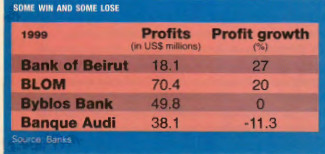

Lebanon’s heavies in the banking industry are starting to release their 1999 profits, giving hodgepodge results. Bank of Beirut and Banque du Liban et d’Outre-Mer (BLOM) came out with fine performances, earnings up 27% ($18.1 million) and 20% ($70.4 million) respectively. BLOM proved again that its conservative approach to banking can withstand the pressures of the economic slowdown and the tightening of the spreads as interest rates continue to decline. Along with BLOM’s loan-to-deposit ratio being low, its clients are mostly high-net-worth corps, which has brought its doubtful loans down to 6.27%, one of the lowest in the sector. It also aims well at cost control. From 1995 to 1999, its cost-to-income ratio has dropped from 56.8% to 38.3%, again one of the lowest in the banking industry. Additionally, it has the advantage of having the image of being a very safe bank: It is able to attract customers with low deposit rates, which maintain good deposit growth and a healthy spread.

“We are confident that we will achieve better profits this year,” says BLOM’s general manager Samer Azhari. He claims that BLOM’s track record of withstanding the pressure of economic slowdown and the steady drop in interest rates shows that the bank can continue healthy earnings growth.

But the harsh conditions have affected two leading banks. Byblos Bank ended up with its earnings flat ($49.8 million), while Banque Audi’s profits dropped 11.3% ($38.1 million) last year. Audi’s profit decline comes not only from economic pressure but from its aggressive expansion in retail banking and branch network. Audi opened 13 new branches in 1999, reaching 55, and has plans to open 12 more this year, which will put it way ahead of its competitors. “Audi has a strong management team and will benefit long-term,” says Fidus’ deputy general manager Rudy Sayegh. “But there is a price to pay to be the top innovator in products and services and expand rapidly with branches. This will pay off when the economy recovers, but when the economy improves is unclear.”

Reluctant MPT

The Ministry of Post and Telecommunications (MPT) is now the state’s second-largest source of government revenue after customs taxes, reporting $539 million in returns for 1999, a 37% increase over 1998. Largely responsible for the increase is the MPT’s ban on international calls made over the Internet and the tax hike on cellular calls. International calls increased 99% from 1998, bringing in $124 million, while the ministry collected $109.5 million in dues from international telecom firms.

The MPT also sold 110,000 fixed lines last year and restated its right to issue a third license for a cellular operator in 2002. Other plans for the medium term include setting up an independent telecommunications company, Liban Telecom, which will be 25% privatized. The draft law to create Liban Telecom is still in progress, and as yet the listing of the company’s shares is undecided, as well as whether to list the company’s shares on the Beirut Stock Exchange or sell them to a single strategic investor.

The ministry was also unclear on whether it will maintain management or give it over to the private partner. Says Lebanon Invest’s Nassib Ghobril, “Telecom is one of the government’s biggest revenue generators, so it’s a very sensitive and strategic sector.”

On the other hand, the government has also been slow in privatizing losing operations like Middle East Airlines. An analyst claims that the controversy of privatization is that it would result in layoffs of politically affiliated employees.

Upswing

Solidere can breathe a little more easily in 2000. After making losses of $435,000 for the first six months of 1999, the real estate company scraped into the black by year-end. Solidere’s white knight was Selim Kheireddine, chairman of Al-Mawarid Bank, who authorized the last-minute purchase of land and buildings for a reported $10 million in the Beirut Central District, near the site where Banque Audi’s new head offices are being built.

Solidere shareholders also have something to be happy about. After falling to a low of $6 per share in November, anticipation of a peace settlement pushed up Solidere stock 40% by January 24.

But still in disagreement over compensation terms are former BCD property owners and Solidere. In a development that may hinder the former, the government has closed the Concorde offices in Hamra, where the claimants’ cases were previously assessed before the largest and last properties were evaluated in an attempt to cut costs. “It was costing around $210,000 to keep those offices,” says Muhammad Mugraby, the lawyer handling the cases for the claimants. “The move is mainly in the best interests of the government.”

