Ever since the Golden Arches first lit

up the night sky in Dora in

November 1998, the Lebanese just

can’t seem to get enough of that all-American

fast-food chain. Beirut’s five

branches of McDonald’s are almost always

packed to overflowing: a gaggle of kids

dipping fries in ketchup and parents sinking

their teeth into a Quarter Pounder with

cheese, while the drive-thru outside does

just as brisk business. But wait a minute, this

is not an article about the Zoghzoghi’s success

in bringing the Big Mac to Lebanon’s

shores — in fact they have repeatedly

declined to be interviewed. This is the

story of the family in charge of distributing

all McDonald’s consumable products: the

Obegis. Ring a bell? McDonald’s is just one

of their most recent business associations

and is sure to beef up their business even

more. The Obegi family dynasty has

already made it into virtually every

Lebanese home. Look around; you’re sure

to find a detergent, soap, canned food or cosmetics

which Obegi Consumer Products

(OCP) supplies and distributes.

The Obegis’ business is grouped into

three main activities: consumer products

(OCP), chemicals (Obegi Chemicals, OC)

and banking (BEMO). Their size is

impressive. OCP chalked up consolidated

revenues of $71.8 million last year, while

OC did even better, hitting $82 million. At

the same time, BEMO’s assets reached

$381.5 million (see box). As enviable as

those numbers might be, the Obegis didn’t

get there by sitting comfortably in the back

seat. But the family’s thirst has yet to be

quenched; they continue to expand the

activities of their mushrooming business.

It all started in Syria when Yordan Obegi,

grandfather of the current division heads, began

working with BASF in

1905, the number one

chemical company in the

world, and became its agent the following year. OC is still BASF’s

sole agent for Lebanon, Syria and Jordan. In

the late 40s, Obegi entered Lebanon importing

carpeting and all types of furnishings for

the home as Obegi Better Home. Its cooperation

with German manufacturer Henkel

began in 1954 with the importation of Pre, the

predecessor of Persil. Ever since, Obegi has

maintained a strategic alliance with Henkel

— which had revenues of about $42 billion in

1999 — importing, distributing and then a joint

venture manufacturing core products such as

Persil, Der General, Pril and Nice.

“Our partnership with a multinational like Henkel

makes us sustainable for the long run and

gives us access to their know-how and global

expertise,” says Georges Obegi, president

and CEO of OCP since 1994. With

Henkel’s internationally known brands,

OCP has been able to penetrate Syria and

Jordan, and its sights are set on Iraq.

With OCP in the driver’s seat, its market

share for Persil increased from 12% to 48%

from 1985 to 1996. Henkel and OCP then

entered a joint-venture deal, similar to their

agreement prior to 1971, though OCP kept

control of both marketing and distribution.

Backed by strong international brands, the

ability to manufacture locally and solid distribution

that doesn’t rely solely on wholesalers,

OCP has grabbed strong market

shares in its core Henkel products.

OCP is big on detergents and cleaning products,

with a large market share in two core

brands: Persil and multi-purpose Der

General, which are manufactured locally.

Persil still holds the lion’s share of the market

equally with Ariel, despite having

recently lost ground to Syrian imports like

Madar Super Topper, Modhish and

Nourass. How important is that? Very, now

that OCP holds a 42% share of the $56 million

local market for low-foam detergents

with Persil. OCP also leads the multi-purpose

liquid detergent market with its second

core brand Der General with a 65% share.

That compares to 22% for its main competitor

Ajax, which is distributed by the

Abou Adal Group. Though Ajax has a sizable

market share, it is an imported product.

“We’re at a disadvantage against locally

manufactured Der General because they

save on shipping and import duties,” says

Raymond Abou Adal, president and CEO of

the Abou Adal Group.

With its 9% market share for Palmolive,

Abou Adal does compete against Fa, for

which OCP has a 15% share. But this is a market

dominated by Unilever products, such as

Lifebuoy and Lux, both of which are manufactured

by Unilever-Fattal, Dove and Good

Morning. That gives Unilever an estimated

20% market share, while Procter & Gamble

(P&G) holds a 17% share with Camay and

Zest.

Unilever Levant (UL), a locally based

firm covering Lebanon, Jordan and Syria, is

part of the multinational giant Unilever with

$45 billion in revenues last year. Established

in March 1998, UL has a five-year plan to

grab a 25% market share in the Levant, or

$150 million of a $600 million consumer

market in the areas where they compete,

according to Abdul Jessani, UL’s chairman.

“These are the guys we have to watch for;

they have strong brands like Sunsilk shampoo,

Lipton tea, Signal and Close Up toothpaste,

Comfort fabric softener, and others

that can really take off with their undeniable

marketing expertise,” says Obegi.

But while Lux matches OCP’s market

share in soap with a 10% market, according

to AMER research firm, its multi-purpose

detergent Jif has so far underachieved

against Der General with only a 2.8% market

share. P&G is their main competitor on

OCP’s remaining core products with Henkel.

