Less than a decade ago, Sudan, the largest country in Africa, was hardly a blip on the business map. Today, it is one of the most talked-about emerging markets in the region and Africa. The opening-up of the economy earlier this decade and the peace agreement between the Khartoum government and the southern rebel groups have made it possible again to access the country’s oil wealth, resulting in a surge of foreign government officials and businessmen to Sudan.

Sudan’s current economic boom started in 1999 when it began exporting crude oil. This growth takes place despite strong internationally imposed sanctions, and in particular tough US sanctions, implemented since 1986 with new ones introduced in May 2007. Sudan has been able to sidestep these sanctions primarily because of China’s vast energy needs. The rapid economic surge Sudan has undergone was further bolstered in 2005 when a Comprehensive Peace Agreement (CPA) was signed between the northern National Congress Party (NCP) and the southern Sudan People’s Liberation Movement (SPLM), ending a brutal 21-year civil conflict. The CPA was arrived at under intense international pressure and this has meant that the agreement is weak, but so far sufficient. Maintaining peace has been a prime concern of both the northern and southern governments, despite high tensions between the two. National elections are planned for 2009 and both sides are keen to bolster their domestic positions and continue the ongoing “peace dividend”. If the CPA can be maintained Sudan is likely to continue its record-breaking economic growth. A settlement of still outstanding political issues, most prominently the Darfur conflict, would result in the lifting of sanctions, and increase the economic development even more.

Economic situation

Sudan has benefited greatly from its relationships with China, Japan and the Arab World. China currently gets around 5% of its total oil imports from Sudan and has invested $7 billion, mostly on oil projects and related infrastructure, in the country. Other major trading partners include Japan (9.2% of exports), UAE (4%), KSA (2.2%), and Egypt (1.7%). The scale of this economic growth is illustrated by the increase in foreign direct investment (FDI), which in 2000 stood at $312 million and in five years grew to an estimated $3.2 billion.

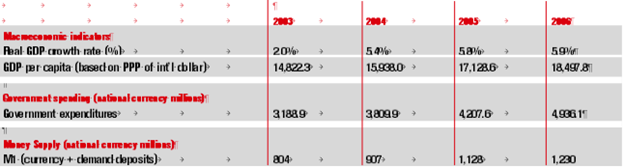

Exports grew by 17% to $5.65 billion, in 2006, as a result of increased oil production and high oil prices. Sudan has also increased its non-oil GDP by 10%, through a strong recovery in agriculture and expanded activity in manufacturing. These increases resulted in Sudan achieving 11.8% growth of real GDP and an overall GNP of $22.7 billion in 2006. For 2007, real GDP growth is estimated to be around 13.3%. Projections for 2008-2009 are for a real GDP growth rate of around 7%, as slower rates of oil output, a decrease in international oil prices and increased imports slow the pace of growth. Import spending is expected to increase in 2008 by 12% to $9 billion, from the estimated $8 billion that was spent in 2007. The oil boom is giving Sudan the necessary liquidity to finance mega-projects, such as the Merowe Dam, which, it is hoped, will translate into accrued contribution to economic growth at large.

In spite of this strong economic growth, due to shortfalls in expected revenues the Sudanese fiscal position deteriorated. The Sudanese economy is labored with heavy debt, estimated to be $26 billion in net present value terms. Shortfalls were experienced particularly in non-oil revenues due to administrative deficiencies and wide use of tax exemptions. Inflation is also an area of concern, tripling from 5.6% (2005) to 15.7% in 12 months. However, in early 2007 inflation dropped by 8-9% and maintained a rate of 7.2%, largely due to a sharp drop in food prices.

Oil industry

In 2006, 90% of Sudanese export revenue was generated through oil exports. However, oil production was below target for 2006, with production at 364,000 barrels per day (bpd) well below the projected 492,000 bpd. Proven oil reserves are estimated at 1.6 billion barrels, but the original and most reliable

in 2006, 90% of sudanese export revenue was generated through oil exports

oil fields, which produce valuable low-sulfur crude, are maturing. Much of the new oil fields are of inferior quality, being highly acidic and difficult to process. Nonetheless, the new inferior oil, the Dar blend, is finding higher acceptance in international markets and substantially increased in price throughout 2007. Sudan’s refiners in Khartoum, which processes the higher quality Nile blend crude, and Port Sudan giving a total combined capacity of 121,700 bpd, since January 2007. In 2005 Petronas was given a contract to build a new refinery, with the Ministry of Energy and Mining, at Port Sudan, to process the Dar blend crude, the refinery is planned to have a capacity of 100,000 bdp and open in 2009. The state’s oil company is Sudan Petroleum (Sudapet).

