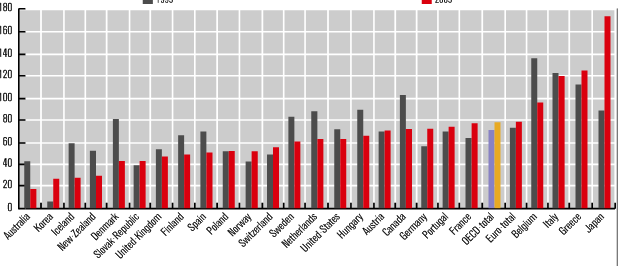

Government deficits are sensitive to the economic cycle as well as to government taxation and spending policies. For the OECD as a whole, deficits as a percentage of GDP reached a peak in 1993 but then fell steadily over the next six years and had turned into surpluses (net lending) at the peak of the economic cycle in 2000. Since then, deficits have been growing and the deficit to GDP ratio had become high in 2003 for most of the larger member countries including France, Germany, the United Kingdom, the United States and, especially, Japan. In 2004-2005 the deficit to GDP ratios were reduced in most countries with the exception of Hungary, Italy and Portugal.

In the run-up to monetary union, EU countries that expected to adopt the euro followed fiscal policies aimed at reducing government deficits. Deficit reduction policies were successfully implemented in several other countries, including New Zealand (since 1994), Australia (since 1997), Denmark (since 1998) and Sweden (since 1998). Korea is the only country which has recorded surpluses throughout the period, although Norway has had surpluses in most years since 1990.

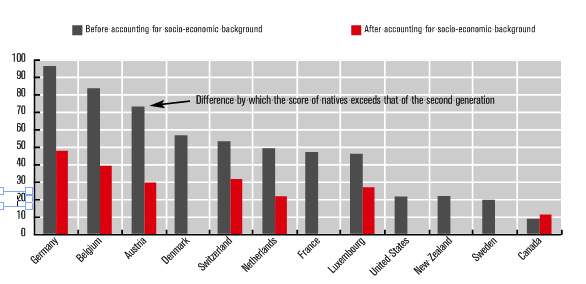

Gaps in the PISA score between native and second generation immigrant students in the OECD

Second generation immigrants now constitute a significant and growing share of students in many OECD countries and their integration is of increasing policy concern, particularly in Europe. In the OECD area as a whole, they tend to perform better than immigrant students, as one would expect since the former have been born in the country of assessment and were entirely educated in the host country. In most countries for which data are available, there are nevertheless significant gaps between natives and the second generation. This is particularly the case for Germany and Belgium, where the gaps in the raw scores for the second generation amount to the equivalent of about two years of schooling. Gaps are also large in Denmark, Switzerland, the Netherlands, Austria and France, but tend to be small or even insignificant in the traditional immigration countries. Adjusting for socio-economic background generally reduces the gaps by about half, but even then, second generation students often remain at a substantial disadvantage, particularly in Germany, Belgium, Switzerland, Denmark, the Netherlands and Austria.

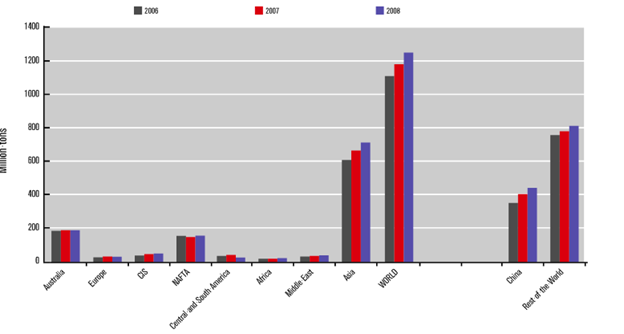

Outlook for Apparent Steel Demand 2007-2008

2006 was a particularly strong year for steel use with a growth of 8.5% for the world. The forecast is a growth of 5.9% in 2007 taking the total to 1,179 million tons, an increase of 65 million tons over 2006. No deceleration in growth is foreseen in 2008 with a further increase of 6.1% bringing the total for the year to 1,250 million tons.

The particularly strong positive trend is foreseen for both years in Africa, Asia and South America. Growth continues in Western Europe and after an inventory draw down in 2007 in North America a positive trend is forecast in 2008. China remains the largest single market and the strongest growth area. Steel use will increase by 13% in 2007 followed by another 10% in 2008, taking the total to 443 million tons — 35% of the world total.

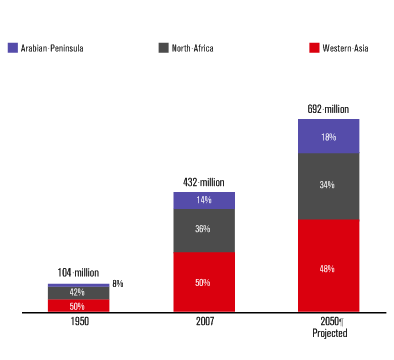

MENA Population: 1950, 2007, 2050

In 2007, the MENA region has about 432 million people, making it one of the least populous world regions. But rapid population growth rates — second only to sub-Saharan Africa — caused MENA’s population to quadruple since 1950, and will propel its total to 700 million by 2050, exceeding the population of Europe in that year. This continuing growth is complicating the region’s capacity to adapt to social change, economic strains, and sometimes wrenching political transformations.

While the region embraces religious and cultural tradition, there has been a veritable revolution on many fronts. Just a few decades ago, illiteracy rates were quite high for women in many MENA countries. Women often married before age 20, and they rarely worked outside the home. Now, women are attending school and beginning to enter the labor force. Couples are waiting longer to marry and are deciding to have fewer children. Child and maternal health have improved, leading to longer life expectancies and plummeting infant mortality rates in many countries.