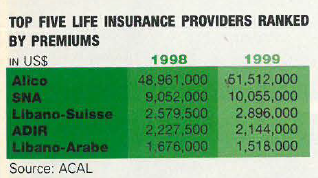

Sales of life premiums grew by just 6%

last year, from $74,778,669 to

$79,272,469, according to the Lebanese

Insurance Companies Association (ACAL).

“The slowdown in growth is more related to

life insurance policies sold as guarantees

for bank loans rather than those sold for

future security,” says Joseph Mrad, a manager

at ADIR, an insurance company catering

mostly to the insurance needs of Byblos

Bank. Over 50% of ADIR’s portfolio is

composed of life insurance policies. The

value of life premiums has dropped from

$2.227 million in 1998 to $2.144 in 1999, a

3.7% decrease. Libano Arabe, which caters

to Banque Audi, is in the same boat. Its life

portfolio has decreased by nearly 10%.

“Banks are being more careful in issuing

loans and consequently the amount of life

premiums collected by the concerned insurance

companies is affected,” says Mrad. In

contrast, firms like Alico, SNA, and

Libano-Suisse, which sell private life insurance

policies not tied to bank loans, have

each seen an increase in business.

NO-LOSE SITUATION

Banque Audi, one of Lebanon’s top

five banks, is offering customers the

opportunity to invest in international equities.

In mid-May, Audi launched “Harvest

Guaranteed” products. Returns are tied to the

performance of the three best-known international

indices: Dow Jones Euro Stoxx 50

(40%), S&P 500 (35%) and Nikkei 225

(25%). Harvest Guaranteed offers three

products. One investment guarantees

returns of 15%, with a maximum return of

between 65% and 70%. A second guarantees

a return of 9%, with a maximum return of

between 82% and 87%; and a third investment

guarantees a return on the capital

invested, with a maximum return of

between 100% and 105%.

“One of the reasons we launched Harvest

was the demand of our clients,” says Nabil

Chaya, head of treasury at Audi’s capital

market division. “It’s also to help investors

think of long-term investing, focusing on

consistent growth, instead of being speculative

and trying to make a quick buck.”

Until now, Audi has offered clients the

chance to trade only on the local market. But

in the last two years, trading volume on the

Beirut Stock Exchange and on Lebanese

GDRs has been in decline, which has been

harmful to the bank’s capital markets division.

Many investment firms, such as

Financial Funds Advisors and Fidus, as

well as the capital markets departments of a

number of banks, including Byblos Bank

and Banque du Liban et d’Outre-Mer, have

been focusing on international markets.

CASINO: EVERYONE

GETS FLUSHED?

The ongoing conflict between the 11

board members of the Compagnie du

Casino du Liban (CCL) and Elie Ghorayeb,

its chairman, continues. The two sides are in

disagreement over how to handle a government

demand that the casino pay back taxes

on slot machine revenues, from which nearly

40% of the $87 million earned from gaming

is generated. “Deloitte & Touche, the

casino’s auditors, estimates that the claim

can vary between $33 million and $100 million,”

says one board member. Intra

Investment Company, the state-controlled

firm that owns 51% of CCL, is expected to

take action when it elects a new president

soon. Three scenarios are possible: remove

Ghorayeb and elect a new chairman, dismiss

the entire board or a combination of both.

“Those scenarios represent a last-ditch effort

to get Ghorayeb removed and solve our

problems with the Ministry of Finance,” says

the board member. He adds that Ghorayeb has

succeeded in alienating the members, the

employees’ syndicate and the minister.

IN NEED

OF A STIMULANT

The Beirut Stock Exchange (BSE) suffered

operational losses of $70,315 in 1999

due to a slowdown in trading. A decrease in

earnings from commissions, coupled with a

failure on the part of some member companies

to pay their dues, was the root of the problem,

according to Fadi Khalaf, the market’s chairman.

Sales of BSE stocks have cratered since

1997, from $639 million to $331 million in

1998, falling to just $90 million in 1999. The

market did not start off well this year either,

with trading volume amounting to

$28 million in the first four months, in

contrast to $40 million for the same

period in 1999. There have been

reports that the BSE is trying to

encourage television stations to go

public. But there are obstacles: To list

shares, television stations have to get

the approval of the Council of Ministers.

There have also been reports that the

BSE was trying to encourage the two

mobile phone operators, LibanCell

and Cellis, to list shares. “Listing big

names such as LibanCell and Cellis could be a stimulant

to the nearly nonexistent trading activity

on the BSE,” says one analyst. That idea

may have to wait until the operators resolve

their differences with the government.

