Syria chalked up numerous successes in 2007. Politically, the country ended its international isolation. On the domestic front, the government continued — however cautiously — to open the economy. The country’s private banking and insurance sectors both posted healthy gains, bricks and mortar finally began to be put in place on a number of high profile real estate developments, the country’s first private university graduates hit the job market and the first Syrian produced car rolled off the production line, a joint Syrian-Iranian venture.

The coming year, however, presents greater challenges on the economic front. Over 2007, Syrians learned they had become net oil importers, exploding the budget deficit. Throughout 2008, debate over the need to reduce fuel subsidies and reform a bloated public sector is set to pitch a new wave of Syrian economic reformers against old guard Baathists in ever more heated argument. Tough decision regarding the economic direction of the country will become increasingly difficult for President Bashar al-Assad to postpone.

One door opens, another closes

Any debate about the strength of Bashar al-Assad’s position was laid to rest in 2007. Ongoing violence in Iraq and political unrest in Lebanon saw stability and security emerge as major themes of the young president’s referendum campaign; a presidential poll in which he secured 97.6% of the vote.

The deep freeze on diplomatic contact with Syria began to thaw over 2007. The need for Syrian involvement in producing solutions to conflicts in Iraq, Lebanon and Palestine was grudgingly admitted to by US officials. The first major diplomatic breakthrough came in March when EU foreign policy chief Javier Solana broke a two-year freeze on high level EU contacts and visited Damascus, pledging to help Syria regain the Golan Heights in the process. US House Speaker Nancy Pelosi lead a congressional delegation to Syria one month later (and went shopping for pearls in Souq Hamidiyya), spurring talk that American sanctions against Damascus may be lifted. The major breakthrough came in May when US Secretary of State Condoleezza Rice met with her Syrian counterpart Walid Mu’allem on the sidelines of a conference about Iraq. Damascus ends the year having forced the 40-year-old occupation of the Golan Heights onto the agenda of the recent Annapolis peace conference.

Not that it was all smooth sailing. While 2007 may have seen the resumption of diplomatic activities with Western nations, Syria’s relationship with her Arab neighbors became increasingly strained. The usual stage-managed facade of Arab brotherhood has been torn away in the past few months and sharp disagreements regarding Lebanon, Iraq, Palestine and Damascus’ tightening embrace of Tehran spewed into the public arena. The most sensational allegations arose in August when Saudi ambassador to Lebanon, Abdel Aziz Khoja left the country because, according the Kingdom, he had received death threats from Syrian proxies in Lebanon. The Saudi daily Okaz went on to damn Syria’s relationship with Iran, calling Damascus “a dagger thrust by this regional element into the Arab nation.”

Border conflict between Turkey and the Kurds, growing division in Palestine, the threat of American strikes on Iran, instability in Lebanon and the continuing investigation into the killing of former Lebanese Prime Minister Rafik Hariri all require careful navigation by Syria in 2008. In all, however, Damascus can look to the new year with increased confidence, secure in the knowledge that the international community has all but decided that ignoring Syria benefits no one and that the most hostile US administration on record will soon be forced out of the White House.

Making the most of any opportunity

Syria’s private sector continued to show, when given the chance, it will defy expectations. The country’s newly opened insurance sector grew by 25% over the year, with premiums totalling $85 million in the first six months. Fifteen firms now operate in the newly opened market. The state-controlled Syrian Insurance Company continued to take a beating; its market share fell by around 40% over the year.

The private banking sector also consolidated its market share over 2007 and now accounts for around 40% of all private sector credits. In April, Byblos Bank Syria became the first Syrian bank to issue MasterCard prepaid, debit and credit cards.

syria’s private sector continued to show, when given the chance, it would defy expectations

Syria’s Islamic financial services sector also took its first baby steps — steps that are likely to become gigantic bounds in the coming years. The country’s first Islamic bank opened in late August, registering 10,000 new accounts in the first two months of operations, a period that included the Ramadan holiday season. The Syrian International Islamic Bank followed shortly after, launching the largest investment drive in Syria’s history by offering $51 million in shares to the public and taking $20 million in deposits in its first month of operation. The country’s first Islamic insurance firms are expected to open throughout 2008, with industry stakeholders predicting the sharia-compliant companies will snare up to 25% of the market.

Syrian policy makers continued to roll out their program of economic reform. Presidential Decree No. 7 and No. 8 revamped the backbone of the country’s investment regulatory regime, allowing foreigners to own land, repatriate profits and avoid customs tax on the imports of assets and equipment related to projects. It also ended several tax incentives for foreign investors, however the government simultaneously moved to reduce taxation rates on companies and private investors. The ceiling on foreign ownership of banks and real estate was also lifted in a bid to boost FDI.

Speaking at an investment conference in Damascus in late November, Syrian Investment Agency head Mustafa al-Kafri said $8 billion in new projects were licensed under the new investment regime in 2007, a slight decrease from the record $9.2 billion approved in 2006. Like all figures in Syria, the county’s FDI numbers need to be taken with a large grain of salt. Approved is one thing, implemented is another. The agency recently revealed around 60% of approved projects are yet to be started.

Syria’s Central Bank disengaged the Syrian Pound from the dollar in July. The pound is now linked to a basket of currencies which includes the dollar at 44%, euro at 34% and the yen and sterling pound at 11% each. Foreign exchange bureaus were given the green light to set up shop and traders gained permission to purchase all their foreign exchange requirements for imports from the private sector.