Locally manufactured Nice, a high-foam

multi-purpose powder detergent, has

a 19% market share versus the 65% share of

locally produced Yes, according to Nadim

Tabet, CEO of Transmediterranean, P&G’s

local distributor. Against OCP’s dishwashing

liquid Pril, P&G’s Fairy has a commanding

75% market share, says Tabet.

Obegi says he will take up the challenge

against P&G primarily through greater visibility

and increased presence in the market.

The last of the core products is one that

belongs to the Obegis independently of

Henkel. That’s Al Wadi Al Akhdar, a 50%

locally produced canned and frozen food

brand. Whenever the foodstuff is not locally

available, the product is toll manufactured

in Hungary and Belgium and imported

into Lebanon. Al Wadi Al Akhdar is

OCP’s own-labeled brand, similar to G.

Vincenti & Sons’ Maxim’s brand.

Like Vincenti, OCP manufactures and exports Al Wadi Al

Akhdar to the US, Europe, Brazil and the

Gulf. Exports of this brand represent 50% of

local production and 25% of the brand’s

total turnover. The entire range of core products

represent 60% of OCP’s turnover.

The other 40% of OCP’s revenues are generated by the sale of a range of auxiliary

products, including Hajdu Bihar Kashkaval

cheese, alcohol like White Horse and

Carlsberg beer, frozen foods and cosmetics.

Here, Vincenti and Fattal compete better as

this represents their core products. From

1997 to 1998, OCP increased sales 9% in

these frozen foods, which represent 4% of

the company’s turnover. OCP abandoned

the sale of selective cosmetics in Lebanon

this year in favor of mass cosmetics like

Rimmel and Diadermine, which represent

10% of revenues on auxiliary products.

OCP did it for a good reason: mass cosmetics

target a larger audience, which is in line

with its other products.

So how has Obegi fared since he was put

in charge of marketing and distribution?

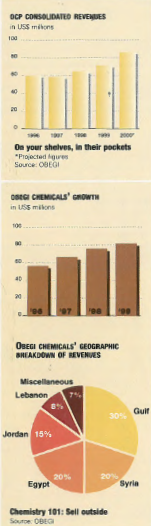

OCP’s consolidated revenues have grown

from $60.5 million in 1996 to $71.8 million

in 1999. And he expects that will rise to $83

million as a conservative figure for this year.

“The Obegis have an empire, they are very

respectable, and they get a lot of merit for

developing products,” says Tabet.

Now here comes the exciting part of OCP.

Last June the Obegis took over manufacturing

in Syria from a previous Henkel licensee

that was producing Persil. There they have

embarked on an expansion plan. OCP added

the manufacturing of Nice, Der General, Pril

and recently launched Al Wadi Al Akhdar and

Yemel fabric softener. Almost $1.5 million,

or 2% of OCP’s consolidated revenues, were

generated in Syria, where Henkel has an

option to buy into the manufacturing operations

after two years.

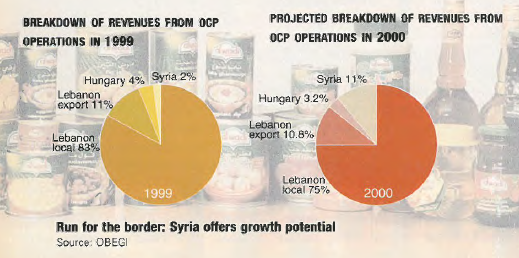

This year Syria is expected to account for

11% of revenues with an additional

$8 million to $10 million. And Obegi

projects at least another $25 million in revenues

in three years. The main office is located

in Aleppo, the Obegi family’s original

stomping ground, while another was set up in

Damascus. With a national sales force of 30,

OCP plans a uniform and aggressive product

launch across the country.

The starting point is a 0% market share

for Der General and Pril, and just a 5% share

for Persil. However, since a July launching,

OCP has grabbed a 7% share of the $26 million

high-foam market with Nice. Could this be a sign of things to come?

The total powder detergent market,

which is at $82 million, is up for grabs.

Nice is already doing well for a few reasons.

“The three-in-one detergent concept is new to

Syria and is designed for low-income people,”

says Obegi. He also has a marketing budget

advantage. Local production relies heavily on

labor so the products are uneven in quality and

quantity, while OCP’s factory is highly automated

and meets international standards.

The competitor for Persil is UL’s Omo.

The retail price for Omo is 235 Syrian

pounds, whereas Persil is at 280 Syrian

pounds for a 2.7kg pack. So shouldn’t

Obegi lower its price to better compete?

Persil is priced at 35% to 40% lower than

the Lebanese product, which is proportional

to the gap of GDP per capita

between the two countries. For now, Obegi

has no intention of lowering the price significantly.

He doesn’t want to widen the gap

in prices between the Lebanese and Syrian

product because of trans-border trade. That

would allow wholesalers to buy in Syria and

sell at cheaper prices in Lebanon. “Omo

started on the high end, then dropped their

prices 17% and it didn’t increase their

sales volume; on the contrary, it damaged

their brand,” says Obegi.

