Trading places with Adonis Insurance and Reinsurance

(ADIR) would be an irresistible proposition to many of

Lebanon’s insurance companies. The company knows

how to tum a profit and, let’s face it, at the end of the day that’s what

business is all about. In the eye of the hurricane that is Lebanon’s

turbulent insurance sector, ADIR operates as if completely

immune to the surrounding mayhem.

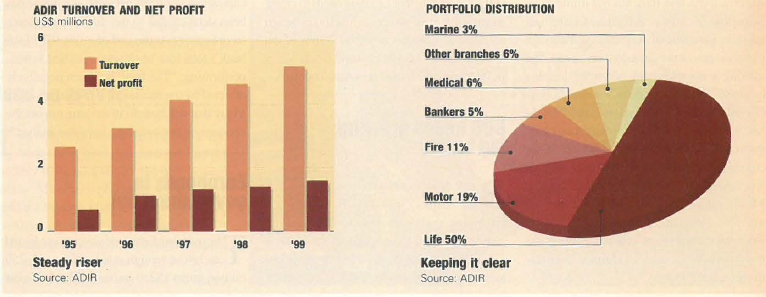

Accounting for less than 2% of the $400 million in life and nonlife

premiums sold last year, ADIR ranks 16th overall with a portfolio

of just $5.2 million. That’s up almost 100% from $2.7 million

in 1995. The increase in premiums has been more than matched by

profits, which rose by 135% from under $700,000 to $1.6 million

in the same period. So how does ADIR do it when the industry has

been caught in a nasty storm?

The insurance firm’s strength is derived largely from its parent company

Bank Byblos, which provides more than 80% of business.

Lebanon’s second largest bank in terms of profits and third largest in

deposits and assets, Byblos has demonstrated its prowess on more than

one occasion, especially with the unprecedented leap to become the

first to offer retail products such as personal loans, mortgages and certificates

of deposit in the early 1990s. The bank’s retail products include

insurance policies guaranteeing that whatever happens the bank

will get its money back. That resulted in net advances to customers

totaling nearly $1.44 billion last year. But being approved for that housing

or car loan is an unlikely prospect without the purchase of

accompanying insurance policy from none other than ADIR.

But ADIR isn’t unique in this respect (see “Come together,”

September 2000). More than ten of the banks have established

their own insurance companies, including Banque du Liban et d’Outre

Mer (BLOM) with Arope. Others, like Banque Audi with Libano

Arabe, have either completely acquired an existing insurer, or, Like

Bank of Beirut with Arab Lebanese Insurance Group (ALIG), have

taken a partial stake in an insurer.

ADIR’s strategy is simple. It takes advantage of the captive business

through Byblos by keeping costs low. ADIR need not worry about investing

in real estate since Byblos has over 50 branches that double as a source

of business for the insurer. “We are everywhere without needing to have

so many branches,” says Jean Hleiss, deputy general manager of ADIR.

“And our staff is very small compared to the market, so that cost is also

reduced.” ADIR has no need for sales agents or office personnel.

Profits remain in-house, instead of large chunks being handed out as commissions.

The savings are substantial since brokers take as much as a 60%

cut on premiums in some cases. “If you Look at insurance companies that

are owned partly or completely by banks, you’ll see they have either

small- or medium-sized portfolios,” says Fateh Bekdache,

general manager of Arope insurance. ‘They’ re all comfortable if you look at

their balance sheets. All captive business, zero receivables, they get paid upfront

and at the same time it generates business on a daily basis.”

ADIR also focuses on its bottom Line by doing a balancing act with

its portfolio, which is heavily weighed in the more profitable lines.

Life insurance – the most profitable – constitutes about 50% of premiums

at more than $2.6 million. That puts ADIR fourth in the

Lebanese market after American Life (ALICO) with $51.7 million,

Societe Nationalc d’ Assurance at$ I 0. L million and Libano Suisse with

$2.9 million. But, with the exception of ALICO, none are so heavily

weighted in life as ADIR. “It’s not a secret, life insurance is a very

profitable business,” admits Bekdache. “Nowadays it’s probably the

only profitable business.” Credit Libanais d’ Assurance (CLA),

owned by Credit Libanais, similarly handles the bank’s insurance

needs with over 55% of its $2.3 million portfolio in Life, and made a

tidy net profit of $912,000 in 1999.

