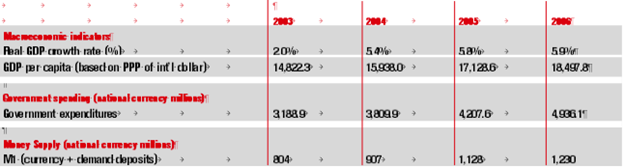

Egypt is riding high. Economic growth in the last fiscal year that ended on June 30 reached 7.1%, the highest level in more than two decades. This pace has prompted Finance Minister Youssef Boutros-Ghali to inform International Monetary Fund officials in October that Egypt could reach a growth rate of as much as 9% in a year, according to a finance ministry statement.

The International Finance Corp, the World Bank’s financing arm, set the record straight and declared Egypt the world’s top reformer this year, eliciting cheers from the Egyptian authorities who faulted the IFC’s last year assessment of the North African country’s business climate. As a top reformer, Egypt cut the minimum time required to start a business, lowered fees for registering property and relaxed bureaucracy for construction permits among other measures, according to IFC’s 2008 Doing Business report released in October. The report, the fifth in a row, details regulations that affect business activity among 178 economies.

Outlook is excellent

“The outlook for growth in Egypt for the next two years is excellent,” Matthew Vogel, the London-based head of Head of Emerging Europe, Middle East and Africa Strategy at Barclays Capital told Executive. “The government has done a tremendous job in privatization and reform.”

According to the World Investment Report released by the United Nations Conference on Trade and Development, Egypt emerged as the number one recipient of foreign direct investment in Africa, beating South Africa (last year’s top recipient) by attracting as much as $10 billion in 2006, compared with $5.4 billion a year earlier. Egypt, which jumped 35 places among countries ranked in the report, attracted 80% of the investment to expansion and new projects in the non-oil industry, the report said.

The government, undaunted by allegations of selling state assets to colonizers, announced its intention to sell as much as 80% of the country’s third largest state lender, Banque du Caire, to a strategic investor, in a step seen as a rebuff to detractors who had criticized the slowing pace of the government’s privatization program. Privatization proceeds also increased to $2.8 billion in the last fiscal year that ended June 30 from $906 million a year earlier, Central Bank figures show. However, the pace of privatization is not expected to remain the same over the next few years.

“The government has privatized the blue chips,” said Reem Mansour, a Cairo-based economist with HC Securities & Investment, an Egyptian investment company. “What’s left may not be very as attractive to investors as the assets sold before and the government may not find it easy to sell the remaining assets.”

Besides these reforms, the Arab World’s most populous state continued to benefit from the influx of Gulf oil money generated from prices that are inching closer to $100 a barrel in New York. The Cairo & Alexandria Stock Exchanges (CASE), the nation’s bourse, has benefited from the oil boon as the benchmark CASE Index broke a new record in November. The CASE Index’s stellar performance has prompted the Egyptian government to set-up in October a new exchange for small and medium sized companies, called NILEX, the first such market in the Middle East and North Africa region.

The country’s balance of payment recorded a surplus of $5.3 billion in the last financial year ended June 30, compared with a surplus of $3.3 billion a year earlier. The Central Bank of Egypt attributed the increase in surplus to a rise in the services account and transfers. Total Egyptian trade exports grew by 19.3% to $22 billion in the last fiscal year from $18.5 billion a year earlier, widening the trade deficit to $15.8 billion. Exports have increased despite the appreciation of the pound.

Foreign investment doubled

“The country’s increasing trade orientation to Europe has been very encouraging, which has allowed the government to allow currency appreciation against the dollar to fight inflation without any major negative impact on export performance,” said Vogel.

Meanwhile imports rose 24.3% to $37.8 billion in the last fiscal year from $30.4 billion a year earlier, according to the Central Bank. Tourism revenue rose as much as 10.7% to $8 billion in the same financial year. Foreign direct investment almost doubled to $11.1 billion in the last financial year from $6.1 billion a year earlier, with significant growth in investments directed to new businesses.

“We think investment will continue to grow, but investment growth at these levels is not realistic,” Simon Kitchen, a Cairo-based economist with Egyptian investment bank EFG-Hermes Holding, told Executive. “There are constraints such as high land and cement prices.”

Yet the economic bonanza taking place in Egypt is tainted. Some low-income Egyptians are not feeling the fruits of the economic overdrive, analysts and politicians say. Egypt, blessed with the world’s longest river, suffered this year from the disgrace of being unable to provide clean water to its rural citizens, amid protests about the level of government services. Strikes, mainly at state-run textile companies, marred the economic success of privatization and revealed a level of revolt among public state employees unseen and unfamiliar to the much-controlled socialist state. The crackdown on labor unions has riled human rights activists, including Human Rights Watch, which criticized the Egyptian government’s closure of two labor groups in a report in April. The Muslim Brotherhood, the country’s largest opposition group in parliament, is leading the political and economic rally to hold the government accountable.

