The last few years haven’t been easy for local industry. And the Lebanese Ceramic Industries Co., which is owned by the Garghour Group and Finland’s Sanitec, is no exception. A local manufacturer of sanitary ware and tiles, Lecico saw its profits go down the toilet in 1998, when it registered a net loss of $1.4 million, and barely managed to break even last year. Not the direction anyone wants to see their business take after a net profit of $3.5 million in 1995.

Output in tiles has remained steady at 1 million m², but Lecico decreased production in sanitary ware, which includes toilets, sinks and bidets, from 730,000 pieces in 1995 in order to off-load excess stock. Last year it produced 490,000 pieces. At the same time exports dropped from a level of 50% to 55% of production in the 1980s to about 25%.

In Egypt, where Lecico also has manufacturing facilities, it’s a different story. There the company has been dealt a royal flush. Lecico Egypt dwarfs its Lebanese cousin; though the company would not release exact figures for each year, its Egypt operations have generated yearly net profits of between $8 million and $11 million since 1995. Its annual production of sanitary ware increased from about 2.2 million pieces to 3 million last year, with export markets soaking up 800,000 to 1.1 million. About half is destined for England, where the firm claims to have a 7% to 8% market share. Last year the group’s revenues totaled almost $90 million, while Lebanese operations accounted for just $17.8 million.

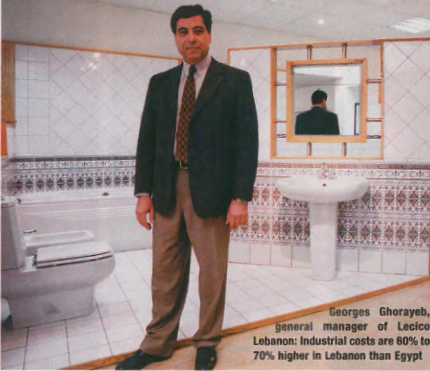

So why has the company taken a turn for the worse in Lebanon despite having a 58% market share and being the sole local manufacturer of sanitary ware, while its Egyptian operations remain strong? “Lecico has definitely been affected by the freeze in construction activity in Lebanon and the lack of opportunity to develop new export markets in the Middle East,” says Georges Ghorayeb, general manager of Lecico Lebanon and the group’s technical manager. While exports to the region shrank with the economic downturn in the Gulf, Syria and Iraq have remained closed and low-cost manufacturers have wreaked havoc on Lecico’s market share, explains Ghorayeb.

To add insult to injury, industrial costs in Lebanon are high. Ghorayeb should know, being the beneficiary of low-cost production at Lecico Egypt. “There is no comparison at all between the structure of cost in sanitary ware manufacturing in Egypt and Lebanon,” says Ghorayeb. He estimates that direct industrial costs are 60% to 70% higher for energy and labor in Lebanon than Egypt.

Faced with such a drain on profits, Lecico has begun implementing a strategy to boost its local operations and reap greater rewards in Egypt. Staff in Lebanon have been reduced from 670 at the start of 1997 to 500. Further reductions will come through attrition. Last year, Lecico invested close to $900,000 to upgrade the tile-making facilities in Kfarchima. That is expected to reduce costs by 18% to 20% on energy and labor. It also allowed the company to introduce floor tiles to the market this year, having previously been restricted to wall tiles. “That should help diversify our market share, but on the other side it will make a more complementary product,” says Ghorayeb.

That’s an advantage that Uniceramic, the other local manufacturer, doesn’t have. Uniceramic, which is 39% owned by the Ghorra family, produces just floor and wall tiles at its factory in Chtaura. Nonetheless, it has the larger market share in tiles with about 30%, while Lecico claims 15%. Imports account for the rest of the estimated 8 million m² market. More importantly, Uniceramic is in a profitable position, with 1999 showing an increase of 15% over 1998’s net profit of $1.05 million, unless provisions are increased.

“Lecico’s going through restructuring and this is costing them a lot of money today … we had done that in the previous three years so we were a little bit ahead,” says Nabil Ghorra, the assistant general manager, explaining his company’s better fortunes despite the downturn. Joseph Ghorra was among the founders of Lecico, which held a 36% share in Uniceramic until two years ago. The $4 million raised was reinvested into Lecico.

