T he rating agency just won’t quit. Two

months ago Standard & Poor’s

(S&P) threatened that if the government

didn’t do something about fiscal problems

running wild, Lebanon would be downgraded

later this year. S&P’s latest incoming

targeted the country’s most cherished sectorthe

banks. Rest assured: The recent warning

did not highlight problems within the banks.

Whether or not the government heeds S&P’s

earlier signal will determine to a great extent

the problems that banks may face.

The agency went after financial systems

around the world that are vulnerable or

already tasting deterioration of credit quality.

If, by chance, defaulting on loan payments

reaches critical mass, banks could experience

a credit bust. Out of 15 banking systems

cited by S&P, US banks’ credit exposure

could be hit if the booming economy comes

to an end with a hard landing. Japanese banks

cannot prosper as the country’s recovery

from its financial crisis a decade ago is moving

slowly. Lebanese banks, on the other hand, are operating

in a feeble

economy and if it’s

not resuscitated in the

near future, loan portfolios could be in jeopardy.

“Lebanon is a special case,” says

Navaid Farooq, S&P’s sovereign analyst for

the Middle East and North Africa. “It’s about

macroeconomic conditions. We’re not concerned

about the banks themselves as much as

the environment they operate in, which is

riskier due to the government’s severe fiscal

imbalances.”

Relying on a rescue team to pull the

economy out of its dismal state is in question.

The administration, in office for two

years, put together a fivt:-year plan that

included lowering the debt, correcting fiscal

imbalances and stimulating growth.

Instead, it let debt to GDP climb from

118% at the end of 1998 to 140%. In the first

half of 2000, the budget deficit reached

53%, way above this year’s target of

37.3%. Economist Intelligence Unit reports that GDP growth fell to – l % in

1999 and predicts only 0.5% this year.

Right now there is a glimmer of hope that the

elections will bring in a new government able

to repair the crippled market. But the next government

has little room to maneuver. After debt

servicing and salaries and wages, the government

can only play with about 15% of its

expenditures – something they can’t reduce

since it’s their meager contribution to growth.

Raising taxes again to increase revenue

would bury the economy even further.

Many analysts believe emergency action

must be taken. ”The most important thing is

for the government to get money today,”

says Marwan Barakat, head of research at

Banque Audi. “It must relieve debt and debt

servicing as soon as possible.” He suggests

selling mobile phone licenses – $2. 7 billion

was lost when the government rejected offers from LibanCell and Cellis – and

picking up the pace on privatization. But

once a new government settles in, it might

be too late to make an impact this year. And

some wonder whether any Lebanese

administration can unite and generate political

will to implement solution~ “I don’t pin

any hopes on anybody anymore,” say~ um: analyst.

“We have to be realistic:

All government

policies will be dictated

by political interests, not

political will.”

On the upside, unlike the

wayward government,

most banks have the discipline

to prepare for the

worst. “Most of the banks

are low on lending compared

to other countries,

which gives them a lot of fat,” says Andrew Stephens, head of retail at

Credit Libanais. “And most have significant

assets in Lebanese T-bills. The banks do not

face deep problems.” By the end of June, the

loan-to-deposit ratio for the sector was 42%.

And expecting hard times, banks have

become less generous handing out money.

Loan growth fell from 20.5% in 1998 to

12.7% last year. Lending up to the end of June

increased only 3.7%. The banks are also high

on liquidity: Liquid assets to total assets

stood at 68% in the first half of 2000.

Creating a cushion using conservative tactics

makes it unlikely for numerous banks to

fall if defaulting on loans accelerates. “The

banks will get into problems only if they stop

lending prudently and start lending outside

certain banking criteria, as a couple of them

have done,” says Stephens. One case was

Inaash Bank. Found with bad loans and

fishy lending in violation of regulations, the

central bank stepped in and sold it to Societe

Generale Libano-Europeenne de Banque.

