S ociete Generate Libano-Europeenne

de Banque (SGLEB) has reportedly

acquired the financially troubled lnaash

Bank in a deal worth $50 million. The

Central Bank had recently taken control of

lnaash after the J affal family relinquished its

84% stake. The bank had allegedly been in

violation of certain lending regulations.

SGLEB, which is half-owned by France’s

Societe Generale, will add 17 branches to its

30-branch network, vastly expanding the

reach of the financial institution and giving

it a presence in the South and Beirut’s

southern suburbs. “They were restricted in

opening new branches so they bought

lnaash,” says one banking analyst. SGLEB

is in an expansion mode. The bank has

moved into the Jordanian market and, a

couple of months ago, it purchased a

majority share of the local brokerage firm

Fidus. SGLEB registered profits of $18

million last year. lnaash had a capital of $10

million, assets worth $356 million and

$290 million in customer deposits in 1999

Safe bet

A rab Bank is planning a regular issue of

Investment Linked Deposits (ILD),

which will be offered with a choice of

indices. The US dollar-based deposits

guarantee that investors will not lose their

capital. The ILDs also, to some extent,

guarantee a certain return on an investor’s

money. The issue of the ILDs follows the

success of an earlier issue by Arab Bank. It

is linked to one or a basket of major

indices. These include the Nikkei 225,

Standard & Poor’s 500, Hang Seng or the

DJ Eurostoxx 50. “Instead of a fixed interest

rate, you get a return based on the

increase in the indices,” says Rim Zanabili,

senior relationship manager at Arab Bank.

“Once a new ILD is opened, clients have

four to six weeks to invest.” The minimum

deposit is $20,000.

Fast mover

A 1-Mawarid has become the first

Lebanese bank since the Israeli

withdrawal to open a branch in the former

occupied zone. The new branch is located

in Hasbaya. It has six employees and

serves a population of around 50,000 people,

including those living in outlying

.1 areas and villages. Only Fransabank –

which has been operating branches in

Marjayoun, Bint Jbeil and Jezzine since the

early ’90s – has had a presence in the

zone. “The next closest bank is at least a

half-hour’s drive away,” says Marwan

Kheireddine, AI-Mawarid’s chairman.

“Most of the local residents are middleclass

employees, so they are the ideal target

market for our retail products.”

Kheireddine is originally from Hasbaya

and his familiarity with the area and many

of the locals who live there helps assure that

he will have a loyal clienl base. The medium-

sized bank had profits of $1.1 million

in 1999, up a full 26.9% from the previous

year. Its assets increased by 32% to $30.19

million. Al-Mawarid has over 40,000

accounts and has extended 17,000 loans, averaging around $2,000 each.

Current accounts

Allied Business Bank (ABB) and

Societe Nationale d’ Assurance (SNA)

have launched a new set of bancassurance

products called H.imaya. The policies were

developed by SNA and will be marketed

exclusively by ABB to its clients. These

include savings-with-insurance plans for

education and retirement benefits as well

some traditional policies. ”We have to keep up

with the worldwide trend that makes it possible

for clients to handle all of their financial

transactions – namely banking, investment

and insurance – at one location, a sort of

financial supermarket,” says Nada Assaf,

ABB’s manager of research and development.

A number of banks in Lebanon have

either started theirown insurance company or

have bought majority shares in established

firms. Banque du Li ban et d’ Outre Mer is one

of Arope’s major shareholders and Byblos

Bank owns ADIR (see pp. 32).

The casino cashes in

Casino du Liban (CCL) saw profits

jump to $5.2 million in the first half of

2000, a 60% increase over the same period

last year. Profits were just $3.6 million in the

first half of 1999. Revenues for the first half

of 2000 totaled $42 million. The casino

saved some $5.4 million by renegotiating

contracts. It is also trying to change the contract

with Abela Development and Tourism

Company and the London Clubs responsible

for running the gaming facilities. But the

casino is not as lucky as it may seem. The

company owes the London Clubs some $5

million and the ministry of finance is

demanding that the casino pay $23 million

in back taxes from slot machine revenues, a

case that is now before the Shura council.