At $7 to $8 per m², Uniceramic’s prices are comparable to Lecico’s $6 to $8.25 per m². But Ghorra insists he’s targeting the import market share. To that end, the company is monitoring trends in colors and designs from Europe and expanding its size variations from 11 to 15 by the end of 2000. Lecico counts three sizes and will increase that to four. Ghorayeb acknowledges that Lecico cannot compete with the sophisticated manufacturers from Italy and Spain. His strategy is to protect the company’s current share of the tile market, and target growth in sanitary ware.

In this connection, Lecico was given a boost by its joint venture with Sanitec, a Finnish manufacturer of sanitary ware, which has operations in Europe, Southeast Asia and the Middle East and recently acquired the Dutch company, Sphinx. Last year’s net sales of Sanitec and Sphinx combined are expected to total about $800 million. Sanitec purchased a 50% share of the controlling stake in Lecico in 1997. Sanitec’s Wolfgang Molitor came on as Lecico Group’s managing director, while Gilbert Garghour retained his position as president. Together they own 96% of the Lebanese operations and 76% of Lecico Egypt.

“Lecico is pushing more on the sanitary side because that is Sanitec policy, they’re not in the tile business at all,” says Ghorayeb. Now comes the move to modernize the local sanitary ware facilities, which will suck up a yearly investment of $600,000 to $700,000 over three years, and gradually return to full capacity.

In Egypt the company is undergoing expansion. With an investment of $21 million, Lecico opened a second plant. Starting with a production level of 1 million pieces a year, the factory’s output will gradually be increased to 4 million. That would bring Lecico group’s total production to 7 million if the Lebanese plant reaches its full capacity of 800,000.

Increasing production is one thing, but what’s the firm’s strategy to sell more? In 1997, Lecico began creating a greater presence by establishing an active marketing division and building showrooms. Currently at three, that number will be increased to five or six in three years. Through its technical agreement with Sanitec, Lecico will begin producing European models here, including brand-name items. Ghorayeb also hopes that the new Lebanese norms for sanitary ware, established in late 1999, will be enforced and keep poor quality products off the market. But for Mansour Ayoub, sanitary division manager of Abdulrahim Diab, agent of American Standard and Ideal Standard, it’s another bureaucratic nightmare, requiring certification with each shipment. He questions the timing and reasons behind Lecico’s push for norms.

Lecico is also pushing for an increase in customs duties, which are about 25%. Unless the government can decrease energy costs and assure fair bilateral agreements, Ghorayeb sees higher tariffs as the only way to save Lebanese industry from a certain death in the face of low-cost imports. Importers disagree, and say it goes against the trend of opening world markets.

“Customs duties have never been effective in protecting industry, because if you can’t compete you shouldn’t be there. It’s artificial competition,” says Mazen Zantout, managing director of Wafco, a local distributor of Spain’s Roca sanitary ware.

Nonetheless, neither Zantout nor Ayoub consider Lecico as direct competition. Targeting largely the medium to high-end market, they believe the local manufacturer could only soak up some of the higher quality portion of the low-end market if prices are bumped up with higher duties. A sanitary set, bath tub not included, from Abdulrahim Diab sells at a low of $400 and an average of $800 to $900, and for Roca the low end is $500 and average $650. Lecico says it can supply the low, medium and high end of the market with prices at $120 to $500, and claims a 58% share of the low-end and 59% of the mid- to high-end market. Importers aren’t having an easy time either. Abdulrahim Diab has seen its sales drop by 16.6% since 1995, though it staved off a worse fate by bringing in more medium to low-end products.

From Egypt, where Lecico has a 40% share in sanitary ware, the firm hopes to expand further into the European market. That will be given a boost through its partnership with Sanitec. Exports will also target the south of the Arabian peninsula. From here, Ghorayeb is eyeing the Syrian market, which he currently gauges at 700,000 to 750,000 pieces a year, and Iraq for 2001. Sanitary ware and tiles were included in the Lebanese-Syrian free trade agreement last fall. Lecico estimates it can supply 150,000-160,000 pieces, having already established a chain of dealers.

With that, Lecico would move back into the black for 2000. Ghorayeb has received confirmation from Lebanese officials that the Syrian market will be open to tiles and sanitary ware starting in February. “We hope it will be a good year,” he says. But trade between the two countries has declined in the past two years, while industrialists complain that red tape has kept the border from opening up. Lecico Lebanon will still have to fight hard not to sink further, while its Egyptian sister looks ready to clean up.