Al-Mashrek has its sights set on

becoming the top insurer in

Lebanon – and not just in terms of

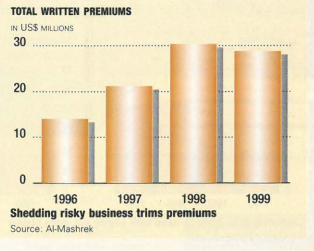

premiums. Already ranked sixth in the country

last year with non-life premiums of

$14.5 million, Al-Mashrek’s global business

was about $29 million in 1999. That’s an

increase of more than 100% from $14 million

in 1996 (see graph). Al-Mashrek is now getting

ready to tackle the 21st century. The company

is aiming to expand both locally and

abroad, where already 50% of its business is

generated. But that won’t be so simple.

The insurance market is no longer the

carefree, anything-goes sector it once was

(see “Premium Pressure,” March 2000).

The players are faced with many new

obstacles, such as consolidation and new

government solvency requirements. Then

there are the foreign big hitters who have

moved in: Assurance Generale de France

(AGF) now owns 51% of Societe Nationale d’ Assurance (SNA), the third

largest insurer with non-life premiums of

about $20 million, while Axa bought 51%

of Societe Libano Française (SLF), the

fifth largest at $18.5 million. There are also

local subsidiaries of international firms,

such as Arab Lebanese Insurance Group

(ALIG), which is majority owned by its

parent company, Arab Insurance and

Reinsurance Group (ARIG). These firms

have the financial strength to compete

aggressively in the Lebanese market, solid

international experience in insurance and the

advantage of having names that carry a lot

of weight. Banks are also joining in the

insurance game, posing a new threat.

That aside, insurers have to find a way of

satisfying market demand, despite the relatively

low purchasing power of the population.

This has forced some to quote rates

lower than they would like, despite liquidity

considerations, and offer extended

credit facilities. If companies don’t walk a

fine line, they could easily follow Mesir,

Income and Phoenix.

All this and Al-Mashrek

doesn’t appear

overly concerned. Why

so smug? Al-Mashrek

thinks it has what it

takes. Part of its strength

comes from its reinsurers.

These help determine

to a large degree an

insurance firm’s credibility.

The reinsurers

behind Al-Mashrek are … and Swiss Re of Switzerland. All are rated

triple A. Al-Mashrek’s pricing strategies

are just as sound. The firm sets tariffs for

each branch of insurance based on statistics

gathered from the markets in which it operates.

Based on volume of expected claims

and rates offered by competitors, Al-Mashrek

works to maintain a balance

between safe underwriting and a competitive

spirit. Some, like American

Underwriters Group (AUG), sell just

below the market norm, while ALIG seriously

undercuts prices (see “New kid on the

block,” July/August 1999).

But with their financial strength (ALIG

has $7 million in capital and AUG has $4

million) and strong reinsurers (ARIG has

$1.7 billion in total assets and $460 million

in shareholders’ funds), both should be

able to cover losses in the event of unexpected

claims. Bankers, Societe Nationale

d’ Assurance and Libano Suisse are much more conservative when it comes to pricing,

with some of the more expensive rates in the

market. Al-Mashrek’s prices fall between

the two extremes.

On the collection front, Al-Mashrek also

tries to maintain a balance between liquidity

and convenient terms for its clients. For medical

insurance, the riskiest branch, it will not

deliver a policy before receiving a deposit

equal to 25% of the premium. The firm

allows no longer than 45 days for full payment. Sixty days is allowed for other types of insurance,

except in cases where large amounts are

owed. “We have to be realistic,” says Naji

Habiss, Al-Mashrek’s new deputy general

manager. “Someone who buys $4,000 to

$5,000 worth of coverage

may not be

able to pay all at

once.” In such

cases, the limit is

set at three months.

“But we have to

make sure that the first thing we collect

is what we have

to put as reserves

with the government,”

he continues.

Lebanese United Insurance,

for example, demands 35% up front and a

maximum of two months to close the

account, well within the market average

of four months (see “Getting tough,”

January 2000). Middle East Assurance and

Reinsurance Co (MEARCO) leaves no

room for maneuvering, requiring all payments

up front (see “A sure thing,”

February 2000). Some, like Libano Suisse,

play it too dangerously, allowing clients

as long as five months to complete their payments

(see “The $8 million millstone,”

November 1999).

Although initially Al-Mashrek’s activities

were geared towards marine insurance, it

gradually realigned its business by extending

operations to all branches. Now, 35% of its portfolio is in medical and 5% in life. The rest is in general insurance. Of that 40%, or about

25% of Al-Mashrek’s

portfolio, is in motor

insurance. Dealing in

all branches of insurance

assures that the

firm won’t have to turn

away potential clients.

“Often we lose clients

for the branches we do

have,” says Rached

Rached, chairman of

MEARCO, “because we

don’t deal in other branches that the

client needs.”

