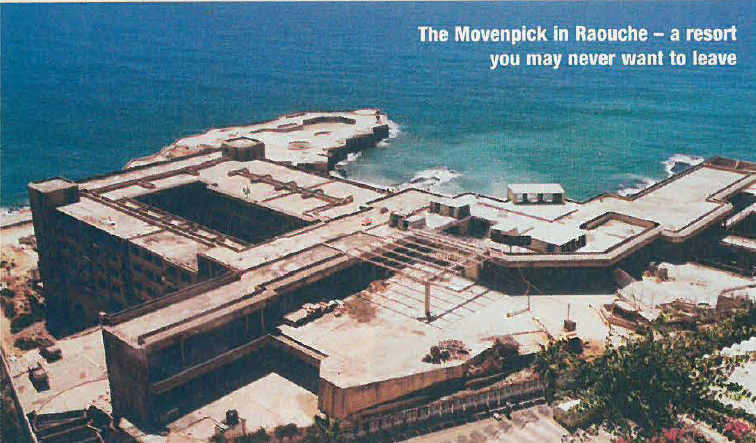

Construction at the $100 million

Movenpick resort in Raouche steams

ahead. The 72 chalets and 1,000 cabins

have already gone up 7% in price since hitting

the market on August 1, and while

Kingdom Holding won’t reveal the figures,

the diagrams in the on-site sales

office suggest sales are going well.

Sales manager Samer Abu Ayash admits

that the project has faced a credibility gap.

“Everyone knows the checkered past under

the old owners,” he says. “This makes it

more important that we get things right and

on time.” Movenpick has similar resorts at

the Dead Sea and Sharm el-Sheikh.

Branding is important. Alwaleed Bin Talal

is himself a brand name. “When he says the

project will be finished in summer 2002,” says

Abu Ayash, “people believe him.”

The project has a 4,000m2 health club, a

30,000m2 hotel, a l ,500m2 shopping mall,

swimming pools, restaurants, chalets, cabins,

a marina and 700 parking spaces. The

shops, says Abu Ayash, will attract local

residents as well as those using the resort.

The biggest unit until now is 80m’,

although the design allows up to 200m2

“Visitors to the hotel will be able to do

everything within the resort,” says Abu

Ayash. “This is unique in Lebanon. They

can rent a boat, put the kids in their own

pool, have a mud bath and go to a restaurant.

Some people who go to Sharm el-Sheikh

never leave the resort for two weeks.”

The main interest in chalets has come, says

Abu Ayash, from Lebanese expatriates,

while interest in cabins stems mainly from

Beirutis. The largest chalet, around 208m’, is

close to $ l million (with prices between

$4,250 and $5,250 perm’) and the 6m2 cabins

are $25,000 to $30,000. Not cheap. But

there is no rival project on the horizon.

Score one for SMGH

The Saudi-run Societe Mediterraneenne

des Grands Hotels (SMGH) has finally

received permission to demolish the old

Hilton, amalgamate the plot with an adjacent

one and keep a built-up area (BUA) of over

31,000m’ on the combined site. That clears

the way for a new 20-storey Hilton.

The company bought Mi net el Hosn plot

111 – complete with the 27,000m’ ruined

hotel – in 1980. When the Solidere master

plan came into effect, the appraised value

of the site was around $ 11 million, but the

owners decided to keep it rather than take

Solidere shares. SMGH then paid $4 million

for the adjacent plot with 4,300m’ of

BUA. Under current regulations, new

build on I LI would have been restricted to

around 10,000m’, but the council of ministers

has granted an exception and

allowed the combined site to retain the

existing BUA of 31,300m2

It adds up to a shrewd move by the owners.

If they had bought at current Solidere

prices, they would have paid around $31 million

for both plots. Construction will take

around three years. The company is confident

that Lebanon can accommodate more

five-star hotels in addition to the Phoenicia.

Building a

bad reputation

Architect Charles Hadife had a shock in

June when he opened a newspaper

and saw a picture of his home in Beit

Chehab house. “A traditional Lebanese villa

developed by the Hayek Group,” he read. Not

true. Hadifeh did the renovation himself.

