One look at 45-year-old Raji El

Mawla, regional manager of the

Maytag Group, and you would

probably think that life is pretty easy for this

businessman. He speaks with a calm voice

and rarely wears a suit and tie to work. But

first impressions can be deceiving.

It is 9am at Mawla’s office. He has a portable phone close to one ear and a cellular

in his hand. He is busy typing an

email to the corporate office in the US

while trying to resolve a misunderstanding

between an area manager and a distributor.

In the following hour, he manages to

schedule two or three field meetings,

respond to a few of his nearly 70 daily

emails and receive five urgent phone calls,

that he responds to in the same relaxed

manner. “Hello, what seems to be the problem

… I see … don’t worry … relax, I’m

on it as we speak … Your problem will be

solved by tonight … How’s the family?

Good … Keep up the good work, goodbye.”

After two minutes, the crisis is over.

“Easy and effective communication is

essential in this business,” says Mawla.

“People can reach me via email or cellular

24 hours a day.” Mawla must oversee the

work of four area managers based in

Lebanon, Saudi Arabia, Tunisia, and

Tehran. He is responsible for 65 distributorship

accounts in such countries as Saudi

Arabia, Jordan, the UAE, Kuwait,

Pakistan, Egypt, Tunisia, Morocco,

Senegal, and the Ivory Coast. Because of the

overlapping days and hours of operation in

the countries under his command, Mawla

works a seven-day week. With Maytag’s

corporate office in the US eight hours behind local time,

he usually does not get home until late at night.

Mawla is truly sleepless in Lebanon, but has

it paid off? The answer can be found in his

office. Sitting on a shelf is a red Everlast

boxing glove, awarded to him for reaching his

mid-year quota. Next to it are six certificates

given to him by the Iowa home office for

exceeding his quota each year since 1993.

Five years ago, when Mawla introduced

Maytag to the Middle East, it was a little

known brand. Today, it leads the pack among

US imports, both locally and regionally.

Since his promotion from area manager to

regional manager in 1994, Mawla has doubled

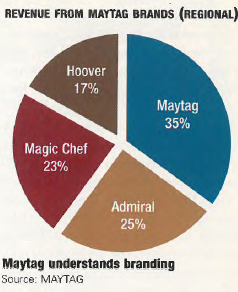

local sales of Maytag brands, which

include Maytag, Hoover, Magic Chef,

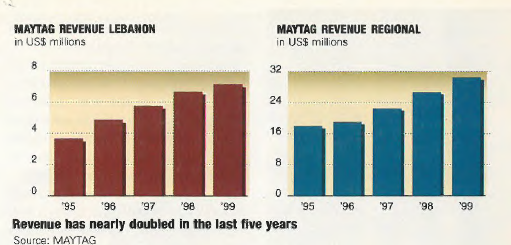

Admiral and Norge. Revenues have gone

from $3.5 million in 1995 to $7 million in

1999 and the company has carved out a

10% share of the local market for refrigerators,

which compose the bulk of

Maytag’s sales, which include washing

machines, floor cleaners and gas ranges.

His performance regionally has been equally

impressive, expanding revenues from

$18 million in 1995 up to $30 million in

1999. In relation to other US brands, local

market share of Maytag’s brands has grown

from 32% in 1997 to 61% in 1999, outpacing

GE, Frigidaire and Kelvinator. In Saudi

Arabia, Maytag has a 45% market share

against other US imports and in the UAE,

42% against US imports.

But what is most impressive is that Mawla

has managed to make these gains in a market

where imports of US refrigerators (the

bulk of the group’s sales) have been declining

rapidly. With the country in a recession,

people cannot afford to buy expensive US

manufactured refrigerators. As such, cheaper

Korean and locally produced refrigerators

have been slicing into the market share of the

US brands.

Statistics from the Ministry of Economy and

Trade indicate that imports of complete

American-made refrigerator units have

dropped from 36,000 units, $21 million, in 1998

down to 15,000 units, $15.7 million, in 1999 (see

“Chill in with the big boys,” February 2000).

This gives US refrigerators a 19% share of the

80,000-unit-per-year local market.

Meanwhile, Concord, a locally produced

brand which sells for at least half the price

of its US rivals, has boosted its output from

2,500 units in 1992 up to 30,000 units in

1999. Sales of popular Korean brands, such

as Samsung and LG, have also been strong.

“Until last year, GE was selling about 7,000

units per year. Last year, they started to

come down and we are taking their share.

Koreans as a whole have been coming in

strongly in the last five years,” says Antoine

Cherfane, president of AC Holdings, distributors

of Samsung refrigerators. The

Korean manufacturer has spent hundreds of

millions of dollars upgrading its manufacturing

facilities, building a state-of-the-art

robotics factory that is able to produce 2 million

units per year. The company sells some

7,500 units a year locally with sales volume

increasing at an annual rate of 25% over the

past three years, according to Cherfane.