Meanwhile, Solidere reports that it has completed the final phase of the infrastructure work as well as finishing renovation work on 90% of the old buildings in the downtown area. They are continuing advanced work on the Saifi residential project, which they expect to complete by summer of 2000, disclosing that 35% of the units have already been leased. While all work on the second sea defense wall has been completed, the first is still only halfway done, though Solidere expects to finish it by the coming spring. This will make the reclamation of 608,000 m² of land for office and residential space and another 70,000 m² for a public park possible.

Let it slow, let it slow, let it slow

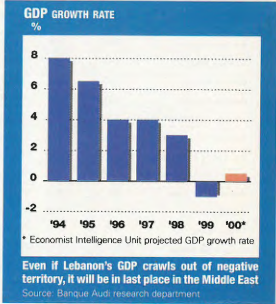

The Economist Intelligence Unit (EIU) recently forecast that the Middle East and North Africa region will have the second highest growth rate (3.5%) in the world due to the increase in oil prices. Its report on Lebanon, of course, has not been so favorable. EIU’s annual World Outlook report expected the Lebanese economy to grow at a low 0.5% rate this year, up from -1% in 1999, making it the slowest growth rate of any Arab country in 2000. Projected growth rates for other countries include Tunisia at 6.5%, Morocco at 6.3%, Egypt at 5.6%, the United Arab Emirates at 3.5%, Kuwait at 2.8%, Jordan at 2.5%, Syria at 2.3%, and Saudi Arabia at 2%.

In tune with Lebanon’s poor growth rate, the country’s vital statistics don’t look good. Government expenditures in 1999 reached $5.608 billion, with just $3.23 billion in revenues. The result is a budget deficit of 42.41% of expenditure, 2% short of the government-budgeted target but marginally lower than the 1998 deficit of 43.73%. The monthly deficit was 33.14% in December, up from 31.4% in November but down from 62.75% in December 1998. Expenditures increased by 6.92% over the previous year, and revenues by 9.41%. On the flip side, revenues from taxes on income and profit rose by 28% following tax hikes in the budget for 1999, while property tax revenues increased by 55%. The Ministry of Finance maintained that the aggregate revenues from direct taxes were 13.3% above expectations.

The M&A treat

Word has it that Jordan National Bank (JNB) will acquire Bank of Lebanon and Kuwait (BLK), a local bank that is owned by Lebanese and Kuwaiti investors. The acquisition would move JNB, already doing business in Lebanon, up to a medium-sized bank with nine branches and total assets of $200 million after absorbing BLK’s $87 million in total assets, which pulled in $1.2 million in earnings in 1998. If the deal is finalized, JNB, based in Amman, Jordan, will follow London-based Standard Chartered, which purchased a local financial institution just recently. In late 1999, Metropolitan Bank was scooped up by Standard, which bought a 75% stake.

But Schroders corporate finance manager Spiro Youakim says this is not the beginning of a wave of foreign banks buying out locals. He points out that Standard Chartered is simply returning, it left Lebanon in the early 80s, and JNB is enlarging its presence in the country, having already developed familiarity with the market. Most foreign banks that have an interest in Lebanon would like to see economic conditions improve before making an attempt to acquire local banks, adds Youakim.

However, most analysts believe that mergers and acquisitions between local banks will accelerate. Lebanon’s economic slowdown has put pressure on banks’ profits, down 3% on average earnings for the first three quarters among 13 leading banks. Interest rates on the way down and stiff competition in a saturated market have put a squeeze on spreads, also putting a dent in the sector’s profitability. “Small banks will not be able to withstand these conditions for a long time,” says Youakim. He expects small to medium-sized banks to be more open to M&As in 2000, and even though the central bank is against larger financial institutions merging in the near future, banks in the top tier will probably negotiate with each other as well.