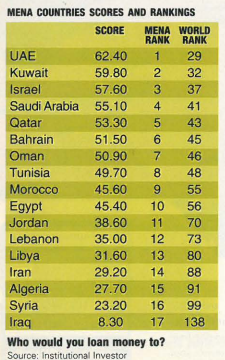

How likely is Lebanon to default on its

loans? More than you might think,

says US magazine Institutional Investor. In

its semi-annual survey of the creditworthiness

of 145 countries, it ranked Lebanon 73rd

worldwide and 12th out of 17 countries in the

Middle East and North Africa. The survey

ranks countries on a scale of zero to 100, with

100 representing the least chance of debt

default. Lebanon scored 35, below the

regional and global averages of 42.64 and

40.9 respectively. Lebanon placed ahead of

regional countries such as Libya, Iran and

Algeria but fell behind Sri Lanka and El

Salvador on a global basis. The highest

ranking in the Middle East and North Africa

went to the UAE with 62.4. “Lebanon has

never defaulted on a loan, even during peak

war times,” says Ziad Maalouf, vice president

of Middle East Capital Group. He adds

that although rating agencies like S&P,

IBCA and Moody’s have not given

Lebanon an investment grade rating, they

also haven’t changed their three-year credit

rating stance of BB-.

Facts

or fiction

about the

Casino?

There have been conflicting

reports in the

media about troubles at the

casino. The board of directors of the Casino du

Liban reportedly asked chairman Elie

Ghorayeb, who was appointed in March

1999, to resign or face being ousted at the

upcoming general assembly. But according to

one board member, the request was not made for

Ghorayeb’s resignation. “If anything it

would have to be a political decision and not

ours,” he says.

Another mid-April report claimed that

Georges Corm, minister of finance, had

demanded $80 million in unpaid taxes and

fines from the casino. It said that the casino

must pay 30% taxes on revenues generated

from slot machines. The article also warned

that, as a result, auditors Deloitte & Touche

expected the casino to record a loss of $4 million

to $5 million in 1999 and that some

$45.2 million were owed in taxes on slot

machines since 1997. Another publication

quoted board members and auditors as saying

that the earlier article was incorrect. What’s the

truth? “The casino and the ministry of

finance have conflicting opinions on slots. The

latter wants to impose a fee similar to other

gaming fees at the casino, rather than the

fixed fee they used to impose,” says a board

member. The casino had announced preliminary

pre-tax profits of $19.5 million in 1999,

a 50% increase over 1998.

Niche player

Al-Mawarid’s strategy of investing in

retail products, IT and human

resources is starting to pay off. The bank’s

profits increased 26.9%, from $878,000 to

$1.1 million (unaudited) last year. Total

assets jumped 31.9% to $266.9 million,

and deposits grew to $213.4 million, a

27% increase.

Its focus on retail banking, the bank

moved aggressively into credit and debit

cards (it just launched MasterCard free of

charge), has created growth in fee-based

income, up 60.5%. Its interest income

increased 30%, while loans grew by

28.5%. “As a medium-sized bank, it is trying

to be a solid niche player,” says

Nicolas Photiades, senior vice president at

Thomson Financial BankWatch. “It is

working to rely more on a recurrent fee-based

income stream as a normal bank

should operate, while the majority of

medium-sized banks depend mostly on T-bills.”

At the end of last year, Thomson

Financial BankWatch gave Al-Mawarid a

B+ for senior debt rating and LC-2 for

short-term local currency debt rating. But

Al-Mawarid still has a major challenge

ahead: By moving into retail banking, it has

to compete with top-tier banks.

The Innovator

Last month Banque Audi again proved to

be the leader in innovation. It offered

$100 million worth of ten-year bonds, the

first company in the Middle East to issue a

note with this length of maturity. It coincides

with the bank’s buyback of $100 million worth of

its notes, which were scheduled to mature

next year. Audi paid slightly above the

market price. Those who held Audi’s paper

were given the chance to reinvest in the new bond before fresh investors came in.

