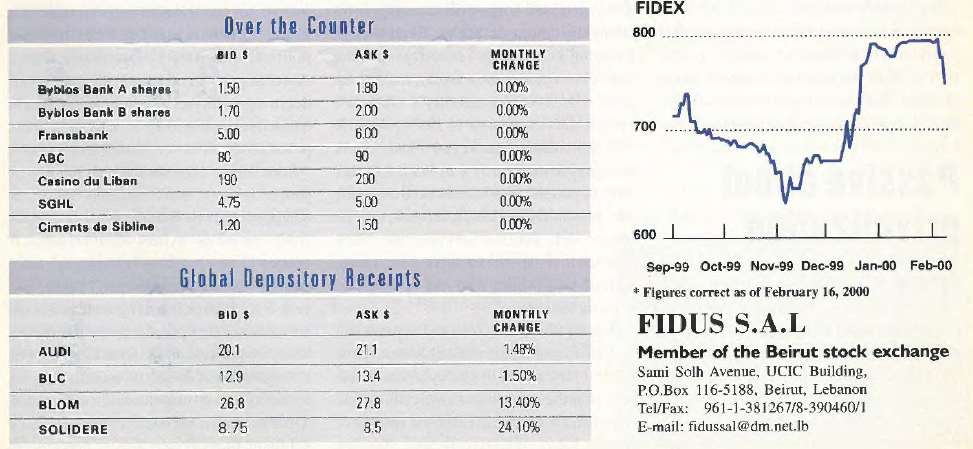

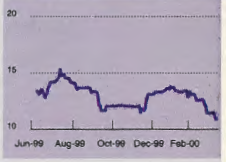

In the middle of January, Solidere

- Lebanon’s real-estate giant –

released a list of projects that it

had been pursuing throughout the

past year. The firm confirmed

that it had completed the final

Jun-99 Aug-99 Oct-99 Dec-99 Feb-00 phase of infrastructure work and

finished the renovation of 90% of

ancient buildings in the downtown area. Solidere also confirmed

continued advanced work on the Saifi residential project, as well

as the initiation of environmental work by the US firm Radian

International on the Normandy landfill. Solidere’s GDR witnessed

much fluctuation in January, whereby its price varied

between a low of $8.7 and a high of $8.8.

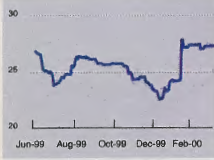

BLC

Banque Libanaise pour le

Commerce enjoyed a rather rocky

month that saw it subdued by negative

sentiments following its declaration

of 1998 profits of a loss of

$4.3 million.

The bank attributed the loss to a

$16.5 million increase in provisions

and doubtful loans, which

amounted to $24.1 million.

The Bank’s GDR suffered throughout the month, whereby its price

spiraled downwards, dropping consistently from $13 on January 17,

2000, to a low of $10.85 on January 16, 2000, representing a 19.8%

drop in the GDR’s price.

BLOM

Lebanon’s largest bank in terms of

assets and customer deposits,

Banque du Liban et d’Outre Mer

SAL, declared net profits of

$70.43 million for 1999, a 20%

rise over 1998 results. Return on

Average Equity stood at 28.6%

while return on average assets was

1.46%. Total assets reached $5.08

billion, up 10.9% from 1998. Customer deposits amounted to $4.33

billion, a 12.2% rise year-on-year, while loans rose 12.49% to

$1.107 billion. BLOM announced that the results were due to a conservative

lending policy, cost containment and the launch of retail

products and services. Merrill Lynch reaffirmed its long-term “Buy”

recommendation for the stock and it also announced that it expects

the bank’s income from retail products to grow significantly in 2000

compared to fees generated from loans and trade finance.

AUDI

Bank Audi SAL, one of Lebanon’s

top five banks, declared consolidated

net profits of $38.1 million in

1999, an 11.3% decrease from 1998

adjusted figures. Return on average

equity stood at 17.1% while return

on average assets was 1.23%. Total

assets reached $3.246 billion, up

9.88% from 1998. Customer

deposits reached $2.69 billion, an

11.07**%** rise year-on-year and loans rose 0.27% to $862.2.

The Bank attributed the decrease in results to the prevailing economic

recession as well as to the cost of expansion and development.

Following the Bank’s annual earnings results, Merrill

Lynch raised its medium-term opinion on Bank Audi’s GDR from

Neutral to Accumulate, and recommended the stock as a long-term

“Buy”.

MOROCCO

A surge in turnover, led by block deals, failed to pull the

Casablanca Stock Exchange (CSE) out of negative territory

last month with year-to-date losses totaling 4.8%.

The bourse was occasionally led higher by gains posted

by the subsidiaries of the conglomerate ONA Group.

However, these gains were short-lived as the market

succumbed, driven by losses in major stocks including

Ciment du Maroc, Samir, and SMI. Although the surge in

trading activity indicates potential signs of recovery, the

market is still in need of more liquidity to be injected by

large local and foreign institutional investors to pull it out

of the doldrums.

EGYPT

Strength in the cement sector and renewed interest in a

score of blue-chip issues, along with news of falling inter-bank

rates, consolidation and privatization in certain sectors, propelled

the Cairo Stock Exchange (CSE) into positive territory.

Several reports pointing to the privatization of Telecom

Egypt with an initial tranche of 10% slated for the second half

of 2000 also added positive sentiment to the market. The stabilization

in inter-bank rates at around 15% alleviated concerns

of a rising interest rate environment following the US

Federal Reserve’s decision to hike the overnight borrowing

rate by 25 basis points in early February.

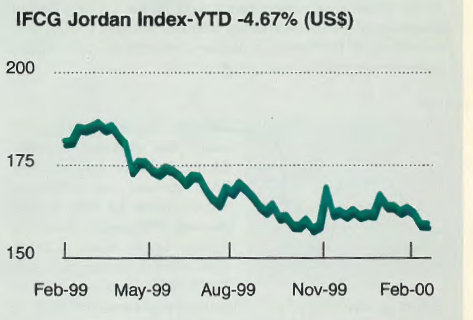

JORDAN

The Amman stock exschange recorded substantial losses

on the back of steep declines in leading industrial and

banking blue chips. The banking sector led the decline as

the heavyweight Arab Bank share lost ground after

announcing a marginal rise of 0.9% in 1999 net profit to

$225.6 million, triggering a selling spree among foreign

funds. In the industrial sector, the Jordan Phosphate

Mines Co. dropped steeply dragging the whole sector with

it. However, trading activity was strong thanks to the government’s

continued divestiture of its holdings in Arab

International Hotels as part of its privatization drive.