• Some signs of moderation are evident in recent economic data, and

inflation remains virtually absent. That’s unlikely to stay the Federal

Reserve’s hand, however. Policymakers are concerned about the

underlying strength of the economy and the tightness of the labor market.

Those worries are likely to prompt a 25-basis-point tightening at

the June 27–28 FOMC meeting, in our judgment.

• Sharp declines in energy prices pushed the April producer price

index down by 0.3%. The core PPI edged up by 0.1% and was only

1.3% above its year-earlier level; excluding the recent pop in

tobacco prices, the year-to-year PPI was unchanged. In other words,

the report showed no inflationary pressures.

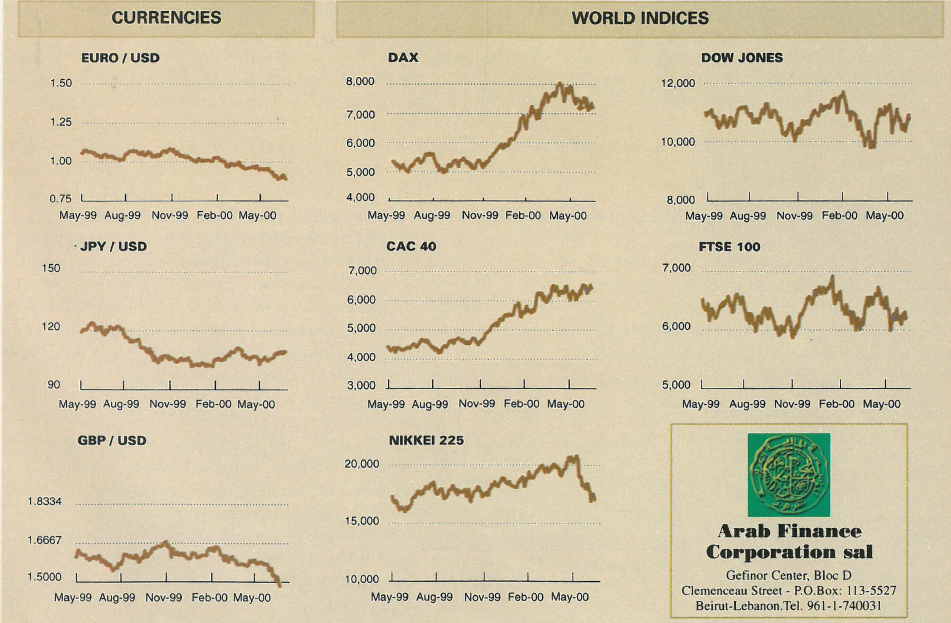

EURO

• The euro recently declined to a record low of about 89¢ against the

dollar. We continue to think that the euro will eventually strengthen,

but we have lowered our target. Without a recession in the US or a

burst of public sector reform initiatives in Europe — both of which are

unlikely to occur, in our view — the dollar will probably stay at higher

levels versus the euro than we had been expecting.

• We now think that the euro will remain below parity for much of

2000. Next year, when US and European economic growth rates are

likely to converge, the euro ought to be able to move above parity.

Our new forecast: we think that the $/euro rate will be 0.95 in three

months, 0.99 in six months, and 1.06 in 12 months; our previous forecasts

were 0.99, 1.06, and 1.10, respectively.

• In our view, two major problems plague the euro. First, the US economy

has been growing faster than the Eurozone economy by a wide margin.

Second, structural reforms in the Eurozone have not gone far enough

in the crucial areas of labor policy, regulatory policy, and pensions.

Investors’ concerns about both issues have helped to channel the flow

STRATEGY FOCUS

GLOBAL VIEW

• We have reduced our overweight of Japan in favor of Eurozone equities.

We still like Japan, but the pace of restructuring in that country

in relation to that of the Eurozone does not justify a more aggressive

stance, in our view. It’s particularly true at a time when money

growth is slowing in Japan and the Bank of Japan has let speculation

flourish about possible rate hikes later in the year. The Eurozone has

the added advantage of having a much more competitive currency than

Japan and, consequently, better growth prospects, in our view.

• Consumer spending moderation in April as overall retail sales

declined by 0.2%; excluding automobiles, retail sales were unchanged.

That was a much weaker showing than most market participants

expected. In addition, it appears that concerns about stock market

volatility and higher interest rates have started to show up in consumers’

spending patterns. We expect real consumer spending to increase at a

rate of 4.5% for the second quarter; that’s a healthy pace, but far below

the torrid first-quarter pace of 8.3%.