“The government policies do not take into account the social needs of the Egyptian people, because of the widening gap between the rich strata of society which consists of businessmen allied with the state and the poor strata representing the majority of the population,” Mohammed Habib, first deputy of the Muslim Brotherhood told Executive.

the government policies do not take into

account the social needs of the egyptian people

Undoing socialism in Egypt has come with a heavy price. Inflation has rocketed to 8.8% in September from a year earlier, a level not seen since it peaked this year at 13% in March, as a result of an increase in domestic food prices such as maize, edible oil and wheat — staples of Egyptian diet — according to the Central Bank of Egypt. The bank, which nonetheless has left interest rates unchanged at its last meeting in November, said “higher economic growth” is expected to push inflation “above the upper level of the CBE’s (Central Bank of Egypt’s) comfort zone.” Usually government and central bank officials have defined their target inflation rate to range between 6 and 8%.

“Inflation is going to be an on-going problem for these levels of growth,” said Kitchen. “Growth will be between 6 and 7% for the next five to 10 years, which is quite a transformation of the Egyptian economy.”

The rise in inflation and strikes at state-owned enterprises has prompted some politicians to call on the government to halt its sale of state assets, which is seen by some lawmakers as allowing “colonizers” to return to the country, which kicked out foreign businesses during the socialist era of former President Jamal Abdul Nasser.

“I do not think there is substantial pressure on the government to slow the pace of privatization,” said Vogel. “The challenges for the government lie more in the areas of civil service reform and subsidies. Privatization and FDI (foreign direct investment) inflows are leading to job creation, not job destruction.”

Opposition focuses on unemployment

Government officials and ministers have cautioned that the trickle-down effect of economic growth will take time to reach the low-income bracket. Prime Minister Ahmed Nazif has said he is willing to sacrifice a rise in inflation in order to maintain growth and create jobs, which was one of the tenets of President Hosni Mubarak’s re-election program in 2005. Pro-government and opposition members of parliament have rallied to underline the lingering problems in Egypt, starting with meeting the needs of low-income earners to lowering the unemployment rate. The state says the rate has fallen to 9.1% in June 2007 from 9.5% in June 2006. However, independent organizations had in the past doubted the official levels of unemployment.

“The government is likely to refocus on social infrastructure more to further strengthen the country’s productivity and ensure that poorer members of society share in the benefits of higher economic growth,” said Vogel. The government has attempted to meet the needs of the low-income earners. In a bid to halt the spike in inflation and spare the poor extra expenses, the government has said that fuel subsidies would be restructured to suit the needs of the most-deprived Egyptians.

In a bid to attract investors and lower inflation, the government also lowered average tariffs to 6.8% this year from about 9%, after lowering them from 14.6% in 2004. The government is also seeking to lower property taxes and introduce value-added tax.

Boutros-Ghali has emphasized that the government intends to increase spending, but at a controlled pace, to meet the needs of Egyptians over the next few years. In addition to these measures, the government is intent on implementing an ambitious economic program that includes slimming the fiscal deficit and thus the public debt through higher income from taxes and other resources and economic growth exceeding 7%.

“With growth helping so much with public sector finances, some of the more pressing and difficult issues, such as civil service reform, may be postponed,” said Vogel. “This poses some risks to confidence should growth slow.”

Lowering the deficit

Boutros-Ghali has pledged to lower the fiscal deficit from 7.5% of GDP in June to about 3 to 4% of GDP by 2011 through higher growth, greater tax revenue, stable growth in expenditure as a percentage of GDP and other fiscal measures. The government managed to lower its fiscal deficit last year by lowering fuel subsidies, a move that sparked a rise in inflation, and higher proceeds from privatization. The government, though, has postponed another fuel price hike for now to tame the rise in inflation.

“The first moves they did on lowering fuel subsidies were encouraging,” said Vogel. “Since fiscal revenues have been performing so well, the public sector deficit is falling as programmed. However, they may be encouraged to move slower on the pace of future cuts in subsidies.”

A lower fiscal deficit and higher growth would help stem the rise in the country’s total domestic debt, which stood at 637.2 billion pounds or about 87% of GDP at the end of June, compared with 593.5 billion pounds or 96% of GDP in June 2006. The public debt has irked Egypt, which has had bad history with its borrowing needs, which spiralled out of control in the 1980’s and 1990’s. Owing to its strong ties with the US and other Western power, Egypt managed in the 1990’s and under the supervision of the International Monetary Fund to cut its debt. Its participation and support to the US-led war on Iraq in 1990-1991 helped Egypt secure debt rescheduling agreements and write-offs from various countries.

Uncertainty remains

However, lowering the fiscal deficit and thus cutting the debt has its own set of problems. Further cuts in the fiscal deficit involve removing subsidies on fuel and food, and slashing the bloated public wage bill, two politically unpopular moves.

“The government is relying on other sources of revenue such as sale of land and privatization proceeds to lower the fiscal deficit, but these are unsustainable,” said Mansour. “They have to look at decreasing expenditure. They can’t cut the wage bill because that will cause political upheaval and they can’t say they will lower food subsidies because that is also threatening.”

The issue of lowering the fiscal deficit and maintaining political stability, mainly succession of power, is affecting the country’s rating, according to credit rating agency Standard & Poor’s. President Hosni Mubarak has ruled Egypt since 1981 on his own, without a vice-president. He has yet to nominate a possible successor to power.

“Since our revision of the outlook to stable from negative in March 2005, we have not raised the ratings on Egypt,” Standard & Poor’s said in a report released in November. “They continue to be constrained in the ‘BB’ category by the country’s fiscal inflexibility, and by uncertainty surrounding presidential succession.”