Four major foreign companies have to come to dominate Sudan’s oil industry:

n China National Petroleum Corporation (CNPC), state owned

n China Chemical and Petroleum Corporation (Sinopec Corp), private

n Petroliam Nasional Berhad (Petronas), state-owned (Malaysia)

n Oil and Natural Gas Corporation of India-Videsh (OVL), state-owned (India)

The three major consortia are:

n The Greater Nile Petroleum Operating Company (GNPOC), the main oil producing consortium in Sudan and 40% owned by CNPC

n The Petrodar Operating Company Ltd. (PDOC), owned by CNPC (41%), Petronas (40%), Sudapet (8%), Sinopec (6%), Al-Thani (UAE, 5%)

The White Nile Petroleum Operating Company Ltd (WNPOC), a joint venture of Sudapet and Petronas

Many of the big Western oil companies are being scared away by the prospect of more sanctions and humanitarian disinvestment campaigns over Darfur. In 2003, the Canadian firm Talisman was forced out by pressure from campaigners and in 2006 a Swiss firm, Cliveden Group, was also pushed out of Sudan citing similar reasons.

The majority of the oil lies in the south of Sudan, a semi-autonomous region with 6 million residents. A conflict between the southern residents and the northern governments had seen fighting on and off since the country’s independence in 1956. The 2005 Comprehensive Peace Agreement (CPA) entitled the South to half of all oil revenues but oil sharing agreements remain unresolved. On 11 October 2007, ministers of the Sudan People’s Liberation Movement (SPLM) refused to participate in the national unity government, claiming that the ruling National Congress Party (NCP) is failing to cooperate with them or implement the agreed peace agreement. The problem is exasperated due to the ongoing conflict over the boundary between the North and South, the region where much of the oil lies. The CPA stipulates that in 2011 there will be a referendum in the South on independence, and at this point it is expected that the vast majority of southerners will overwhelmingly vote to break away from the North. This situation holds the potential for a flaring-up of tension between the two sides, which could have a negative impact on oil production in the disputed areas and, subsequently, on the economy as a whole.

Energy

Sudan’s energy consumption is dominated by oil, around 10% of other energy needs come from hydroelectric power. Sudan consumes 94,000 bpd in oil and uses 3.6 billion kilowatt hours. Sudan’s energy infrastructure is poor and only 30% of the country has access to electricity. However, the government is rapidly expanding this infrastructure, partly because of obligations under the CPA. The most important project is the Merowe Dam, about 350 km north of Khartoum. The largest hydroelectric power project in Africa, it will cost $1.8 billion, create a lake 174 km long and help the government increase the electrification level from the current 30% up to the target of 90%.

Finance

In 1970 the Sudanese government decreed the Nationalization of Banks Act, which put the five commercial banks (Bank of Khartoum, Al-Nilein Bank, Sudan Commercial Bank, the Peoples Cooperative Bank and the Unity Bank) under the control of the Bank of Sudan, giving it the role of a central bank and the power to manage external and internal debt, manage monetary policy, to be the “bank of all banks” keeping their reserves in safe custody, to be the lender of last resort and to be the clearing house.

the latest round of sanctions implemented by the us in may 2007 has had a strong negative impact

In 1974, to attract foreign investment, foreign banks were urged to establish joint ventures, in association with Sudanese capital. This “open door” policy of 1974 allowed Saudi Arabia to invest large sums of petro-dollars in Sudan. In 1977 the Faisal Islamic Bank was established, becoming the first Sharia-based bank in Sudan. It was granted several privileges denied to other commercial banks (full tax exemption on assets, profits, wages and pensions). The banking system was Islamized in 1984, prohibiting the charging interest. Instead of interest, Islamic banks use other finance tools, like musharakah (partnerships for production), mudharabah (silent partnerships when one party provides the capital, the other the labor), and murabbahah (deferred payment on purchases). Government and Central Bank musharaka certificates dominate the Sudanese financial sector. The market for Islamic instruments and government securities remains shallow and an organized international Islamic financial market is not yet fully developed. The government of Southern Sudan has refused to authorize the Islamic banking system in the South or a mixed system, and has stated that it will only operate a conventional banking system.

There are 29 banks operating in Sudan, falling into three different categories: state-owned, joint ownership and foreign banks.

The main state-owned commercial banks are Al-Nilein Industrial Development Bank (NIBD), specializing in promoting industrial development while also providing multi-faceted and full-fledged banking services to all other sectors, Omdurman National Bank, mainly providing banking services for both retail and corporate clients, and Islamic Cooperative Development Bank of Sudan, providing two main facilities: agricultural financing (development) and commercial banking.