The newspaper explained that the Hayek

Group is using the Internet to market themselves

to Lebanese expatriates, offering services

from brokerage to engineering, finance

and legal advice.

Hadife was livid. “I sent someone to

Hayek group asking if I could buy the house

– they said they’d sold it.” EXECUTIVE contacted

the Hayek Group and asked where to

find the house and whether Hayek renovated

it. “I think it’s in Beit Mery or Broummana,”

said the receptionist, “and no, that’s not one

we did.” Strange, then, to choose a house that

has been featured in international architecture

magazines and belongs to one of Lebanon’s

best-known architects.

Southern bargains

The market is even more sluggish in the

South than in Beirut. A 1995, 320m’

duplex with four bedrooms, three bathrooms

and five balconies on the edge ofTyre can be

yours for just $80,000 – and yet it’s been on

the market for several months. The brokers are

Cedarweb (www.cedarweb.com).

Real estate in the south declined with the

Israeli attacks of 1996. The stagnation, says

Tyre developer Ibrahim Mourtada, has been

not so much in prices – which have fallen up

to 20% since 1996 – as in the delay or

amount of a fust payment. Smaller units of

around 120m’ are about $250 per m2, with

new duplexes fetching $320-$350 per m2

This suggests the Cedarweb duplex is a bargain

– provided you have the necessary: It’s

a cash sale with no credit facilities.

EXECUTIVE has teamed up with international real estate consultants Healey & Baker to provide information

about market activity in Beirut and its suburbs. The real estate listings change monthly and

are updated quarterly. The following profiles will be revisited in February.

The BCD residential market is currently skewed by Solidere’s pricing strategy at Saifi,

which is to sell at $1 ,750 per m’ (base) and rent from a base of $85 per m’ – a strategy

followed by the company in order to attract residents downtown when clients are unwilling

to buy at these prices. The rate outside Saifi is around $1,500 perm’ for sale and something

over $100 perm’ for rental. It will be interesting to see how this develops over time,

especially as approximately 65% of BCD is zoned for residential.

After all the delays, and the ups and downs, the market in BCD now seems to be

finding its level. Refurbished offices are fetching between $150 and $175 perm’ in

annual rental, and new build, like the Atrium, is going for up to $250 per m’. Demand

is now focused on new build (especially from international companies), with less for the

renovated buildings.

Solidere’s target price for retail is $5,000 per m’ for sale and $500 per m’ for rental.

The highest price achieved so far for retail downtown appears to be $9,000 per m’

in the Atrium, where proximity to the souks and Banks Street has proved a crucial factor.

The cheapest ground floor retail is available for less than the Solidere target. This

is very much a market that will change quickly, especially when the souks project

comes on stream.

Ever popular for homes, Hamra is a genuine community with local amenities and a

busting, cosmopolitan atmosphere. The cheaper residential is the older buildings,

and there are some bargains here for those seeking character rather than up-to-the

minute luxury. Parking problems, traffic and honking horns will always limit the potential

for growth.

Hamra is mixed as a business area, just as it is in retail. There are no obvious benchmarks

for pricing offices. While there is attraction for some businesses to be in such a busy area,

others – especially international companies – will be deterred by the traffic congestion, the

very low number of up-to-date office blocks and the general lack of purpose-built parking.

I n the best locations, retail prices in Hamra remain high. At the same time, there are a

number of badly designed malls that have fallen into disrepair. The opening of the

Crowne Plaza should give Hamra a big lift, adding to the boost already given by names

like Starbucks, lntimissimi and The Body Shop. Hamra will endure the opening of the

souks downtown if it can continue to offer impulse, easy-access shopping. Don’t

expect large stores in the area.

Mar Elias became a popular retail destination during the war, and subsequently has

suffered because of Verdun’s proximity. The development of retail downtown will

lead to a further deterioration. Housing in Mar Elias – including new build – is of mixed

quality and not helped by the large amount of property let at old rents, which act as a

huge disincentive for owners to carry out repairs, much less improvements. Most rental

is at the medium level.