Imad El-Hajj, president of American

Underwriters Group (AUG), probably

never thought of it, but his job is much

like that of a priest. In times of trouble, anxiety,

and worry, people come running to

him. AUG is among a handful of insurance

companies that provide war-on-land

coverage — insurance for damages caused during

a military conflict.

Demand for

these policies increased 25% in recent

months, with tension building prior to the

Israeli withdrawal — not just in the South but

in Beirut and even Jounieh. The price of premiums

shot up by almost a third. Recently,

a professional syndicate requested that its

medical insurance coverage be extended to

include injuries sustained during wartime.

Now the Israelis are gone after 22 years

of occupation. When EXECUTIVE went to

print, there was a sense of victory across the

country. But despite the celebrations, there

remains uncertainty about what will happen

in the weeks and months to come.

Business does not lend itself to an atmosphere

of uncertainty, whether one is a

banana seller, bank manager, importer, or

stockbroker. The withdrawal has perhaps

brought a feeling of greater uneasiness

than during the occupation, which the

Lebanese had grown accustomed to.

“People feel that a scenario will soon be

played out,” says El-Hajj. “What kind of

scenario, they don’t know.”

There are worries that border conflicts

could escalate into far more punishing air

strikes than what has been seen in recent

times. “Nobody is doing anything, just

waiting to see what will happen,” says

Mohammad Hamzeh, label manager of

Warner Music. “Nobody is making any

investments, nobody is planning any

events.”

At the Riviera Hotel, 20% of this

summer’s bookings are tentative compared

to last year’s near-zero rate. “They don’t

want to commit themselves,” says Nizar

Alouf, managing partner of the hotel.

The uneasiness of the region is affecting

international business circles. “There’s a lot

of indecisiveness from the Americans at this

point, and when you hear the word

Americans, that is business,” says Michael

Dunn, partner at Healey & Baker, a real

estate consultancy firm that helps local — but

primarily foreign — firms with their real estate

needs.

Even prior to Israel’s promises

of withdrawal, the political environment in

Lebanon had impacted its standing in the

investment community. Standard & Poor’s

sovereign rating for the country is BB with

a negative outlook, which is a speculative

grade allowing for political uncertainties.

“The probability of conflict after the

withdrawal is becoming higher,” says Elie

Yachoui, an economist, noting the Shebaa

Farms dispute and other issues. “For the

economy, that means a bad outlook for

investors and more recession.”

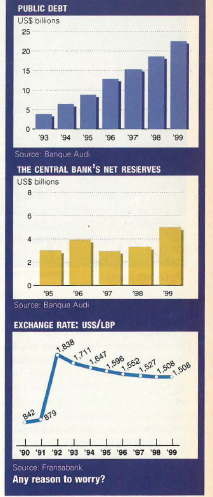

Probably the most disturbing murmurs

prior to the withdrawal emanated from

financial circles. In April, for the first time

in almost a year, the central bank was

forced to intervene in order to prop up the

pound. While figures were not disclosed,

analysts estimate that the bank spent

between $400 million and $450 million

over several weeks.

The pressure on the

pound had calmed down by the time of the

withdrawal, but the Lebanese currency’s

vulnerability is a cause for worry.

“If the withdrawal of Israeli troops in

South Lebanon leads to a deterioration of

stability, we will see a flight to foreign currencies,”

warns Navaid Farooq, Standard &

Poor’s sovereign analyst for the Middle

East and North Africa.

Even if the central

bank, in a bid to prevent the currency’s

collapse, hiked interest rates and started

spending its reserves, there could be panic.

“If depositors decide, in a mass hurry, to

switch from Lebanese pounds to US dollars,

then nothing that any commercial or central

bank can do could hold them,” says one

analyst. In the words of economist Marwan

Iskander: “The banking system could be

shaken to its roots.”

Depositors could rush the banks, changing

their pound-based accounts — 61% at the

beginning of 2000 — into dollars. And if that

happens, it could result in calamity.

People’s purchasing power and standard

of living could be reduced overnight. In a

country so dependent on imports, this

would be devastating. “If the pound were to

devalue by 20% or more, the circumstances

would become all that much harder.

Today, we have a difficult situation, and

if compounded further, it could become

explosive,” warns Iskander.

This would

spur high inflation. Many businesses and

individuals would not be able to repay

loans, and the value of Lebanese T-bills,

which represent a substantial portion of

most Lebanese bank assets, would tumble.

The worry isn’t only with local depositors

switching to hard currencies. Capital outflow

is another concern. “If we have confrontation

with Israel, it would be extremely difficult

for Lebanon to maintain the deposits of the

non-Lebanese, which constitute 30% of

total deposits,” says Iskander.

Couple that scenario with the already bad

economy and possibly hundreds of millions

of dollars in infrastructure damage

caused by Israeli air strikes, and it could

cripple the economy. For the cash-strapped

government, already drowning in nearly

$23 billion of debt, devaluation would create

further troubles.

While a weaker pound

would help relieve the domestic debt,

meeting overall debt payments would

become more cumbersome if Lebanon is

destabilized. “In the worst-case scenario,

there would be increased difficulties in collecting

revenues,” says Farooq.

But prophesying the worst might not be

well founded. The last ten years have witnessed

a spate of crises, from large-scale

Israeli bombardments of Lebanon’s infrastructure,

renegade militants in the North, to

a major turn of government. Through it all,

the sky never caved in, the pound remained stable, people

went to work, the kaaki

sellers continued to sell their kaak, and life went on pretty

much as normal.