The most significant joint-ownership banks are Al-Baraka Bank (Arab and Sudanese investors), Blue Nile Mashreq Bank (merger between the Sudanese Blue Nile Bank and a Mashreq Bank in 2003), Faisal Islamic Bank (principal patron is Saudi Prince Muhammad Bin Faisal al-Saud), and National Bank of Sudan, in which the Lebanese Bank Audi bought a 75% stake in 2006 and which in the near future will change its name to Bank Audi – al-Ahli.

Foreign banks in Sudan include Byblos Bank Africa (the first foreign bank in Sudan), National Bank of Abu Dhabi, Mashriq Bank (the largest private bank in the UAE), Habib Bank (leader in Pakistan’s services industry), and the Emirates and Sudan Bank.

Citibank also used to operate in Sudan, however, following tough US sanctions it was forced to withdraw. European banks, also because of US sanctions, avoid providing financial services to companies that accept contracts for work in Sudan. The latest round of sanctions implemented by the US in May 2007 has had a strong negative impact on Sudan’s banks. They are suffering from the fact that, due to large amounts of US regulations on dollar transactions by Sudanese banks, some Arab banks have been refusing to conduct any dollar transactions with Sudan. This has led the Central Bank to announce that they will convert all dollar reserves into euro, British pound and other currencies by the end of 2007. A number of new measures have also been introduced to strengthen the banking sector in the face of these sanctions. The most important of them is the tightening of capital-adequacy ratios and the establishment of new paid-in capital minimum requirements.

Sudan’s banking sector remains weak in both relative and absolute terms. The ratio of assets to GDP stood at 28.4% in 2006, against MENA averages of 93.3% and 81.8% for emerging markets. The 29 banks that operate in Sudan are scattered over 522 branches which represent a ratio of 69,383 residents per branch. The banking sector has ample room to expand.

Real Estate and construction

There is a shortage of residential villas and apartments targeted at the high-end investor and user sub-markets. The housing needs of expatriate staff, mainly UN workers, have increased the demand for housing at the high end of the market. This has caused rents to increase rapidly. A two-bed apartment in central Khartoum that rented for $250 per month in 1999 now rents at around $1,750. Over the next 24 months, 95% of villas and apartments that are expected to be delivered will be aimed at the higher income segments. This does not reflect the income distribution spreads in the city and therefore a gap will continue to exist in the middle income segment of the market.

Currently, Sudan’s construction sector contributed just 4% of GDP in 2006. Today, Khartoum has the largest construction site in Africa with a $4 billion development is built across 1500 acres in Al-Sunut. On the construction industry side, however, Sudan imports 90% of its domestic cement needs, as its own cement factories have low capacities and weak technology.

a two-bedroom apartment in central khartoum that rented for $250 in 1999 now rents for $1,750

Transport infrastructure

Sudan’s road network is inadequate, although large stretches of roads are being built or overhauled. The new roads under construction are mainly around Khartoum and connecting the various oil fields. A main road between the North and South is also being built as part of the peace agreement. Another road will link Sudan with Egypt, obviating the necessity to ship all goods via Lake Nasser and promising an upsurge in traffic. The total road system in Sudan consists of 20-25,000 km, of which 3-5,000 km are asphalt all-weather roads. The railway system is also in poor condition and huge investment is needed in new signaling systems, the addition of double tracks to boost capacity and increase speed. In February 2007, the government announced an ambitious rehabilitation program for Sudan’s railways, signing a $1.7 billion contract with China to upgrade the 762 km line from Khartoum to Port Sudan to a double track. China is also delivering new locomotives and rolling stock.

Port Sudan is the country’s major commercial port. Just south of it, a new port has been constructed at Bashayer, to handle oil exports. The tanker terminal at Beshayer has a capacity of about 2 million barrels and in 2004 handled exports of 230,000 bpd. A second terminal is soon to be completed and is expected to handle around 330,000 bpd of exports.

River steamers serve all towns on the Nile and river cargo has increased by 8.2% to 79,000 tons and transported 25,000 passengers, a 31% year-on-year increase, in 2006. It is hoped that the CPA will enable a resumption of long distance boat transport on the Nile and the completion of the Jonglei Canal, which would significantly cut transport time between the South and Khartoum.

There are 15 sizeable airports of which Khartoum, Port Sudan, El Obeid, El Fasher and Juba airports are the most important. Due to a large increase in foreign airlines serving Khartoum, the government announced plans for the construction of Khartoum New International Airpot (KINA) at the cost of $500 million, scheduled to open in the beginning of 2011. The government of southern Sudan has announced that it will build two new international airports and will also upgrade the current one in Juba.

