SOLIDERE

Solidere’s GDR found itself the beneficiary of positive investor expectations upon news of the planned resumption of peace talks between the Syrians and the Israelis. Even though the real estate giant faced some unnecessary bureaucratic knots, which resulted in delays on its projects, the GDR was buoyed by prospects of peace talks that might generate capital inflows into the real estate sector. The GDR reinforced vital signs of revival as it inched up steadily from December 15’s close of $6.950 to close on January 12 at $8.475, a 21.90% increase in a one-month period.

BLC

On December 23, Banque Libanaise pour le Commerce held a General Assembly to discuss the merger with the United Bank of Lebanon (UBL).

The Assembly revealed a net loss of $4.3m in 1998, well below the $11.7m profit announced earlier and the $15.9m profit in 1997. The discrepancy between the two was the result of a sharp increase of $16.5m in the provisions for doubtful loans to $24.1m. BLC’s GDR had a very volatile month, falling to $13.25, only to rise back again to $13.35 after the turn of the millennium. On January 6, the GDR hit a low of $12.83.

BLOM

In mid-December, Banque du Liban et d’Outre-Mer SAL announced the launch of a new interactive banking voice response system called ALLOBLOM, a 24-hour-a-day service that facilitates banking transactions and information inquiries. BLOM’s GDR was the main highlight of the month: it soared to $28.5 on the back of strong demand supported by sound fundamentals and good value, with a P/E ratio on expected 1999 earnings of 7.33. With the publishing of its full-year 1999 figures, BLOM is expected to further consolidate its position as Lebanon’s most profitable bank.

AUDI

Bank Audi’s announcement that it was to buy back two-thirds of its outstanding GDRs at $20.75 and the Central Bank’s authorization of this plan were two events, the very first of their kind in Lebanon, to promote a certain degree of liquidity and confidence. Audi’s GDR was subject to an initial rise directly after the bank’s announcement. However, soon afterwards, the GDR retreated back to its static price of $20.3 and then managed to inch up just a little to close finally on January 12 at $20.6.

MOROCCO

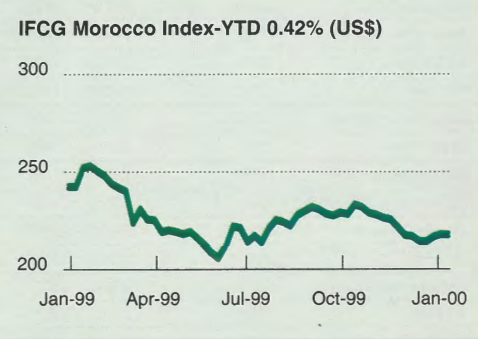

Moroccan equities started the new year on a hesitant note, with institutional investors remaining largely on the sidelines. However, investors are looking ahead into the year, when GDP is expected to pick up to around 6% from almost zero growth for 1999. The new five-year plan, recently released by the government**,** is likely to promote more economic diversification, reduce the country’s dependence on the agriculture sector, and tackle the high unemployment level. Achieving higher economic growth will spur more activity on the equity market, while the next phase of the state privatization agenda is likely to boost liquidity levels.

EGYPT

The Egyptian market continued its bull run into the second week of the year, registering further gains on the back of healthy earnings results in the telecom sector and consolidation news in the cement sector. Market leader MobiNil announced that its 1999 fourth quarter (Q4) net profit rose 45% to EGP90.4 million ($26.3 million) from EGP62.5 million in Q3, with full-year results amounting to EGP140.8 million on EGP1.5 billion in revenues. Sentiment on the bourse was also boosted by Suez Cement’s bid to buy a 65% stake in Tora Portland Cement for an amount of EGP1.4 billion, or EGP80 per share. The banking sector was also buoyant, boosted by news that a new law on mortgages was being drafted.

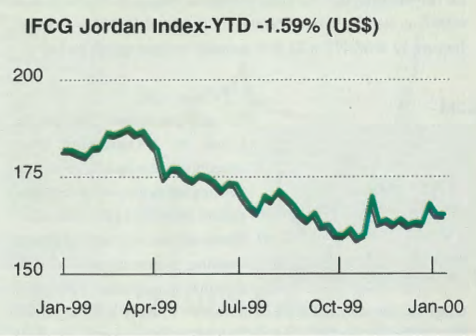

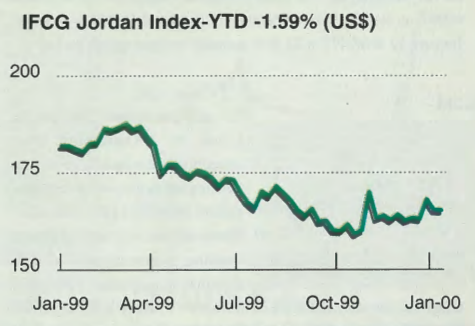

JORDAN

Despite easing monetary policy and lower interest rates on JD deposits, the Amman Stock Exchange continued to suffer from thin liquidity, with prices losing ground in the first two weeks of the year. Equity prices have barely moved since last November, when the market witnessed an extraordinary rise. However, the market is expected to witness an increase in fund flows as valuations reach attractive levels and new privatization deals come to the market. This is expected to be supported by growth in the construction and tourism sectors and new automated trading at the ASE from the second quarter of 2000.

