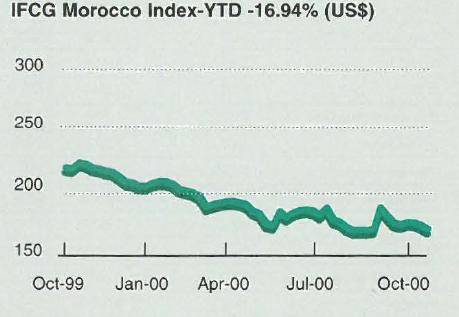

MOROCCO

The Casablanca Stock Exchange ended lower driven

by losses in leading shares as investors failed to

react to the announcements of first-half corporate results

that were somewhat in line with expectations. A

wait-and-see mood dominated the market as investors

kept to the sidelines awaiting the announcement

of promised reforms, including new incentives

for companies to list their shares on the stock market

and a series of tax breaks. Year-to-date losses now

stand at almost 17%.

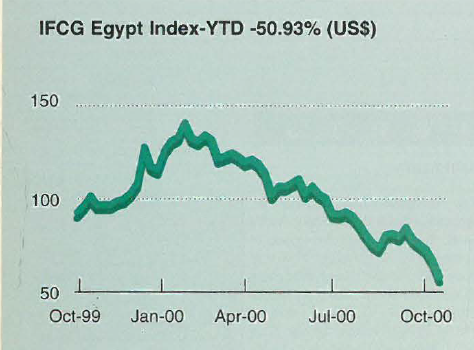

EGYPT

The rising political tension in the region and the continued

liquidity crisis combined to deal a heavy blow to

Egyptian equities, which shed almost 20% since early

October and are down more than 50% since the beginning

of the year. This was heightened by news that foreign reserves

retreated to $14.64 billion in July 2000, down from

$15.13 billion a month earlier, while the Egyptian pound

has been traded at almost EGP4 to the dollar. In an effort

to contain the foreign currency crisis, the Central Bank issued

directives limiting daily cash withdrawals of foreign

currency to $20,000.

JORDAN

A cautious mood continued to dominate the Amman

Stock Exchange following weeks of Israeli atrocities

in the Palestinian Territories, bringing year-to-date

losses to 21 %. The banking sector led the decline as a

result of a drop in Arab Bank, which is one of the market’s

largest blue chips in terms of capitalization. Nevertheless,

statistics show that around 150 foreign mutual

funds have been operating in the Amman Bourse

over the past three years. Net non-Jordanian investment

at the bourse between August 1996 and the end

of August this year amounted to $281 million, or

around 6% of total market capitalization.

The performance of the largest 100 Arab banks in 1999

The positive effects on Arab

economies of higher oil prices

from mid-1999 onward and the

ongoing structural adjustment programs

in the non-oil countries saw

Arab banks recording healthy returns in

1999, with few exceptions. The combined

net income of the 100 largest

Arab banks rose by 10.2% to $8.3 billion,

while their combined assets

increased by 4.2% on their 1998 level to

$526.3 billion. However, these assets

remain smaller than the assets of any of

the largest ten banks in the world. For

example, the assets of HSBC Group

alone were $569 billion last year.

Average return on equity for Arab

banks stood at 13.9%, with return on

assets and capital-to-asset ratios at

1.58% and J 1.3% respectively. The top

Arab bank in the region in terms of

equity, the Arab Banking Corporation in

Bahrain, ranked as number 161 among

the world’s largest l000 banks in 1999,

followed by Saudi American Bank,

which ranked as number 166.

According to Euromoney’s Top 100

Arab Banks survey, the seven largest

Tunisian banks recorded the highest

increase in combined net income in

1999, up 84%, followed by the top

Bahraini and Egyptian banks with earning

growth of30.5% and 25.2% respectively.

ln the Gulf, the banking sectors of Kuwait and Qatar fared

well, with the top banks in

each country posting profit

increases of I 0.8% and

5.7% respectively. In

Saudi Arabia, the combined

pretax profits of the

nine banks (excluding

National Commercial

Bank, which had not yet

released 1999 results) rose

by a modest 1.5%.

A comparison of return on equity ratios, a key measure of profitability,

places the five top Qatari banks

in the lead with 17.7% average return

on capital in I 999, followed closely by the

largest 14 Egyptian banks, which saw

their average return on capital rise from

16.2% in 1998 to 17.5% in 1999. Return

on equity for the seven Lebanese banks

fell to I 6.9% in I 999, from 18.1 % the

year before.

The banking sector ‘s concentration

ratio measured by the market share of the

top five banks in the region is relatively

high. In Saudi Arabia, two banks, the

Saudi American Bank and the National

Commercial Bank, hold almost 50% of

the sector’s assets. The National Bank of

Kuwait and the National Bank of

Bahrain each holds 30% of their country’s

respective banking assets. Egypt’s

four state banks have 50% of total

assets and control most of the retail network,

while in Jordan, the top five

banks control 80% of the assets.

Management of Arab banks has so far

been emphasizing mainly asset size and

market share, believing that the large balance

sheet on the long haul would guarantee

competitive advantage. Instead,

management objective in the new millennium

should be to maximize shareholders’

value. This necessitates shedding

off businesses where the returns do

not cover cost of capital and allocating

more resources to those activities that

add value over time. Enhanced profitability

could also be achieved by

reducing operating expenses through

the effective use of modem technology

such as the Internet, and seeking consolidation

with banks in the domestic

market or abroad.

Arab banks will have to understand

their products and their customers’

needs much better and invest more in

technology if they are to survive the

onslaught of new competition. And if

they were too slow to adapt, the consequences

could be detrimental. Look at

what had happened in just four years to

stock trading on the World Wide Web,

and note that the stock market with the

highest proportion of Internet trading is

not in New York but in Seoul.

Consolidation would reduce operation

cost, minimize duplication, boost efficiency,

spread the huge technology costs

over a bigger base and cross market products

on a larger scale. However, consolidation

has to be planned carefully and

motivated strategically to be effective.

Despite the few consolidation deals carried

out in the region in the last two years,

mergers and acquisition activity remains

sporadic. It seems Arab banks are unlikely

to pursue serious consolidation activity

unless they are forced to do so by their

respective monetary authorities.