Whether it is

coming or not now that the

Israelis have gone, conflict

is certainly nothing unusual to

the Lebanese; they have

lived with it through most of

the last three decades.

“We have gone through

other periods of uncertainty

over the last few years, and the central bank has been a master

at the game. They know

very well how to contain the pressure,”

says Nabil Chaya, head of the treasury at

Banque Audi’s capital markets

division.

Analysts point to

several key firewalls for the

bank. Foreign investors, who

own less than 10% of

Lebanese T-bills, cannot

directly speculate on the

pound, as they did in Southeast Asian countries during

the economic meltdown in

that region. This will help prevent

a “hot money” problem —

a sudden and massive sell-off

at the first signs of instability.

At the same time, the central

bank’s reserves were about $5

billion at the end of 1999 —

higher than ever since the end

of the civil war. If the bank

needed to step in again to

support the currency, it

should have enough reserves

to last for the short to medium

term.

Although it would

choke investment and slow down

the economy further,

interest rates could be hiked to

defend the pound, as they

were during times of uncertainty

in 1992, 1995, and

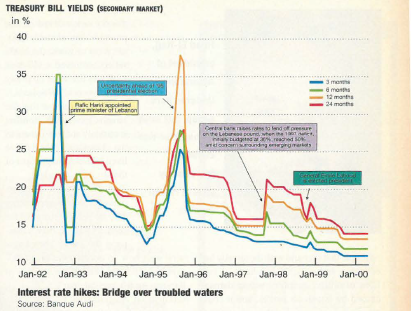

1997 (see graph).

As a last

line of defense, the bank has

gold reserves estimated to be

worth between $2 billion and

$3 billion.

“Even if things go very badly,

no catastrophe is expected for

the simple reason that even with continuing

pressure, the central bank has huge

reserves,” says Mohieddine Kronfol,

financial analyst in the capital markets

division of Middle East Capital Group.

But even if there is no conflict in the

wake of the Israeli withdrawal, Lebanon has

plenty of problems to lose sleep over. “My

biggest concern,” says Kronfol, “is

Lebanon getting its house in order.”

The

government is stuck with a budget deficit

that reached 51.8% at the end of the first

quarter of 2000. That’s up from 42.4% at the

end of 1999 and a far cry larger than the

37.3% that was targeted for the end of this

year — anxiety.

The economy regressed by between –1%

and –1.5% last year, according to the Economist

Intelligence Unit and HSBC.

Official GDP growth estimates for this

year are at 1.5% to 2%. But a recent report

by the Bank of Beirut & the Arab

Countries states: “This year looks harder

than last, given the prudence and the wait-and-see

attitude of economic agents.”

According to a study done by the General

Labor Confederation and the International

Labor Organization, an estimated 48% of

the Lebanese population is on the verge of

poverty and 68% live below the middle

class line — anxiety.

Serious administrative reform has yet to

get underway, the government is locked in

disputes with a number of foreign companies,

and there are serious doubts that this government’s

privatization plans will go

through — anxiety.

At the same time, parliamentary

elections are coming up this

summer, and many are forecasting a change

of government — more uncertainty.

“These are the issues that weigh heavily

on Lebanon,” says Kronfol. “If the issues

are not addressed, the government will find

itself, against its current intentions, having

to raise interest rates to keep the depositors

from converting and keep banks participating

in T-bill auctions. This

would exacerbate Lebanon’s

current economic problems.”

Without solutions, the economy

will continue to deteriorate,

which itself could put pressure

on the pound.

What’s more, opinions are

divided about what may come

now that the era of occupation

has ended. The pullout could

usher in an era of stability.

“The problems with the economy

are obvious,” says Paul

Salem, development analyst.

“The only thing that can get us

out is peace and investment.”

And many people feel that the

withdrawal could be the first step towards

a comprehensive peace settlement.

“This

will turn a new page,” says Georges

Ghorayeb, general manager of the tile

manufacturer Lecico. “We don’t know

what’s coming, but I think it’s a step

towards a solution. We’re optimistic. We

still believe that the past of Lebanon was

much more dangerous than the future.”

The advantages of a peace settlement are

obvious: millions of dollars in foreign

investment and foreign aid, a flood of

tourists, possible trade liberalization.

“Lebanon could count on a rejuvenation of

economic conditions and could hope to

grow at 5% to 6% [per year],” says

Iskander.

He adds that the country may see

as much as $2 billion in compensation for

damages sustained during the Israeli occupation,

from the European Union, Japan, and

especially the oil-rich Arab countries.

“As

well, the privatization process would result

in greater receipts due to increased investor

confidence, which would lead to a larger

reduction in the debt stock, and we would

see increased tax revenues,” says Farooq.

Without a settlement, the benefits are

less obvious. Many political problems, such as

the Palestinian issue, would

continue to fester.

But if

the situation remains

calm, there would likely

be a certain increase in tourism revenue, and it

might prompt some

investment, especially in

the South.

This, according

to Iskander, would mostly

come from the Shiite community

that made money in

Africa, estimated to have

about $5 billion in wealth.

He estimates that as much as $500 million could flow into the South.

“That kind of investment in an economy as

small as Lebanon’s would make a significant

change,” he says.

While the economic choke on Lebanon

may be loosened, the country won’t

breathe easily. “If someone is sick and has

a siesta, how will he wake up?” asks

Yachoui. “Lebanon will probably feel better

after the withdrawal of Israeli troops, but

it does not mean that the country will

recover its full economic health.”

One thing is certain — Lebanon’s problems

did not go away with the Israelis.