If obituaries are rare, one area will be difficult

to defend: profits. “Not many banks will

fail in the near future,” says Bassam

Yammine, senior manager of corporate

finance at Lebanon Invest. “Banks have

enough ammunition, especially the large

ones, to continue. I’m worrying mostly about

the bottom line.” There have already been

attacks on banks’ earnings. Spreads have been pinched in recent years. With interest

rates on two-year government paper falling to

14%, stiff competition has kept deposit rates

up (around 12% on LBPdeposits). The economic

slowdown has put pressure on growth

in deposits and assets. An increase in deposits

fell from 20% in 1998 to 11 % last year. Nonperforming

loans are now starting to move up.

Doubtful loans to gross

loans inched up to 14%

last year from 13.75% in

1998. In June, they

climbed to 15.1 %.

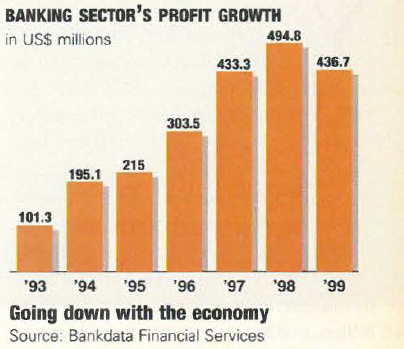

After profits dropped 13%

for the sector in 1999 – a

blow after 40% average

annual profit growth

between 1993 and 1998 -many predict that earnings

will experience a similar fall this year. “Now adding

deterioration of asset quality and an increase

in provisioning to revenue stagnation and

tight spreads, profits will drop between 15%

to 20% this year,” says Yanunine.

Finding solutions for the banks to generate

better earnings will not be easy. Banks are still

heavily investing on a safe bet: Thirty-five percent

of assets are in T-bills. But with the

spreads in a vice and the option of increasing

lending to the private sector with higher

yields a no-no for now, the banks are in a catch

22. “With the loan ratio this low, banks cannot

make up the thin spreads on lending,” says

Stephens. “That’s about it for the bottom

line.” Banks have been moving more into

retail banking to help beef up non-interest

income. “It’s important for the banks to move

into products and services as profitable activities,”

says Haroutiun Samuelian, vice governor

at the central bank. “In the early ’80s,

non-interest income for US banks took up

20% of their revenues. Now it’s a 50/50 split

between interest and non-interest income.” But

retail banking has yet to pay off. It requires

high volume, which is difficult in a small

market, while other non-interest tools, like letters

of credit, have been pulled down with the

recession, damaging gains coming from new

products and services to make a difference.

As in any sector, downtime means lowering

costs. “Banks must focus on restructuring,

cleaning up, cost cutting,” says Yammine.

Banque du Liban et d’Outre-Mer, Lebanon’s

largest bank and one that is still enjoying

healthy profit growth, is not only conservative

in lending but has focused on reducing

expenses. Its cost-to-income ratio dropped to

34.7% after the first six months this year

from 38.4% at the end of 1999. But other

majors more aggressive expanding on retail

find it more difficult to contain costs. Banque

Audi’s and Byblos Bank’s cost-to-income

ratios have moved up this year. ”The human

cost is already low compared to other countries.

Plus, many banks, out of necessity, are

investing in new services which all have

costs,” says Stephens.

If economic agony is prolonged, the pace of

mergers and acquisitions may pick up-especially

small and medium-sized banks swallowed

up by larger ones. Out of the 63 banks

operating in the country, the top 20 carry the

most muscle. Over 90% of total profits are in

the top tier, which leaves less room for the rest

of the banks’ earnings to fall. “With consolidation,

economies of scale can help,” says

Samuelian. ”The sound ones will survive

while the weak ones will not.”

Going abroad would help. But up to now

Lebanese banks have been hesitant to fan

out across the region. This could change.

Syria, with a state-owned, dilapidated banking

system, is opening up. It just established

free-trade zones and three Lebanese banks got

the green light. The problem is having to wait

for the entire Syrian market to open up.

“Syria is the place,” says Stephens, “but not

tomorrow. Maybe the day after tomorrow.”

What’s more certain is that if banks

remain mostly entrenched in the Lebanese

market and the economy continues to falter,

it may take time for them to see glory days

in profit growth again.