W orld commodity prices

have strengthened signifi-

– candy since mid-1999, as

evidenced by the 25% rise in the IMF

index of primary commodity prices in

the past 12 months. While much of the

credit for this recovery goes to the

upturn in oil prices, non-fuel commodities

have also shown strength this

year with the index of non-fuel commodity

prices rising by 5% over the

nine months to June this year.

However, non-energy prices have yet

to recover fully from their late 1990s

slump when they fell by as much as

25% over the period between the beginning

of 1997 to the middle of 1999. The

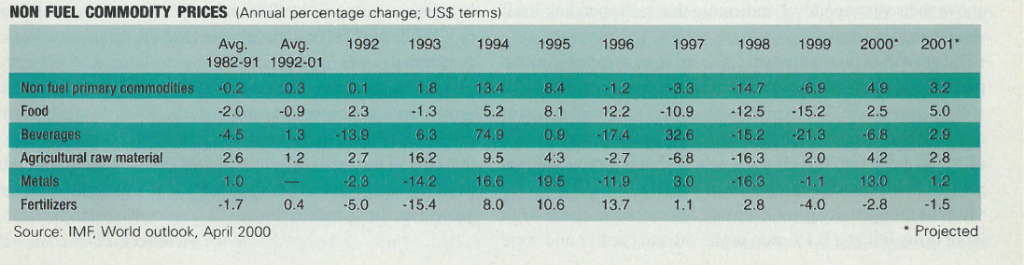

IMF non-fuel commodity price index fell

by 14.7% in 1998 alone. Prices are

expected to continue the recovery that

started in 1999, due to stronger economic

growth and reductions in excess

supply of certain commodities.

Cycles are the dominant feature of

movements in world non-oil commodity

prices, challenging policy makers in

many developing countries that depend on

primary commodity exports. This last

cyclical decline has been more severe

than the previous two declines in the

early and late 1980s due to the more pronounced

than usual concurrence of

strong supply and demand shocks. The

slowdown growth in global demand during

19’97 /98 coincided with continued

production increases. Most of the decline

in non-energy prices was due to the Asian

crisis and the recession in Japan, especially

as several of the Asian countries were a

major source of demand for primary

commodities prior to the crisis. At the

same time, production of many commodities

had continued to increase at a

rapid pace, owing to technological

advances that cut production costs. In the

case of metals and fertilizers, oversupply

by producers to make up for the reduction

in revenues maintained the downward

pressure on prices. For certain agricultural

commodities, prolonged periods of

favorable weather in the US and Europe

have resulted in particularly good harvests,

preventing major rises in price.

The recent pickup in non-fuel commodity

prices is due to a reversal of the

supply/demand factors that triggered

the decline. World economic growth is

expected to be around 4% in 2000,

higher than initially expected, and supporting

a recovery of commodity

prices. However, while non-fuel commodity

price indices appear to have bottomed

out last summer and raw material

prices are increasing as the world

economy revives, the recovery is likely

to be slow. Stocks for most commodities

are still relatively high, and new capacity

is coming on stream. This means

that it will probably take longer than

usual for the upturn in demand to translate

into a significant increase in prices.

According to the IMF, non-oil commodity

prices are projected to increase by

5% in 2000 and between 3% to 4% in

2001. One important distinction

between the recovery in oil prices and

non-oil commodities as a group is that the

upturn in oil prices, while supported by

the recovery in world demand for oil, was

mostly driven by significant supply cuts

by OPEC and other oil producing countries.

On the other hand, producer cartels

in other commodity markets have largely

failed and producers in these markets

are unable to follow OPEC’s example in

reducing excess supply. Ample capacity

exists in countries producing non-oil

commodities, be it metal, phosphate,

petrochemicals and potash. Production

volumes should continue to ·rise in the

remaining part of 2000 as a result of the

ambitious expansion programs introduced

prior to the Asian crisis and a general

upturn in demand.

For exporters of non-fuel commodities,

the net effects of this year’s projected

increase in price hinge on the specific

commodities they export. The prospects

for Arab countries that depend on

exports offertilizers, such as Jordan and

the Gulf states, remain subdued.

According to the IMF, fertilizer prices fell

by 4% last year and are expected to

decline further, albeit at a slower rate, this

year (2.8%) and in 2001 (1.5%).

However, the surge in oil prices and

stronger economic growth worldwide

may initiate an earlier recovery.