At the other end of the spectrum, ADIR keeps unprofitable and

volatile medical at a minimum. Just 6%, or about $300,000 of its

business, is generated from medical insurance. That makes ADIR

31st in a market that averages 50% for the medical line. “It’s a losing

product,” says Hleiss. “Our hospitalization is limited and we

only cover people who are completely insured with us. We are not

interested in having hospitalization plans, and that’s one of the main

reasons behind our profits. “AI-Fajr, for example, has a portfolio

about the same size as ADIR’s at $5.6 million. But 39%, or $2.2 million,

of Al-Fajr’s portfolio is in medical resulting in profits of less

than $160,000 in 1999 (see “Profits not insured,” July 2000).

That’s a profit margin of3%, and only LO% of ADIR’s profits. Even

tiny Middle East Assurance and Reinsurance company

(MEARCO) with a portfolio of $1. l 3 million managed $159,000

in profits – a result of staying out of medical insurance. CLA doesn’t

even provide medical insurance unless it’s a client of the bank

or someone who has purchased other policies from the insurer.

But perhaps the best part of ADIR’s arrangement is what it means

to collection. Most insurers have to resort to drastic measures in order

to sell, including allowing extended credit facilities. While the

average collection period of the market fluctuates between four and

five months, there are many that allow as long as a whole year. ADIR

doesn’t have to deal with all this nonsense. ALI its accounts are closed

at the end of each month, meaning no receivables, which translates

into liquidity. Collection for insurance is included in loan payments.

That means premiums are secured with collateral along

with the loans themselves. Regardless, they hardly have to worry

about defaults on payments. Since captive business results from loan

applications, the second the client fails to pay the insurance premium

their credibility with the bank is jeopardized. “The bank will

assume the client will not make good on its payments on the loan

either,” says? Elie Torbey, manager of the life and bancassurance

departments at CLA. “They will take corrective measures.”

Other companies have to chase down their money. Some even have

receivables that exceed half their sales. “We don’t allow that,” says

Hleiss. “It reduces our expansion but we have made a choice. We

sacrificed expansion but we collect our money.”

Even with these advantages ADIR seems to operate in a naturally

protective mode. “In all our business we do very selective underwriting,”

says Hleiss. “For life insurance we ask for exams. Every

file is studied by us, our doctors and our reinsurers.” This reduces

the loss ratio. “I know some companies don’t do this for small

amounts, and these cases have a tendency not to disclose all the

facts,” he says. When a claim comes in the insurer might deny payment.

ADIR wants all the cards on the table upfront. “If you don’t

do that you’ll lose,” warns Hleiss. “We insist on having everything

clear at the beginning and we pay without questions. We have to

be cautious because we have the bank’s name to protect.”

ADIR’s success can’t simply be put down to its relationship with

Byblos. Not all insurers that are associated with banks are doing as

well. Over 50% of Arope Insurance’s $5.5 million portfolio is either

captive business from BLOM, or the bank’s products, yet their

profits for 1999 were just $474,000. A third of this insurer’s total portfolio,

or $1.65 million, is in medical. And direct sales-meaning neither

the bank nor brokers are involved-account for 30% of its portfolio,

while broker business comes in at 15%. That translates into

commissions, salaries and real estate expenses.

There are those who argue that catering solely to a bank’s needs

has its downsides. Allowing for other sources of business can be

important to increase a portfolio. “It’s not healthy to depend on the

bank all the time,” says Bekdache. “Direct business will generate

more income for you.” Salam Hanna, general manager of Libano

Arabe, which caters to Banque Audi, concurs: “Of course you have

a much faster collection, but it’s harder to grow your portfolio.”

CLA is a good example of a company that has found a balance

between bank business and outsourcing. While handling captive

business from its parent bank, it also provides services to over a

dozen other financial institutions, specifically in the area of credit

card covers, one of the factors that has led to the firm’s growth

beyond solely catering to Credit Libanais.

All in all, ADIR ‘s strategy is elegant. It avoids the hassle of collections,

cuts costs and has a constant flow of business. Sure that

has its limitations, but considering ADIR’s returns, who cares

about limitations.