The new Audi

convertible

B anque Audi has launched a new threeyear

convertible bond linked to the

bank’s global depository receipts (GDRs)

and carrying a fixed rate of return. The bonds

are being marketed towards Audi’s retail

depositors. The minimum investment is

$1,000. The paper will offer investors a return

of6%, 7% or8% and are priced at$23.81, $25

and $27.03. Interest is paid semi-annually.

The GDRs’ issue price in 1997 was $27!. This

·marks the second issuance of convertible

bonds in post-war Lebanon. The first ones

were issued by Ciments de Sibline in 1996.

Retail depositors at Audi’s 61 branches will

have the right to exchange the bonds any time

during the paper’s lifetime. Over $75 million

in bonds will be issued. The first tranche, to be

sold in August, is not expected to exceed $30

million. ‘The timing is right because analysts

consider the bank’s GDRs undervalued,” says

Nabil Chaya, head of capital markets at Audi.

Rolling downhill

1999 suffered a drop of 17%. Until the end of

June this year, sales fell 28% compared to the

same period last year. Rymco’s shares,

which are traded on the Beirut Stock

Exchange, have been stagnant, just like the

rest of the stock market. They have

remained at or below $2.50 since the beginning

of the year.

Babv steps

S yria has taken the first steps toward

opening up its state controlled banking

system by granting three Lebanese

banks permission to open branches in the

country’s free trade zones. Societe

Generale Libano-Europeenne de Bank,

Fransabank and Banque Europeenne pour le

Moyen-Orient are allowed to provide banking

services to Syrian companies operating

within the free zones,

provided that each

bank maintains a

minimum currency

capital of $11 million.

But the move is

not likely to result in

any major financial

windfall for the

banks that open in

the zones, says

Maurice Iskander, an

analyst for Thomson

Financial BankWatch.

“There are only

about 700 companies

in the free zones,

most of which already do business with

Lebanese banks,” he says. “Yes, it’s interesting

to set up a bank there. How profitable

it will be, I don ‘t know.” But the

move could be a precursor to much bigger

reforms. The Syrian government is reportedly

studying legislation that will allow foreign

banks to open branches throughout the

country. Last month, Mustapha Miro, the

Syrian prime minister, announced that foreign

banks were welcome in Syria, as long

as they had a local partner. Reforming

Syria’s state controlled economy is

believed to be one of the top priorities of new

president Bashar Al-Assad.

Trade aid

The Arab Trade Finance Program (ATFP)

has extended to Byblos Bank and Credit

Libanais lines of credit worth $20 million

and $10 million respectively, to facilitate

trade transactions with Arab countries. ATFP

had previously granted the Lebanese government

a $40 mill ion loan for the same purpose.

The ATFP has so far granted several

Lebanese financial institutions a total of 37

lines of credit, worth some $251 million. The

Credit Libanais program includes deals to

import crude oi l, which could prove fruitful

should work resume on the refineries. “Loans

wilJ be given at Libor for six months and at

Libor plus 1/8 for one year. But the bank will

add a risk factor of 1 % to 2%, depending on

the project and the client,” says Georges

Khoury, assistant general manager of Credit

Libanais Investment Bank.

Bucking the trend

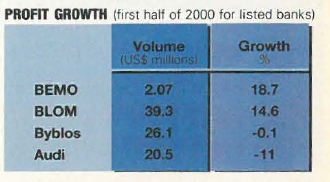

At a time when most banks are struggling

to maintain profit, Banque

Europeenne pour le Moyen-Orient (BEMO)

has been seeing some healthy earnings.

Profits for the sector dropped 13% in 1999,

but BEMO’s earnings shot up to $2.07 for the

first half of 2000, a full 18.7% increase

compared to the same period last year.

Customer deposits climbed 35% and total

assets increased 28.8%. While most

Lebanese banks are reducing the amount of

money they lend to private sector companies,

BEMO increased its lending 31 .4%.

“BEMO’s performance is obviously working

against the tide in the banking sector,” says

Nicolas Sawan, head of trading at Lebanon

Invest. The bank is also bucking the trend at

the Beirut Stock Exchange. While there is little

activity on the market, BEMO’s shares

climbed 8% last month, to $3.25.