STAYING

IMAGINATIVE

Lebanese tile maker Uniceramic is celebrating

its 25th anniversary this year by

launching a new line of products. The company

was busy showing off its new

30x60cm, 30x45cm and 10x10cm tiles,

as well as a new imported brand called “Lifetile,”

during the Project Lebanon exhibition at the

Beirut Forum. The company has been trying

to compensate for what has so far been a

20% drop in local sales this year. The company

has also been looking abroad for markets.

“With the drop in construction, our capacity

has been reduced to two days per week, and

now our focus is to increase exports,” says

Nabil Ghorra, assistant general manager.

Exports have increased by 142% in the first

four months of 2000. Uniceramic expects to

acquire ISO 9000 certification some time

this year and has a goal of increasing exports to

20–25% of all sales by the end of 2000. “The good

part is that we have hit the US and Canadian

markets where they have a quality requirement

and we don’t have to compete against cheap

products,” says Ghorra.

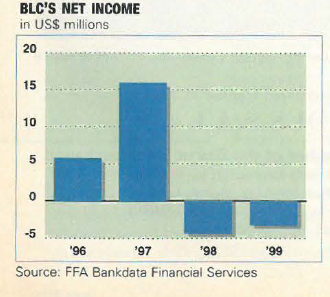

MORE WORRIES

Banque Libanaise pour le Commerce

(BLC), a listed bank with shares traded on the

Beirut Stock Exchange (BSE) and the GDR

market, finally released its 1998 and 1999

results. After impressive earnings of $15.9

million in 1997, BLC showed losses of $4.3

million in 1998 and $3.2 million last year. But

these are the least of the bank’s worries.

BLC is currently recovering from a messy

merger with United Bank of Lebanon. Two

months ago, Safi Harb, the architect of the

deal, was forced to step down as chairman of

the financial institution after being accused of

mismanaging bank funds. Last month,

UBL-BLC filed a $14 million lawsuit

against Harb. But the bank’s board of directors

is reportedly divided over whether to continue

legal action against their old chairman

or settle out of court. “To be honest with you,

I don’t know where this bank is heading,”

says one analyst. Investors feel the

same. BLC’s shares on the BSE have fallen

over 27% this year, while its GDRs have

plummeted nearly 36%.

DIFFERENT

STRATEGIES,

DIFFERENT RESULTS

Byblos Bank, one of Lebanon’s top five

banks, declared unaudited net income of

$13.4 million in the first quarter this year, a

0.24% decline from the same period last

year. Total assets, on the other hand, went up

7.35% to $3.75 billion, and there was an

11.9% rise in customer deposits, which

reached $2.87 billion. Byblos’ stocks on the

BSE have fallen 20% so far this year. Banque

Européenne pour le Moyen Orient SAL

(BEMO) posted net profits of $866,546 for the

first quarter, an increase of 2.94% compared

to the same period last year. The bank’s total

assets went up 26.8% to $395.3 million and

customer deposits totaled $319.88 million, a

35.4% rise. “BEMO is a recession-proof

bank, having most of its liquidity in US dollars

and 95% of its loans also in dollars,”

says a local analyst. BEMO doesn’t rely as

much on T-bills and tries to forego high

yields for less risky investments.

Banque Libano-Francaise (BLF), on

the other hand, saw its net income fall 23%,

to $36.4 million in 1999. Assets rose 6.7%,

to $3 billion, and customer deposits went up

8.3%, to $2.54 billion. “BLF has a high

exposure to the Lebanese pound and has

extended its loans to the government,

increasing exposure and risk, while receiving

slow-moving returns,” says one analyst.

IMPLEMENTING

PRIVATIZATION:

MISSION IMPOSSIBLE?

Alas, the government has finally passed

the much anticipated draft bill for the

privatization of state-owned enterprises.

Reports from the Ministry of Finance suggest

that the telecommunication sector and

Middle East Airlines are the first candidates

for privatization. Along with the sale of

Électricité du Liban (EDL), Télé Liban and

the casino, the government could net some $5

billion in revenues, helping to reduce the government’s

ballooning debt. “I expect delays

in implementation as the bill had no clear

plan of execution and it faces serious political

opposition,” says one local analyst.

PLASTIC FOR BRAINS

Your credit cards are about to become

a whole lot smarter. Lebanon will

soon become one of the first countries in the

world to adopt Smart Card technology.

Credit Libanais and Visa International, in

cooperation with a number of local banks,

are responsible for bringing the new technology

to Lebanon.

The card contains electronic chips that are

able to store and process large amounts of

information and provide a higher level of

safety and security. “It is the beginning of

the future,” says Antoine Raad, deputy

general manager of Credit Libanais and

coordinator for the seven banks involved in

the project. “It opens the way to multi-applications

which will be possible with the

new technology.” The Smart Card is

expected to replace the magnetic-stripe

card within the next five years.