OCP’s Syrian operations are by no means

the first outside Lebanese borders: another

4% of turnover comes from operations in

Hungary. Under the name Dove Cosmetics,

OCP acts as the exclusive marketer and

distributor for suppliers like Chanel,

Clarins, Guerlain, Orlane and Lancaster.

The company also operates in Jordan,

where it markets Henkel products only,

such as Dixan, Persil and Pril. Total Henkel

detergents in Jordan represent about 13.8%

of the market share, according to AMER,

compared to a 19.6% market share for

Unilever products such as Surf and Omo.

While OCP’s products have long been household names, few probably know that OC

is a larger operation in terms of revenue. Its

main activity is the distribution of industrial

chemicals, from suppliers like Egypt’s Dow

Chemicals, BASF or US-based Hercules.

OC supplies plastic, polymer, solvent and

thousands of other chemical products to

industries. Dealing with a high-risk commodity,

the company bears the responsibility

of product selection, shipping and/or storage

and delivery to the client. OC also explains

the nature of products on behalf of the

producer, as well as giving alternate products

and solutions for industry. For these services,

the company collects a hefty fee.

OC increased revenues from $56.7 million in

1996 to $82 million last year. Not bad for a

company not involved in marketing, manufacturing

or retail. OC has eight warehouses

(4,000 m² each) in the Middle East and one in

Brussels, employing some 120 people.

The largest chunk of business comes from the

Gulf at 30%, followed by Syria and Egypt

each at 20%, Jordan at 15%, while Lebanon

accounts for just 8%. “Lebanon is a small market

for a regional company like us,” says

Yordan Obegi, managing director.

But is OC content with distribution? No.

The firm is moving into manufacturing in

Lebanon for some products from its factory

in Bauchrieh. But the bulk of manufacturing

will be done in Aleppo, Syria, where it will

begin making chemical products for textiles

and printing inks for industrial use in two months.

Within a year, another factory will open in

Egypt to produce PVA, used in paint and

adhesives. A joint venture between OC and

an Italian company, the plant required an

investment of close to $10 million. OC will

manufacture under license.

Not only is OC catering to the needs of Syria

and Egypt, where textiles and paints constitute

a big market, but it will also save on import costs.

That’s important for an industry where profit margins

are a slim 2% to 5% on average.

Now that you’ve seen the size and breadth of

their business, you’d think the Obegi family

already had their hands full? Wrong again.

Like we said at the beginning, OCP has been distributing

all the consumable products for McDonald’s five

franchises since November 1998. If history

is any indication, less than 5% of McDonald’s businesses fail

worldwide compared to an overall failure

rate of 65% for restaurants in the US.

This should represent a healthy stream of

income for OCP. Because McDonald’s doesn’t mix the business of the franchisee

with distribution, Zoghzoghi recommended

OCP. “What’s interesting about this

account is the credibility and expertise it

gives us, because we are monitored in a very

strict way,” says Obegi, explaining that

McDonald’s has tight regulations on the timing

of delivery, hygiene, storage temperature

and stock level.

OCP built storage facilities within its existing compounds for its business

with McDonald’s; it is also using existing

facilities to freeze OCP products to benefit

from economies of scale. Although these

operations posted losses for three and a half

months in 1998 and broke even in 1999,

Obegi expects to be in the black in 2000.

Ubiquitous in nature, OCP products have

invaded the homes and lives of just about

every Lebanese consumer. The same is now

happening in Syria, with Iraq next on the hit

list. Will the Obegi dynasty be resilient

enough as it conquers more territory to defy

the odds that all empires eventually fall?

Top of Form

Bottom of Form

A weakness in Obegi’s operations?

Everybody’s heard of Obegi Better

Home, which sells upholstery, carpeting,

wall covering, office furniture, furnishings,

decorations and others.

Maybe fewer have heard of Obegi

Audiovise for audio-visual equipment,

acoustical and telecommunication systems

trading, or Byblos Teppish Fabrik

(BTF), which is mainly involved in carpet

manufacturing. Collectively, these businesses

are on a negative growth path.

Their total revenues decreased from

$14.5 million in 1996 to $9.9 million in

1999. The Obegis are only managing

some of them, and they don’t constitute

part of their core activities.

These operations appear to be nothing

more than excess baggage for a

family firm that is showing tremendous

growth. Georges Obegi said the family

has no intention of divesting those

businesses. “We are reinforcing and

strengthening those companies,” he

says.

Obegi Better Home is undergoing

restructuring to enhance quality of service.

Previously under one umbrella,

management for office furniture and

everything under the home is being

separated. Obegi is also focusing

more on the upper-end market with a

consistency in price and marketing via

direct mail and some press.

As for Audiovise, the decrease came as the

firm got out of retail, continuing only with

distribution. Obegi got rid of Supra TV

and is focusing on high-end German

manufacturers Kenwood and Loewe.

According to Obegi, BTF was in

small part responsible for the decline

but will have a larger effect in turning

things around. There are plans to

expand its export markets for its

machine-made rugs from an estimated

25% to 50%. The expansion will hit

South America, Europe and the Gulf.

Then again, these businesses are so different

from the family’s other operations,

are relatively small and receding

even further. Why not just dump them?