With 35% of its business in medical, Al-Mashrek

will start working with an international

third party administrator (TPA)

which is in the process of registering to

operate in Lebanon. Though Al-Mashrek

doesn’t work with one, TPAs like Medical

Express and Mednet already handle the

medical portfolios of many Lebanese

insurers. A TPA manages its clients’ healthcare

portfolios and is responsible for ensuring

that the branch is efficiently run, that the

guarantees are in place and a sound level of

liquidity is maintained (see “Doctoring

insurance,” December 1999). With physicians

working full-time on their payroll, the

TPA will screen clients for pre-existing

medical conditions and make sure that hospitals

don’t overcharge the insurer or prescribe

unnecessary expensive treatments.

This way Al-Mashrek can avoid worrying

about the high-risk branch and focus on

the others.

A major advantage for Al-Mashrek is

chairman Abraham Matossian’s wealth of

know-how. With decades of experience in

the insurance field, Matossian is the current

chairman of the Association of Lebanese

Insurance Companies (ACAL) and was

heavily involved in the implementation of

the new law. He was also instrumental in

getting diplomas from Centre d’Etude

d’ Assurance accredited. This qualification

is essential for those who wish to work in the

insurance industry according to the new

government requirements (see “Corporate

medicine,” September 1999).

Al-Mashrek is also in the process of

restructuring its management, reshuffling

personnel to positions where they’re most

qualified. The firm is bringing in new blood

from other insurance companies, including

SNA, !’Union

Nationale and

Libano Suisse. One

example is Habiss,

who ran Libano

Suisse for more than

22 years, which

ranked fourth in

1999 with non-life

premiums of about

$19 million.

As far as the bank

threat is concerned,

Al-Mashrek is loading

its guns. It is

ready to do business

with all financial

institutions, unlike

insurance firms that

are owned by banks.

One example is

ADIR, which does 90% of its business through Byblos Bank. Banks look for securities against loans. Clients are generally required to buy insurance, ranging from car and cargo insurance to house and life insurance, depending on the type of credit. “Banks won’t give credit to someone if he doesn’t get insured,” says Habiss. “We’re creating all kinds of products for the banks’ needs.” This way Al-Mashrek can sell motor policies to those buying cars on credit and cover the dealer if the client defaults on payments.

Another advantage Al-Mashrek has over

local rivals is its business abroad. Through

affiliates and subsidiaries in Cyprus, Saudi

Arabia, Egypt, and France, the firm generated

$14.5 million

or 50% of its business

in 1999. Not

only does Al-Mashrek

bring

home the experience

derived from

those markets, giving

itself the tools

to face the new foreign

threat, but it

takes the battle to

the foreign firms’

home turf. Others

that have offices

abroad include

SNA and Libano

Suisse.

Al-Mashrek is

also seriously looking

at consolidation.

It is currently in negotiations for an acquisition with two insurance companies, though Matossian declined to disclose which ones. The move would increase the firm’s client base and assets as well as provide greater coverage of the market with an increased branch network.

“But nothing has been finalized,” says Matossian. “We aren’t even ready to apply for ministerial approval.” If it is finalized, the firm will have taken a solid step towards achieving its ambitions for growth.

But growth will also come from within. In

this sense, Habiss plans to put a greater

emphasis on life insurance, which now

accounts for about 5% of Al-Mashrek’s total

premiums. “It’s the most profitable of all the

branches,” says Habiss, “unlike medical,

which is like a running faucet with funds

flowing out continuously.” Many others

agree. “It’s the safest and most profitable

branch of insurance,” says Aline Kamakian,

general manager of Insurance Investment

Consultant (IIC). For this reason, MEARCO

hopes to acquire a company for its life

license within a few years.

Is it worth it? AUG seems to think so. It

acquired ELKA insurance, solely for its

life license. Al-Mashrek is also in the midst

of creating services that are so far unavailable

in the market. For example, those who

buy all-risk car insurance will receive a

loaner car for a few days should they have an

accident. For those with house insurance

that get snowed in, Al-Mashrek will have

the snow cleared, saving you the trouble

and saving money for them by avoiding

water damage claims. The firm also plans on

introducing a 24-hour hotline service for

emergency assistance. “I want to reach the

point where the name Al-Mashrek is as

well known as Pepsi-Cola,” says Habiss.

But in order to grow, Al-Mashrek believes

it has to go back a step first. It’s sacrificing

premiums by brushing off some bad and

high-risk clients in favor of a clean portfolio.

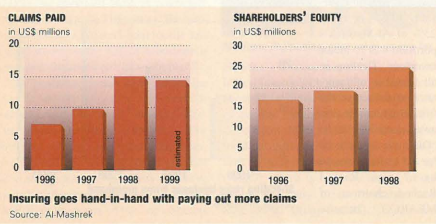

Though premiums generated locally have

increased from about $13.9 million in 1998

to $14.5 million in 1999, the non-renewal of

bad business contributed to a drop of $1.5

million in total revenues from $30.4 million

in 1998. With that, Al-Mashrek is seriously

screening all new business.

Talks are now ongoing with potential

new investors. “Al-Mashrek doesn’t need

big names to attract business,” says Habiss,

“but more liquidity can facilitate growth in

new ventures.”

Al-Mashrek is aggressive, but it does

not take the unwise risks that have brought

the downfall of others. It has also found a

balance to counter most of the sector’s pitfalls.

Al-Mashrek is confident that it is

taking the right steps. The question is

whether this will be enough to take the

business further.