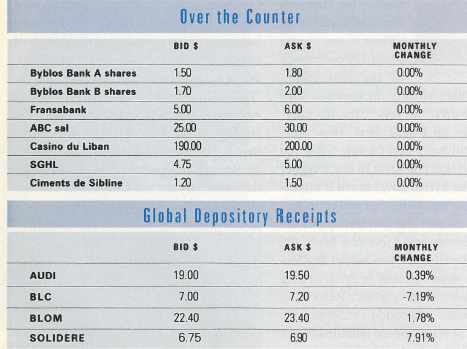

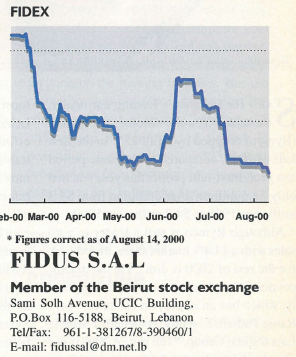

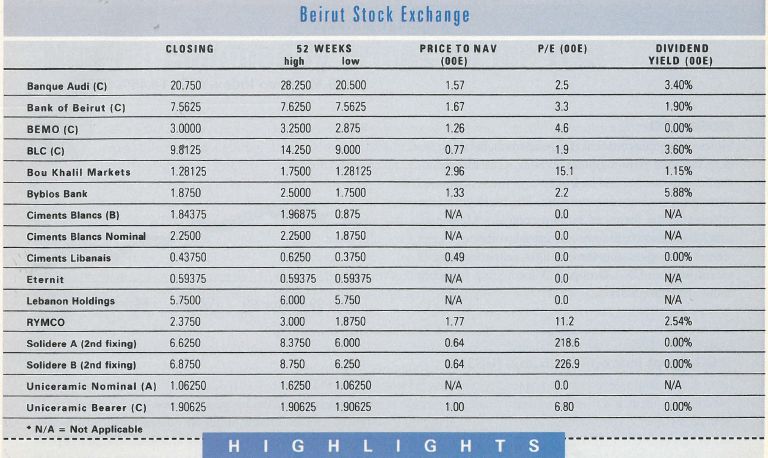

SOLIDERE

The general investor sentiment

toward the Lebanese GDRs

remains unchanged with local and

foreign investors waiting for the

upcoming elections for an efficient

macroeconomic policy. Solidere’s

GDR rose 15.28% to $6.225 (14/7)

as investors perhaps smelled a bargain,

only to fall back 3.61 % to $6

(21/7), then again drop 7 .5% to$ 5.55 as the economic condition worsened

with no signs of relief from the depressed real estate sector (28/7).

By early August, Solidere’s GDR edged up 0.9% to $5.6, as prince Al

Walid reconsidered plans to build a $250-million Four Seasons hotel,

as well as a residential apartment complex in downtown Beirut (4/8).

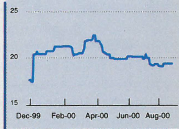

AUDI

Audi’s GDR was no different than

the rest of the GDRs or for that mat-

25

ter the economy in general with the

macroeconomic conditions still on 20

the downside and political instability

due to the elections putting the economy

on hold. Audi’s GDR was 15

priced at $19 .18 ( 14/7) and remained

there for a week (21/7).

By the end of July, news from the ministry of finance on the state of the

public deficit discouraged investors even more, driving Audi’s price

down 1.2% to $18.95 (28/7). Nevertheless, Audi regained some of its

losses as it was chosen as the best bank in Lebanon. It rose 1.58% to

$19.25 (4/8), and stayed at that level till mid-August (11/8)

BLOM

BLOM’s GDR held firm this

month despite several negative

economic reports by S&P, EIU

(Economic Intelligence Unit) and

the ministry of finance, which

pushed most of the Lebanese

GDRs listed on the international

down as foreign investors

interest was slowly fading.

BLOM’s GDR remained at $22.5 for the second half of July

(14/7)(2117)(28/7), mirroring the stagnation of the local economy. It

then edged up 2.22% to $23 ( 4/8).

By mid-August, BLOM’s GDR lost $0.1 to $22.9 as investors cashed

in the gains (l 1/8)

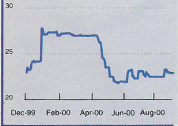

BLC

BLC’s GDR had the poorest perfor- 15

mance among all the GDRs losing

almost 7 .5% of its value in the past 12

four weeks. BLC’s GDR fell 0.32%

to $7.65 (14/7) as the economy 9

showed little growth and debt servicing

exceeding public revenues 6

for the first time, with the deficit

sp~nding ratio reaching 53% in the

first half of the year. Investors’ fear from a possible S&P downgrade was

revived, sending BLC’s GDR down 0.65% to $7.6 (28/7). A report from

the Economic Intelligence Unit (EIU), warning about the deteriorating

economic conditions pushed all the GDRs down; BLC dropped 6.58% to

$7.1 (4/8) and remained there (11/8).

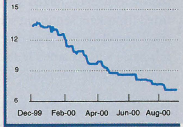

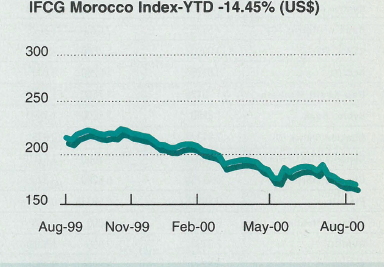

MOROCCO

Moroccan equities conti1’°ed to head south, breaking the

~ey 700-point psychological level as weak macroeconomic

performance and lack of foreign funds continued

to weigh negatively on sentiment. The highlight of the

month was the listing of mining company Managem,

which managed to add some interest to an otherwise quiet

market. Managem stole the limelight, outperforming its

parent holding ONA Group, and accounting for a big

chunk of trading activity.

EGYPT

The Cairo Stock Exchange continued to lose ground, suffering

another month of severe losses with institutional

investors remaining mostly on the sidelines. The lack of positive

economic news and continuous pressure on the pound

has caused the market to decline almost 40% so far this year.

Trading activity was mostly concentrated in the telecom sector

with the successful closing of Orascom Telecom’ s ( OT)

IPO, which was 1.7 times oversubscribed. OT’s attractive

pricing (EP55.568) prompted many investors to sell stakes

in MobiNil (-3%) and invest instead in the new issue.

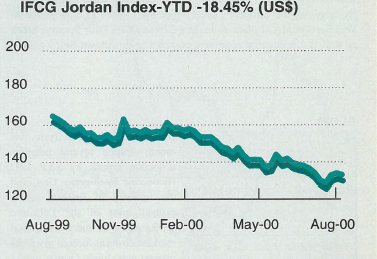

JORDAN

Investors at the Amman Stock Exchange welcomed the

modest rebound in share prices at the end of July following

weeks of consecutive declines. The small upturn was

primarily driven by an impressive rise in the Arab Bank

shares. However, mixed semi-annual results for most

listed firms kept sentiment subdued with the index hovering

around the 140-point psychological level. Mixed performance

was recorded in the insurance, industrial and

banking sectors, while the services sector lost ground