• Meanwhile, import prices for April declined by 1.6%, led by a drop

of 12.7% in petroleum prices; excluding that sector, import prices

edged by 0.1%. Export prices slipped by 0.1%.

Bruce Steinberg, chief economist

of capital out of Europe and into the US, to the benefit of the dollar.

• Europe’s economic growth is currently the best it has been in a

decade, with Eurozone GDP set to rise by about 3.5% in 2000. Even

so, growth this year will probably be 5.0%. That means that the

growth differential will remain very large for the time being. Next

year, however, we expect Eurozone GDP to increase by 3.2% and

US GDP to rise by 3.6%, the smallest gap in more than a decade.

• Additional pluses for the euro include the development of the

region’s capital markets, which are beginning to resemble those in the

US, and the massive corporate restructuring efforts that are under way

in Europe. Nonetheless, Europe lags the US on a number of economic

fronts. In particular, the political will to implement labor market reforms

appears to be lacking. Without more flexibility in the labor market,

trends in European productivity and economic growth will almost certainly

continue to lag those in America. That, in turn, will tend to limit

the euro’s long-term upside potential.

MICHAEL HARTNETT, SENIOR INTERNATIONAL ECONOMIST

GLOBAL ECONOMICS TEAM

• With liquidity conditions deteriorating, risk aversion rising, and a possible

slowdown in global growth prospects looming, we have moved

the emerging markets down from a small overweight to an underweight,

in our global portfolio. However, those markets appear to be better situated

to withstand a slowdown than they were the last time around.

• The recent weakness in global bond markets suggests that investors

are not convinced that monetary policy has been tightened sufficiently

to ensure price stability. We expect short-term interest rates to rise further

during the next three months. For that reason, our regional

asset allocation guidelines suggest that investors adopt above-average

cash levels.

• GDP growth expectations are still rising and inflation expectations

are under some upward pressure from cyclical forces. As a result, it

is no surprise that European central banks and the US Federal

Reserve have been tightening. The tightening, together with the

effects of higher energy costs, could begin to influence economic

growth prospects as fall approaches. The OECD leading indicator for

the G7 nations has topped out, and liquidity conditions particularly

in the US have begun to deteriorate. Moreover, the Japanese inventory-shipment

ratio, a key cyclical indicator, turned down in March.

Those developments are consistent with a peak in global industrial production

growth this summer. That, in turn, would argue for a shift

toward a more defensive portfolio. Interestingly, turning points in the

growth rate of the OECD leading indicator have tended to coincide

with major changes in sector leadership. Traditionally, when the

growth rate is declining, pharmaceutical and insurance issues have

done relatively well.

• The influence of tighter monetary policy has already manifested itself

in the form of increased risk aversion across a number of asset classes.

We expect that trend to continue as central banks tighten further. Signs

of risk aversion include the major deterioration in equity market

breadth, particularly in the NASDAQ; much wider spreads in the corporate

bond market; the underperformance of many emerging markets;

and the weakness of the Australian dollar (the currency of a country

with a large current-account deficit) against the yen (the currency

counterpart of a country with a large current-account surplus).

• One surprise, in our view, is how well the dollar has held up in the face

of the NASDAQ market’s sharp setback. The dollar’s strength indicates

that global investors are still prepared to fund the US private sector’s

financial deficit and that they still think that returns on US assets will

be better than those on European and Japanese assets. However, we

believe that the current divergence between the performance of the

NASDAQ and the dollar is unsustainable.

• If risk aversion declines and the dollar continues to strengthen, economically

sensitive stock market sectors particularly the technology

sector could start to outperform again. On the other hand, if recent

inflation concerns in the US lead to a Fed-induced period of below-trend

economic growth, our strategy would probably need to become

much more defensive.

• The global context raises two crucial questions in that regard. First,

to what extent have America’s remarkable good inflation trends been

helped, until recently, by below-trend growth in the rest of the world?

Second, what are the implications of the funding of the US private sector’s

financial deficit if investment activity starts to increase faster than

savings in Japan and Europe? The more prospective returns in Europe

and Japan improve, the more the US may struggle to fund its expansion

just when domestic capacity is significantly increased. Against

that backdrop, we continue to prefer non-US markets.