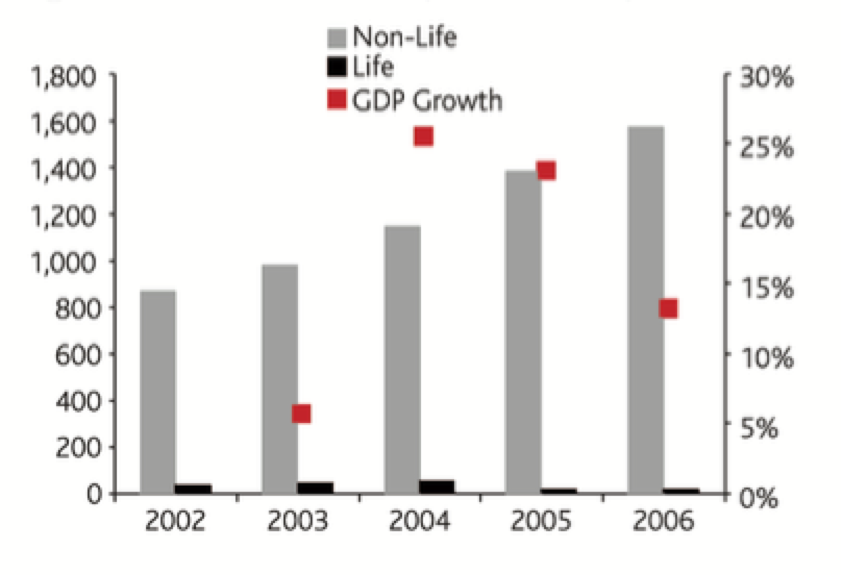

Saudi Premiums (USD million)

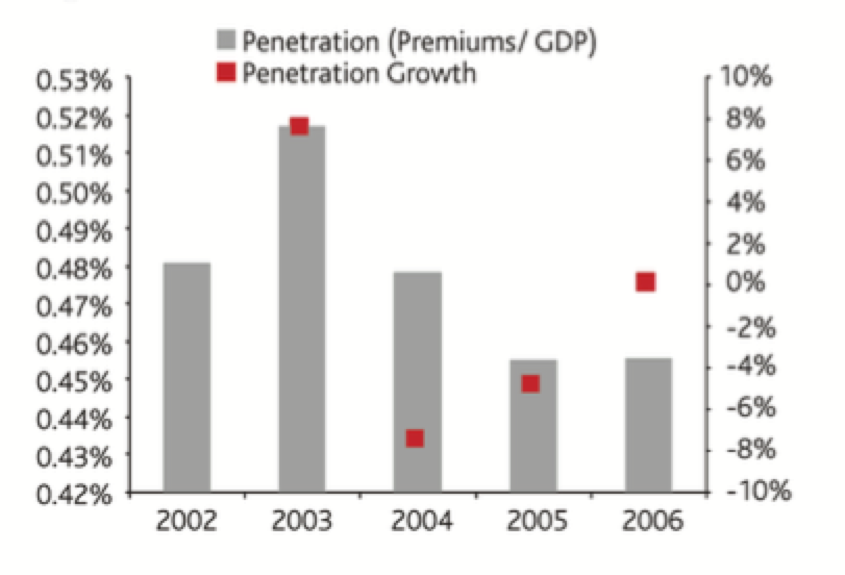

Saudi Penetration

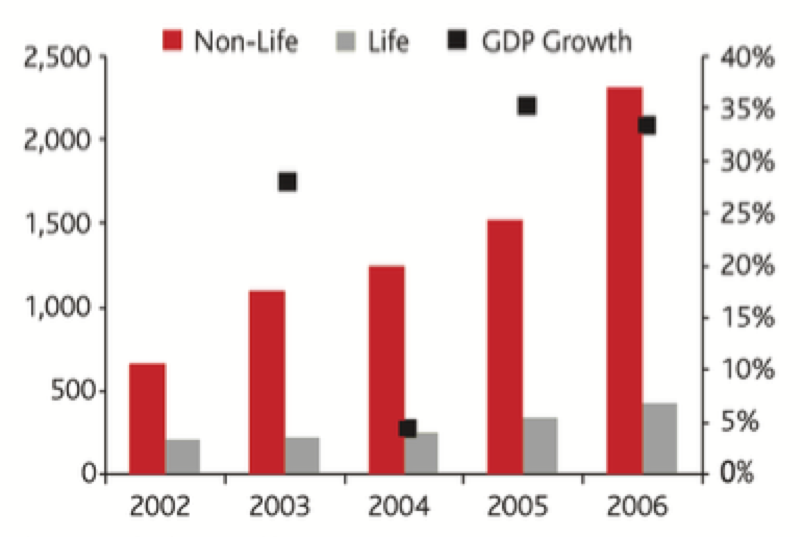

UAE Premiums (USD million)