According to Audi, its objective was to

contain its outstanding debt and lengthen the

time required to repay the entire loan.

But one question remains: When will

Audi’s aggressive approach pay off? Last

year its profits dropped 11%. The recurrent

fees and commissions generated from new

products along with the bank’s heavy

expansion will start generating results in

2000, says Fadlo Choueiri, project officer

at Arab Finance Corporation (AFC).

AFC’s recent report ranked Audi’s GDRs

“outperform”, one notch below “buy.” The

finance house predicts earnings to reach

$41 million, up 8%, and it expects its

GDRs to climb from $20.5 to $23.45 by

year-end. ABN AMRO, however, recommends

“hold,” saying the sluggish economy

will limit growth. It expects earnings to

increase 4%. According to AFC, Audi

shares, currently trading on the Beirut

Stock Exchange for $26.5, are overpriced.

The 2000

challenge

There were mixed results for

Lebanon’s banks during the first quarter

of 2000. Banque du Liban et d’ Outre-Mer

(BLOM), the largest by assets and

deposits, is still managing to shrug off

harsh economic conditions. In the first

quarter, its profits climbed 14.5% compared

to the same period last year. Last

year’s profits grew by 19.97%, above the

average of some of the 15 leading banks,

which saw a 3.7% decrease in profits.

Analysts attribute BLOM’s success to conservatism

and cost control. But the bank is

also making a move in retail banking.

According to Samer Azhari, general manager,

the bank’s non-interest income

increased 25% in the first quarter. Arab

Finance Corporation and ABN AMRO

recently gave BLOM’s GDRs a “buy”

ranking. AFC’s target price is $33.20, up

from the current trading price of $24.75,

while ABN AMRO calculates the target

price at $30. “We continue to favor BLOM as a speculative play for the short term,”

says Ghassan Medawar, financial analyst

for Middle East and North Africa at ABN

AMRO.

On the other hand, Bank of Beirut’s

(BoB) first quarter profits fell 15.8%. This

follows a 27% surge in profits for 1999.

According to BoB, the slump came partially

from non-recurrent expenditures, amortization

and goodwill related to its merger

with Transorient Bank last year, plus the

recent tax hike. It claims that without those

factors, its profits would have increased 6%.

Ciments Blancs in

the red … again

Ciments Blancs, reeling from the slump

in the construction sector, registered

losses of some $564,000 last year, down further

from $372,000 in 1998. The quantity sold

declined slightly from 74,800 tons to 72,000

tons, and losses increased by 35%. “During

the last 15 days of 1998, there was fierce competition

between us and Cimenterie du

Moyent Orient (CMO), and we had to reduce our prices by some $30, which caused a

devaluation of our stock of some $240,000,”

says Georges Ghosn, general manager. If you

take that devaluation out of the $564,000, you

end up with losses of about $324,000, similar

to 1998 figures. A subsidiary of Seament

Group, CMO has been refurbishing its factory

at a cost of $25 million to be able to produce

up to 400,000 tons.

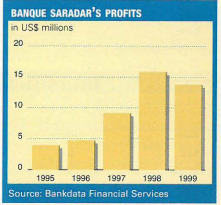

Foreigners

welcome

National Bank of Canada has taken a

15% stake in one of Lebanon’s top-tier

financial institutions, Banque Saradar. The

$22 million purchase will raise Saradar’s

capital from $70 million to $90 million.

“Banque Saradar is set for expansion,” says

Elie Saliba, NBC’s general manager in

Beirut. NBC, the sixth largest bank in

Canada with $70 billion in assets, hopes to

expand its presence in Lebanon. “Foreign

banks cannot compete with well-established

local banks,” says Saliba. And foreign banks

face limits when it comes to expanding their

branch networks. Buying into Lebanese

banks can also be a launching point into the

region. In 1998, the International Finance

Corporation paid $11 million for a 10%

stake in Saradar. It is strong in corporate and

private banking and wants to acquire or

merge with another bank to boost retail

activities. Still in the top ten for profits, its

earnings dropped over 13%, from $15.8 million

in 1998 to $13.6 million last year.