Communication infrastructure

The telecommunications sector in Sudan is now privatized and liberalized. This sector is seen as one of the main success stories of Sudan and has attracted large amounts of foreign investors as the market is seen as untapped.

In 2004 Sudatel relinquished its monopoly of the telecommunication network in Sudan, when a second license was awarded to Canar for $80 million. Until the end of 2005 Sudatel was 100% state-owned but was then floated on the Khartoum stock exchange. With the privatization of the fixed line network subscription doubled and reached 2 million users in 2006. However, with the privatization of the fixed line network Sudatel’s subscriptions dropped dramatically, by 2006 holding only 0.3 million fixed line subscriptions, with Canar dominating the market.

The cellular network in Sudan is growing at a rapid pace. In 1997 Mobitel, owned by Sudatel, was founded and held a monopoly over the mobile sector. In 1999 Mobitel had just 8,000 subscribers but by the end of 2005 this figure reached 1.5 million. The next year, 2006, saw Mobitel’s acquisition by Kuwaiti MTC for an estimated $1.3 billion. The two other mobile operators are MTN-Sudan, which ended the monopoly of Mobitel in 2005 and was formally called Areeba Sudan before it was bought by South African company MTN, and Sudani, part of Sudatel, which started operations in late 2005. By the end of 2006, Sudan had an estimated 4.7 million mobile phone users but market penetration is still only half that of average penetration across Africa. It is predicted that by the end of 2007 market penetration will be 25%.

The government of southern Sudan is opening up its own independent telecommunications regime that is separate from that of the central government. There are reports that Canar wants to start a mobile network but this has been met with opposition from Mobitel owners MTC (Zain). The southern government has opened bidding for mobile companies in September this year to build an $8-10 million cellular gateway in the South. Sudan is seen as a vastly underexploited country in terms of fixed-line, mobile and internet use, with a lot of potential for growth.

Internet penetration in Sudan is 7.6%, with estimated 2.8 million users in 2007. Sudanet was the first internet service provider in 1996 but Canar ended Sudanet’s monopoly in December 2006. ADSL broadband services were introduced in 2004.

Agriculture and Industry

Before the oil age, agriculture represented Sudan’s main sector and foreign currency generator. Until the late 1990s, agriculture represented almost 90% of Sudanese exports. In 2006, the agricultural sector still accounted for 40% of GDP and remains the major employer in the country, accounting for roughly 80% of the workforce. Like the overall economy, it recorded a historical high growth rate in 2006, of 8.3%. The main agriculture exports are cotton, ground nuts, gum arabic, sugarcane, sesame and meat products. All of these crops, except gum arabic and cotton, saw an increase in 2006 as land productivity increased.

Sudan’s non-oil industrial sector has recently enjoyed strong growth as manufacturing has started to recover from the stagnation of the 1990s. Sudan’s manufacturing sector grew by 7% in 2006 and accounted for 7% of GDP. The most successful industries have been in food processing, notably sugar refining. The government has also made plans to expand the textile industry.

Tourism

While Sudan can boast famous archeological sites (Meroë Pyramids), world-class coral reefs, and safari-worthy wildlife, during the past decades the political situation has prevented the development of a serious tourist industry. In 2006, the tourism sector generated $2 million, which is a dramatic increase over previous years but still only marginal in terms of contribution to GDP. The government aims to increase tourist numbers, especially on the Red Sea. Several tourist villages are being built, the one near Suakin costing $2 million and aiming to provide visitors with all expected facilities. The establishment of a nature park on the Red Sea coast has also been announced.

Currently, Sudan has only two hotels that meet international standards, both located in Khartoum. The Libyan-financed Al-Fatih hotel, part of the Al-Sunut project, is slated to open in 2008. The hotel sector is booming, with other projects underway, and occupancy rates of high-end hotels are over 70%. The increase in business travel has been felt particularly in the South and to cater for this new demand Kuwaiti investors are planning the construction of a five-star hotel in Juba. But the overall infrastructure is, as of now, inadequate.

Outlook 2008

Provided the CPA holds and frictions between North and South can be minimized, Sudan can expect to see continued strong economic performance, regardless of the situation in Darfur. This latter issue, however, will continue to curb Sudan’s international position and further sanctions by the US and Europe are possible. Income from oil remains the principal engine for growth in Sudan, but prices will be reduced due to an expected drop in international oil prices and because of the lower quality of oil in the newer oil fields. GDP is expected to be strong for 2008 at 8% but large commitments under the CPA for regional development mean that the government consumption is expected to rise. Inflation and managing the budget deficit are expected to continue to be the major obstacles for the Sudanese economy.