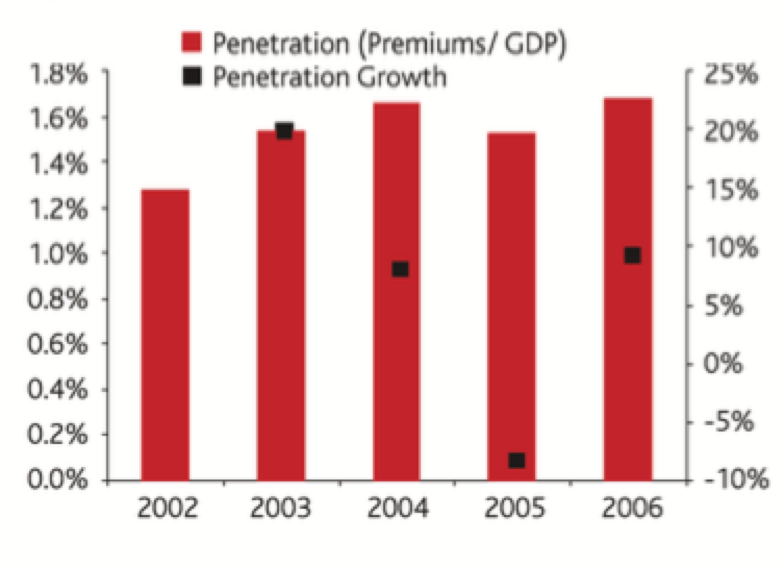

UAE Penetration

UAE Insurance Premiums by Region

Growth of Insurance Premiums

Competition – local and global

EFG-Hermes puts forth that with the recent inception of numerous insurance companies – 47 in the UAE and 13 Takaful companies in Saudi Arabia – “competition is fierce.” It notes that the bulk of insurance companies throughout the region are based in the UAE and Saudi Arabia.

Kaissi feels that in order to be able to compete with the financial might of the global players, reduce back office costs through synergies and increase profitability, MENA insurance companies “should seriously start considering the creation of large regional insurance companies through mergers and acquisitions.” He further noteed, “The only edge we hold on that front is our in depth knowledge of our markets and that still can be acquired by global players in a short period of time.”

Osman finds global competition for regional insurance companies a definite challenge at present, due to short-term implications in the regional industry. “Meanwhile,” he added, “the regional insurance companies are growing considerably, technically as well as financially. I hope to see in the near future very strong regional insurance and reinsurance companies which are in favor the insurance industry as a whole.”

Abdeen presented more faith in the regional industry and its capabilities, trusting it is on its way to being able to compete in the global market, saying that, “the first step has been done, which is quite interesting, where the insurance companies are capable of writing the risks located or emulated from their region. In the past, most companies had very small retention, and really the business or the risks of high capacity were heavily reinsured. This statement remains correct as we speak at present, but we have seen moves by some local companies to increase their capacity; we have seen companies who decided to set up operations within the Middle East region, which on its own increased the capability of the region to be able, to a certain extent, to write its own business. This is the first step to emerge as an international, global player in the region. So we are still in step one, but as a region, we have come a long way on this.”

In terms of the Saudi market, Nazer thinks that due to the fact all Saudi insurance companies are required to be licensed and publicly listed, that “The Saudi insurance market has quite a mix between local players, regional players and global players.” To this he added that, “Local companies in general have done quite well.”

It seems performance of the Saudi insurance market, valued at $1.6 billion (in total insurance premium volume), can be accredited to the regionally noted organized regulation frameworks which were recently put into action. Evidently, Saudi Arabia, as well as the rest of the GCC, will not be able to compete with the global insurance industry until they firmly establish themselves in the region first.

Investing the funds

The issue of where insurance companies are investing their funds is one of great interest. Opinions seem to vary, which may be due to the fact that, according to Malaikah, “Insurance companies are conservative by nature, and do not take very big risks.”

Concurring with this opionion, Kaissi believes that “Regional insurance companies usually follow wisely a conservative approach to their investment strategies. In the Gulf region for instance, we have witnessed about a year ago a clear shift in investment strategy for some companies divesting from the heavy position they were holding in the equity market to the real estate market after the volatility that was witnessed during the past eighteen months in the stock market. It is anticipated that 45% of the cash available to regional insurance companies is invested in the form of cash deposits and government bonds varying in duration in order to meet their immediate liabilities.”

Kaissi also underlined that “The regulatory framework in certain regional jurisdictions places stringent rules on investment guidelines outside their natural borders.”

Similarly, Malaikah feels that “Most investments are in fixed income instruments, with provisions to invest in equities and in real estate. Unfortunately, we are facing a period now – or at least where currencies are pegged to the US dollar – of negative real interest rate due to dollar weakness, making interest rates below the rate of inflation. This is more exaggerated in the GCC countries. It is really an issue that needs to be addressed. Investments in equities and real estate, albeit in much smaller proportions than fixed income securities, are gaining popularity.”

Nazer’s view on investments in the insurance industry draw parallels to these perspectives. “Investments are mandated by the regulators, where there are very specific criteria that insurance companies must follow, i.e. a breakdown in relation to assets, a breakdown in relation to geographic allocation, etc. Every insurance company would have a different ranking. It depends if you are in a short-tail business or a long-term business, and this is how you would define your asset location and the period that you would want to lock in the investments. In the health insurance industry, it is a short-tail business and it requires payment to hospitals right away, so you need to define your strategy based on your line of insurance,” he said.

In addition, Abdeen believes, “some companies have perhaps over invested in the volatile stock market. In one year there were huge profits, but when the correction movement on the stock market occurred, it had an adverse impact on the investment income. I think multinational companies do invest across the globe, locally and internationally.”

Abdeen firmly feels that “Local companies also invest, [but only] after the regulation processes have been implemented in each country. But in my opinion there should be a balance, a balanced way of investing and regulating because the investment aspect is an important part [of the insurance industry].”