Y ou don’t have to pick up a copy of

the National Enquirer to know

that insurance firms are going to

bed with banks these days. The megamerger

of Citicorp and Travelers Insurance

Group created the $700 billion giant

Citigroup almost two years ago, and

helped precipitate the blurring of lines in the

US financial sector – a trend that was

already well established in Europe.

France-based insurer Axa, for example,

has an asset management portfolio of $700

billion, making it the fourth-largest money manager after Union Bank of Switzerland,

Fidelity and Credit Suisse.

Here in Lebanon, the business of banks and

insurance companies is also coming closer

together, albeit on a smaller scale. “It’s the

future. People are looking for a one-stop

shop, and banks are creating a sort of financial

supermarket,” says William Salem,

head of marketing for SNA, the first insurance

firm to start selling insurance in banks.

SNA has created a worldwide group accident

policy, which it sells to banks, and has

developed a complete line of retail insurance

products that are sold at Banque Audi and

BBAC, both shareholders in SNA.

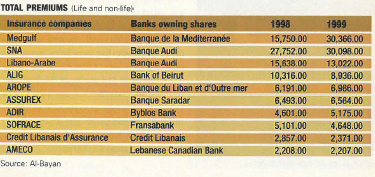

At least ten banks have started their own

insurance companies while others are buying

into existing insurers. Banque du Liban

et d’Outre Mer is a major shareholder in

Arope; Byblos Bank owns all of ADIR;

Banque Audi has a I 0% stake in Societe

Nationale d’ Assurance (SNA) and is finalizing

its recent acquisition ofLibanoArabe.

So what do these profit-driven partners get

out of this love affair? Insurers are the first to

benefit. Banks throw a constant stream of

business their way. Insurance companies

that are owned by banks are guaranteed captive

business. Before granting a loan, a bank

usually requires a client to purchase one or

more policies. These policies virtually

ensure that a bank will get back its money. A

personal loan is accompanied by life or disability

insurance. Car loans must come with

automobile insurance. A housing loan generally

comes with life insurance as well as fire

or natural disaster policies. “This is our

bread and butter,” says Fateh Bekdache,

general manager of Arope insurance.

“Everyday the bank’s branches are open, I’m getting cash business,” he adds. In 1999,

at least a third of Arope’s $5.5 million portfolio

was captive business, policies that

BLOM clients were required to buy.

Most of the insurance pobcies that are

sold through banks, such as life, fire and

marine, are the most profitable forms of

coverage. At least half of ADIR’s $5.2 million

portfolio in 1999 was in life, and the

firm’s earnings were $1.6 million.

Insurance companies that rely on banks for

business are also able to lessen their

reliance on the volatile and high-risk market

for medical coverage. “We’re not interested

in hospitalization,” says Jean Hleiss, general

manager of ADIR. “Others are building

their market share on [hospitalization] and

that’s why they are losing.” But medical

policies account for 33% of Arope’s business.

Although a third of that is BLOM’s medical group, the insurer’s heavy reliance

on health coverage has taken its toll on

profits. Out of $5.5 million in revenues in

1999, earnings were less than $475,000.

Insurers receiving captive business from

banks do away with long collection periods

and receivables. Collection problems have

contributed to the collapse of more than one

insurance firm. With banks, all payments are

made in cash. The insurer has no receivables.

At least 80% of ADIR’s portfolio comes

from Byblos Bank, which pays upfront.

“When BLOM issues a loan, they take the

money for the insurance from the customer

and give it to me,” says Bekdache. “We get

paid ahead and the balance is always zero.”

And by relying on a bank for business,

there are no broker’s charges. ”The commission

rates in our business are very high,”

says Bekdache. “I don’t have to pay that for

business coming from the bank.” Many brokers

are not reliable payers. They tend to

demand extended payment terms for clients

and, says Joseph Issa, lawyer for Middle

East Assurance and Reinsurance Company,

“some brokers don’t pass on everything

they collect from the clients. They pay the

money they’ve collected in parts even

though the client has paid up.” At the same

time, brokers often transfer portfolios from

one company to another every time they

find a better deal. “If you depend on a broker

who has a very large portfolio and he

decides to leave, you have a problem,” says

Bekdache. Arope has already reduced its

broker-based business from 33% of its total

sales to less than 20%.

The banks also benefit from the relationship

by getting a share in the profits. Byblos

Bank is entitled to the $1.6 million in earnings

made by ADIR. BLOM gets 90% of Arope’s profits. “We look at it as an investment,

a diversification of the bank’s products,

which leads to additional profits,”

says Faisal Nsouli, head of research and

development at Byblos Bank. “We rely

heavily on life and homeowner policies.

Having a bank-owned insurance company is

more efficient and more reliable.” At the

same time, banks are able to tailor insurance

products for their clients. A fi vi::-year pt::rsonal

loan can be guaranteed by a life insurance

policy for the same period.

But there are downsides to the bank-insurance

company connection. An insurer that

depends solely on a bank to provide it with

business is restricting its own growth. And in

the insurance business, as your portfolio

grows, your risk diminishes. “It’s not healthy

to depend on the bank all the time,” says

Bekdache. “Direct business will generate

more for you.” About a third of Arope’s total

revenues, or $1.8 million, came from direct

sales in 1999. ADIR is also considering stepping

out of Byblos Bank’s shadow and

expanding into direct sales. “We are seeking

to increase our market share as well as

exploring new markets,” says Hleiss.

There are those who believe that this type of

marriage between banks and insurers denies

consumers the basic right to choose to do

business with another insurance company.

”Banks are actually pushing clients to buy

insurance from companies, which are either

theirs, or with which they have made

arrangements,” says Abraham Matossian,

chairman of Al-Mashrek. “It’s a package deal

and the client cannot refuse. Bancassurance is

important abroad, but the client is not obliged

to accept what the bank offers. He can either

accept what’s offered or go with another

insurer. Here there is no choice.”