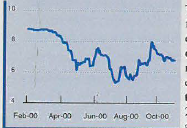

The political stagnation resulting

from the long break between the

end of the parliamentary elections

on September 3, and the appointment

of a new government by the

end of October, is taking its toll on

the market. Solidere’s GDR fell

2.41 % to $7 .075 (22/9), then fell

another 1.06% to $7 with the

materialization of S&P’s downgrades. International investors continued

trading cautiously as uncertainty surrounding the identity of the new

prime minister was still in question, though sentiment is leaning toward

Rafic Hariri. Solidere’s GDR lost 1.07% to finish the first week of

October at $6.925 (6/10). The escalating tensions in the Middle East

alarmed international investors who registered their concern by exiting

Lebanese GDRs. Solidere lost 2.17% to $6.775 (13/10).

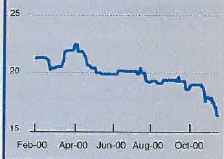

AUDI

Two downgrades from international 25

agencies negatively affected Audi ‘s

GDR, first S&P credit downgrade of ~

Lebanon’s sovereign rating, as well as 20

Bank Audi and two other banks, citing

concerns on the deteriorating public

finances. Audi’s GDR fell 1.06% to

18.65 (22/9). Rating agency Fitch

IBCA then downgraded Bank Audi’s individual

rating, voicing concerns that asset quality will be affected by the

ongoing economic recession. Audi tumbled 4.83% to $17.75 (29/9). It then

fell another 2.37% to $17.33 (6/10) as international investors saw the political

stagnation, resulting from the transition of power, as negative and persistent

to Audi’s outlook. The increasing political instability in the occupied territories

crossed the border into Lebanon, driving Lebanese GDRs south, with

Audi’s GDR losing the most and dropping from 6.64% to $16.18 (13/10).

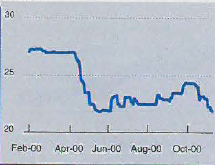

BLOM

S&P lowered its rating for BLOM

in line with the sovereign downgrade

as concerns mounted about

asset quality during the economic

recession. BLOM lost 0.72% to

$24. 125 (22/9), then plummeted

4.04% lo $23.15 after a volatile

week that saw its, price fall to

$22.85, but rebounded by the end

of the week on rumored foreign

buying. The economic and political freeze did not impress investors, but

BLOM attracted some buying leaving its price at $23 (6/10), a 0.65%

weekly decrease. The rising troubles across the border were immediately

seen by wary investors as the first signs of political instability in the

region. They sent BLOM’s GDR down 4.78% to $21.9 (13/10).

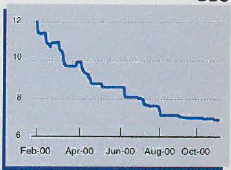

BLC

Going along with the market

sentiment, BLC’s GDR edged back

slightly, 0.36%, to $6.95 (22/9), as

the vacuum in the political arena

started 10 weigh on the economy.

BLC was not specifically affected

By the downgrade by S&P. The rating agency cited the overall

economic recession as the main reason for

the downgrade, while investors

believed that the old news was already reflected in the price. BLC held

its ground two weeks in a row (29/9) lo remain at $6.95 (6/10).

However, investors did not ignore the escalating tensions in the Middle

East that resulted in the halt of the peace process. BLC lost 1.08% to

$6.875 ( 13/10).

MOROCCO

The Casablanca Stock Exchange ended lower driven

by losses in leading shares as investors failed to

react to the announcements of first-half corporate results

that were somewhat in line with expectations. A

wait-and-see mood dominated the market as investors

kept to the sidelines awaiting the announcement

of promised reforms, including new incentives

for companies to list their shares on the stock market

and a series of tax breaks. Year-to-date losses now

stand at almost 17%.

EGYPT

The rising political tension in the region and the continued

liquidity crisis combined to deal a heavy blow to

Egyptian equities, which shed almost 20% since early

October and are down more than 50% since the beginning

of the year. This was heightened by news that foreign reserves

retreated to $14.64 billion in July 2000, down from

$15.13 billion a month earlier, while the Egyptian pound

has been traded at almost EGP4 to the dollar. In an effort

to contain the foreign currency crisis, the Central Bank issued

directives limiting daily cash withdrawals of foreign

currency to $20,000.

JORDAN

A cautious mood continued to dominate the Amman

Stock Exchange following weeks of Israeli atrocities

in the Palestinian Territories, bringing year-to-date

losses to 21 %. The banking sector led the decline as a

result of a drop in Arab Bank, which is one of the market’s

largest blue chips in terms of capitalization. Nevertheless,

statistics show that around 150 foreign mutual

funds have been operating in the Amman Bourse

over the past three years. Net non-Jordanian investment

at the bourse between August 1996 and the end

of August this year amounted to $281 million, or

around 6% of total market capitalization.