On the trade front, the long anticipated Syrian-Turkish free trade agreement came into affect in January, with both countries looking to boost trade from $1.3 billion this year to more than $5 billion over the next five years.

Budget deficit greatest challenge

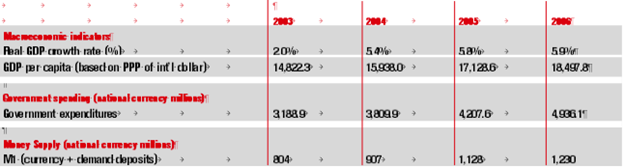

The country’s mounting budget deficit looms as the greatest challenge in 2008. Aggregated by declining oil production, estimated to be falling by 11% per annum, the deficit presently weighs in at $4 billion. Syria’s oil balance has moved from a surplus of $2.4 billion in 2003 to an estimated deficit of $1.3 billion this year.

Increasing taxation has been identified as one possible solution to the fiscal crisis. “The government has said it will deal with the fiscal deficit by increasing taxation, augmenting the existing tax revenues and rolling out a second generation of tax reform,” Ernst & Young Syria head Abdul Kader Husrieh said. Past attempts at increasing tax compliance, however, have only been mildly successful. The 2006 budget anticipated tax receipts to total $3.2 billion; the state collected $1.57 billion. At the same time, tax reform by itself is nowhere near enough. “Even if all this goes ahead, the government does not expect to collect more than $196 million which is less than 5% of the budget deficit,” Husrieh said.

At the heart of the matter are the politically unpalatable choices of ending the government’s long held subsidies regime and public sector reform. Moves to cut into both have provoked much heated debate among Syrians.

The beginning of the end?

Subsidies are projected to cost the government around $7 billion over 2008, around 20% of the country’s GDP. Fuel subsidies alone, according to the IMF, cost the Syrian government around $15 million per day. The price of gasoline jumped by 20% last month, however, Syria is most reliant on diesel for transport, agriculture and heating needs. Due to decades of poor planning, the country has limited refinery capacity. As of 2006, Syria has been forced to import diesel at the international price of just under 60 cents, but sells it domestically for 13.7 cents per litre.

“I don’t think we are going to see anything other than cosmetic reform”

A government plan to end fuel subsidies is meant to take effect from January 1. If it goes ahead, the immediate impact will be to see fuel prices almost double, with a litre of fuel oil rising from 14 cents to 24 cents and a tank a gas increasing from $2.90 to $5 (the price of petrol has still yet to be released). The price of industrial fuel oil was increased in 2004 and would rise by a further 25% to just under $150 per ton. The government has proposed to compensate some 3.5 million families, identified as being in lower income brackets, through the provision of a $235 annual cash payment.

“the government has said it will deal with the fiscal deficit by increasing taxation”

Implementation of the plan is being viewed as a major test for Syria’s economic reform guru Abdullah al-Dardari and an indication of his pull with Assad, who must choose between his economic reform team and the old power elite.

Public sector reform

Public sector reform has long been identified as an urgent need. Syria’s business environment remains strangled by red tape and the president again identified the need to fight corruption as a government priority during his swearing in address before parliament. Deeds, however, are not following words. More disturbingly, a number of indicators suggest the situation is getting worse, not better. The recently released World Bank’s Doing Business 2008 ranked Syria 137 out of 178 countries in terms of ease of doing business, chalking up worse results in 8 of the 10 indicators used to formulate the overall ranking compared to the previous year. Neighbors Turkey ranked 57, Jordan 80 and Lebanon 85. Syria ranked 13 out of the 17 Arab countries listed – only two war-torn countries (Iraq and Sudan) as well as Mauritania and Djibouti fared worse.

The perception of corruption is also disturbingly high. The Corruption Perception Index by Transparency International ranked Syria as the second worse country in the Middle East in terms of perceived corruption, only less corrupt than war-torn Iraq. More worrying is the sharp fall in Syria’s world ranking, from 70 two years ago to 138 last year.

All of which detracts from the investment attractiveness of the country and Syria continues to lag behind her neighbors in terms of FDI. “What these reports show is that attractiveness to private investment is not only a consequence of better economic regulations,” a report by the Syria Report stated. “It has to do, as much, with lowering bureaucratic obstacles and corruption, with the availability of a truly independent judiciary, and last but not least with serious efforts at accountability. Further economic reforms, although necessary, will not be sufficient. The Syrian authorities will have to look at other reforms, not only economic ones.”

No easy way ahead

In many ways 2008 looms as a watershed year for Syria; one which will decide if the country will deliberately move towards full economic liberalization, or be dragged kicking and screaming into a social market economy only after it has exhausted all other economic alternatives. The easy reforms have been taken. With most watchers predicting a slight downturn in the economy this year — The Economist Intelligence Unit expects real GDP growth of 3.3% for 2008-2009 — the room Dardari is given to implement unpopular solutions to stop the haemorrhaging of public coffers will be a litmus test of Syria’s commitment an open economy. Most, however, are not expecting radical change. “On the most sensitive issues of reform, on the unpopular issues like raising the price of fuel and public sector reform to which there is a lot of opposition in the press, in the parliament and among ordinary Syrians, I don’t think we are going to see anything other than cosmetic reform,” said Nabil Sukar, managing director of the Syrian Consulting Bureau. “I think it will take another two years before the situation becomes urgent enough to warrant real change by the government.”