Selim Antaki, chairman and CEO of LG

Lebanon, also reports a strong performance

for his company. With between

7,500 and 8,000 units being sold, Antaki

claims that LG refrigerators have carved out

a 10% market share. LG refrigerators are

equipped with patented new technology

called Door Cooling, a system that equalizes

airflow throughout the whole refrigerator.

“The Koreans are improving in their technology

while the Americans are sitting

idle, not really doing much,” says Gabriel

Traboulsi, general manager of Pharaon

Homeline, distributor of US-made brands

Magic Chef and Frigidaire, Taiwan’s

Sampo and France’s Brandt.

Antaki agrees: “American refrigerators

look like boxes with mechanical controls

and outdated technology that no longer

adapts to the consumer’s needs.”

But even as the demand for US refrigerators

declines, competitors admit that

Maytag remains a strong brand. “Among

other US imports, Maytag is the best

refrigerator,” says Antaki.

How did Maytag manage to do so well? A

quick look at the 17 years that Mawla has

been in this business and it is easy to understand

the secret of his company’s success.

From 1983 to 1989, he was an area manager

in Kuwait for Hoover. In 1989,

Maytag took over the Hoover operation

and the company’s two international divisions

were merged to form Maytag International.

After the Iraqi invasion, Mawla

was forced to transfer to London where he

became Maytag’s area manager for the

Gulf market, with the exception of Saudi

Arabia. In 1992, sensing an opportunity, he

brought the company to Lebanon.

Mawla’s direct management style has been

a key ingredient to turning Maytag products

into big sellers. Mawla visits all of the 65 distributors

under his control, checking on products,

quality of service, dealing with technical

problems and assisting his area managers

and distributors. “I do the product knowledge

training responsibly, and visit the service centers

randomly to make sure they are doing

their jobs properly,” says Mawla. The company

will soon have a locally based service

engineer stationed in Lebanon – for now, the

company relies on someone in London. The

engineer will visit the service centers of

wholesalers and Mawla, in turn, will check to

make sure the service engineer is doing his job

properly. He also conducts monthly and

quarterly meetings with his area managers

where he reviews market conditions, measures

the competition’s products and strategies,

evaluates achievements, reviews that year’s

plans and sets new goals.

The company also benefits from being able

to manufacture, under license, in a number of

regional countries, including Saudi Arabia,

Pakistan and soon Tunisia. This cuts the costs

by eliminating import tariffs. Mawla also

benefits from a strong product development

program. The Maytag Corporation, which

had sales in 1999 of $4.3 billion, has sunk

some $220 million into a new technology

called advanced product design (APD). The

system eliminates leaks and noise and makes

the Maytag refrigerator rust-proof. According

to US-based Consumer Reports magazine,

Maytag has been the number one preferred

refrigerator in the US for the last three years.

In February 1999, Consumer Reports ranked

Maytag’s 24-foot refrigerators first in terms

of energy cost, temperature performance,

noise and convenience.

Maytag also understands branding.

“Maytag spends heavily on advertising its

products,” says Traboulsi. Last year, the

company spent some $250,000 to host a creative

interactive TV show in Saudi Arabia, giving

away an equal $250,000 worth of Maytag

and Hoover products to winning contestants.

Locally, Maytag invests about $600,000 a year

in advertising, equal to the budget of

Concord and $100,000 more than the annual

budgets of AC Holdings and LG Lebanon.

But the main reason for Maytag’s success locally

has been its aggressive distribution network,

headed since 1995 by Nassif El Khechef,

chairman and general manager of Linkers

Group, distributor of the Maytag brand.

Khechef is also general manager of Herald

Trading Company, distributor of Hoover

since 1948, and chairman of Mangroup, distributor

of another Maytag brand called

Norge since 1998.

Khechef heads the distribution of three out

of the five Maytag brands. “Out of the 9,000

Maytag refrigerators that were brought into the

country in 1999, we imported 6,000, 75% of

sales,” says Khechef.

Linkers has a modern service and technical

center. It keeps a stock of spare parts for models

going back ten years. Khechef is responsible

for marketing brands locally in cooperation

with the suppliers. Linkers has a strong

relationship with Power Network, a high-impact

advertising and marketing company.

“I believe Maytag has the right partner by associating

itself with us and we made the right

choice by choosing them also. They have a

great product,” says Khechef. His company

also employs a well-trained sales force with

strong knowledge of the products they sell.

The group has an incentive policy for its distributors’

sales force. “The sales people are

greatly motivated. That was a smart move by

Maytag,” says Traboulsi.

Mawla knows. For a man who never rests,

motivation is his middle name. But he has his

priorities. “If you’re talking about choosing the

right partner, I have one at home. And as

long as I bring my children gifts from my trips,

they’re happy,” he says.