Abroad overview of the Islamic financial world shows that the phenomenon truly is global. From its humble beginnings in the Middle East of the 1950s, the sector has grown into a $500 billion industry, with $350 billion invested in the region itself. Furthermore, the Islamic finance sector in South Asia has broken the $100 billion mark and the infant Western markets are already worth a combined $30 billion. Around the world, there are over 300 Islamic financial institutions in more than 50 countries.

Industry overview

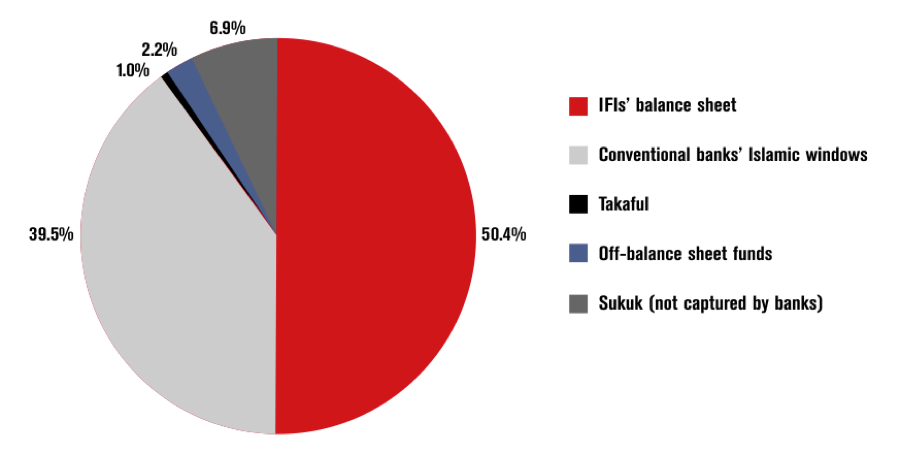

A breakdown of Islamic financial assets at the end of 2006 shows exactly how that capital is distributed. Roughly half of all capital managed under sharia rules resides on the balance sheets of Islamic financial institutions.

The next largest segment, at 40%, is placed at the Islamic windows of conventional banks, like Citi Islamic, HSBC Amanah and others. Sukuk not managed by banks check in at 6.9%, while takaful accounts for just one percent of the total. Although the takaful market is expected to grow, lack of emphasis on long-term planning in the Arab world has largely ham-strung the industry.

On the other hand, the sukuk market has been growing at a phenomenal pace and by 2007, global volumes had reached $97.3 billion, with the majority originating from Malaysia and states in the Persian Gulf. In a recent study, Moody’s noted that overall issuance volume of sukuk increased by 71% to $32.65 billion in 2007 within the Europe, Middle East, Africa (EMEA) region. The largest proportion of sukuk was issued in the financial services sector, accounting for 31% of total volume, followed by real estate with 25% and power and utilities with 12%.

While the sukuk market is growing rapidly, not all is well. Recently a dust-up over sharia compliance had the Islamic finance world’s main regulator, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), claim that 85% of sukuk were un-Islamic. (See the Industry segment for more on this regulatory issue). The incident has prompted sharia scholars and Muslim investors alike to reexamine the basics of Islamic finance.

In this context, it is useful to consider some of the defining features of Islamic finance to better understand the markets. Of course, the most visible feature of Islamic finance is the prohibition on interest.

However, “the Islamic ban on interest does not mean that capital is costless in an Islamic system,” said Ghassan Chammas, an Islamic finance business consultant. “Islam recognizes capital as a factor of production but it does not allow it to make a prior or pre-determined claim… in the form of interest.”

Breakdown of Islamic financial assets at YE2006

Pillars of Islamic finance

Certainly, this prohibition on interest gets the most play in today’s mainstream media, but this is just one of the five distinguishing features of Islamic finance. In order for an investment to be sharia-compliant it should also be multi-purpose and not merely commercial. The idea is to remember that God and society are more important than the bottom line. One can think of it as built-in corporate social responsibility.

Furthermore, financial transactions should involve the sharing of risk. Any deal that is guaranteed to make a profit is unacceptable and falls into the same category as interest. Also, uncertain transactions are not allowed, meaning that goods for sale or the details of a contract must be clearly and completely understood before the transaction takes place.

Finally, sharia-compliant investments must not sponsor haram, un-Islamic, activities. This includes things like the armament industry, pork products, alcohol and the entertainment industry like gambling and nightclubs.

This final prohibition complicates due diligence procedures for Islamic funds, as every element of the fund must be investigated for sharia compliance by a sharia supervisory board.

Despite this inconvenience for funds, and the growing pains in the sukuk market, strong growth for both products is expected to continue for the near future. The sukuk market alone is expected to hit $100 billion by the end of this year.