Interest rate differentials between Arab currencies and the dollar on the decline

Historically, there has been a certain spread between domestic and dollar interest rates in Arab countries whose currencies are pegged to the dollar. The spreads fluctuated over time and varied from one country to another depending on economic fundamentals, size of foreign reserves, inflation differential with the US, and markets’ assessment of the risk of devaluation. The availability of such spreads helped preserve the attractiveness of local currencies and provided support to their fixed dollar pegs. Improvement in a country’s economic fundamentals invariably made it possible for the monetary authorities to steer domestic interest rates lower, closer to those on the dollar. However, there is a limit to how much interest rate differentials can be reduced without threatening the fixed dollar peg. A spread is needed to compensate holders of local currency for the higher risk incurred, both actual and perceived, when holding that currency.

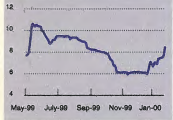

Interest rates on the Jordanian dinar (JD) have been maintained at relatively high levels since 1996 to help bolster monetary stability and support the peg to the US dollar that was officially introduced in October 1995 at $1.41 to the JD. However, the slowdown of economic activity in the country, coupled with a strong build-up in foreign reserves, allowed the central bank to shift to an expansionary monetary policy. Rates on three-month certificates of deposit (CDs) assumed a declining trend in 1999, dropping to an average of 6.025% in November, from 9.45% in January. As a result, the differential between three-month Jordanian CDs and three-month US T-bills narrowed from 5.89% in October 1998 to 0.73% in December this year (chart 1). It has become evident now that there is no room left for interest rates on JD deposits to drop further as the spread on US treasuries is now way below the historic 3% level. On the contrary, if, as expected, dollar rates continue to rise, the corresponding JD rates are likely to follow suit.

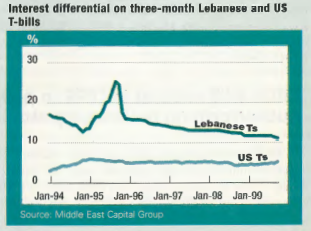

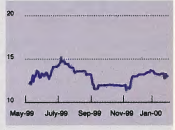

Interest rates have also been trending lower in Lebanon amidst regained confidence in the Lebanese pound and a noticeable slowdown in economic activity. Rates on three-month Lebanese T-bills declined to 11% by the first week of December last year from an average of 12.7% in 1998, 13.4% in 1997, and 15.2% in 1996. The spread between Lebanese three-month bills and their US counterparts now stands at 5.89%, compared to 7.3% in January 1999 and a high of 20% in September 1995 (chart 2). Not much room is left for short-term interest rates on the Lebanese pound to drop as the spread with corresponding dollar rates is approaching the critical 5% level deemed necessary by market participants to compensate investors for the risk they incur in holding the local currency, given the surging indebtedness of the Lebanese economy.

In Egypt, rates have also followed a downward track over the past few years, albeit at a slower pace than in Lebanon and Jordan. The three-month T-bill rate was lowered from 10.2% in 1996 to 9.8% in 1997, 9.4% in 1998, and 9.1% in June this year. The pressure on the Egyptian pound in the foreign exchange market, particularly in light of the widening external imbalance, saw domestic interest rates edging slightly higher in the past few months. The country’s foreign reserves dropped to $17.5 billion from more than $20 billion at the beginning of the year. If the new government regains credibility in the foreign exchange market and the privatization process picks up momentum, leading to higher levels of foreign direct and portfolio investments, then the spread between Egyptian pound and dollar interest rates has room to tighten further.

Other countries in the region have also witnessed a decline in interest rates. In Morocco, deposit rates dropped from 12.3% in 1994 to 7% by the first week of December 1999. Tunisian rates were down from 8.8% to 5.9% during the same period.

In Gulf countries, domestic interest rates rose in the first quarter of 1999, even though dollar rates were stable. Interest rate differentials between Saudi riyal and dollar deposits rose from a low of 0.35% in January 1998 to a high of 1.95% in March 1999. The widening spreads were a reflection of heightened speculative pressure against the riyal at a time when oil prices were on the decline. With the rise in oil prices later in the year, speculative pressure on the Saudi riyal subsided and by December 1999, Saudi riyal-dollar interest rate differentials shrank to 0.3%. During periods where there is little or no speculation against the Gulf currencies, interest rates on local currency deposits tend to move in tandem with corresponding dollar rates.