T he optimism following the Israeli

withdrawal is wearing thin.

Although some property prices

have fallen up to 50% from the peaks of

1995-6, most analysts and practitioners

fear that the market has yet to bottom out.

Bernard Mouchbahani, senior manager of

project finance at Lebanon Invest, is just one

who thinks prices are too high: “We are still

overvalued when you look at the state of the

economy and what property costs in the rest

of the world.”

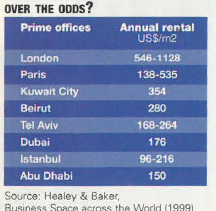

Despite prices that are high compared

with Dubai, Abu Dhabi or Istanbul (see

table), there is a crucial oversupply in many sectors of Lebanon’s real estate market.

Even if the economy were to pick up, there

is a huge slack to be taken up, says economist

Marwan lskandar: “Eighteen percent of

residential is unoccupied, as is 20% of nonresidential.

The total investment in these

properties could be around $6-7 billion, and

it might take seven or eight years for this

oversupply to be removed.” Others believe

there is not so much of an oversupply, but

rather the wrong kind of supply. “Much of

the vacant stock is of very poor quality,” says

Michael Dunn, general manager of Healey

& Baker in Beirut. “Cheaper and better

alternatives are available already, and if the

overall demand increases, the supply of

better stock will increase as well.”

The crucial issue is demand. Whatever the

quality of supply, economic growth at the

moment remains an aspiration. The key

issue for those who don’t see an upturn in

real estate is the failure of the government’s

fiscal policy, which they say is leading

the country toward an economic shakedown

that will hammer real estate as surely

as any other sector.

Many have lost any belief that the government

can turn the macro-situation round.

Each month, economic indices emerge that

chart recession. Last year’s GDP growth was

-1 % and is forecast at a mere 0.5% for 2000,

according to the Economic Intelligence Unit.

The ballooning deficit has topped 50%,

while the debt to GDP stands at 140%. “The government says don’t rock the boat, but the

boat is sinking,” says a leading financial services

manager. “Assume a six-month delay

after the elections until they all settle down in

their new p01tfolios. Remember the weight

and speed of the bureaucracy. Assume the government

does nothing, or rather that it makes

mistakes. Then, you must assume a macroeconomic

shakedown.”

The country, he says, is heading firmly

down that road. “The private sector is creeping

into default. The government will be

doing the same, or worse.” Such pressure

would clearly be deflationary. People and

businesses would have less to spend.

Demand for goods, services and homes

would fall. So, as a consequence, should

property prices. If they did not fall (because

would-be seUers continued with the so-called

‘comparative’ methods, or simple wishful

thinking, rather than looking at yield), then the

market would become even more illiquid.

Underlying the economic indices are the

political failures that undermine confidence.

The saga of the Beirut Trade Center – aka the

Murr Tower – has done nothing to improve

matters. When the Solidere general meeting

in June deferred a proposal to sell the 40-storey

building to interior minister Michel Murr,

many in the real estate business bemoaned

what they saw as yet another postponement of

overdue progress in downtown. “We expected

this sale would speed up the supply of permits,”

says one real estate expert. Solidere’s

land sales, tumbling from $118 million in1998 to $37.5 million in 1999, are one indication

of declining demand that no amount of

political posturing can change.

But against the deflationary pressure

there would be a contrary pressure, which is

where things could get interesting. This

would come from the upper middle class and

above, who have savings. “They haven’t

been investing in real estate because of the

excellent returns on the Lebanese pound,

Nasdaq or whatever,” says the financial

services manager. ” In a shakedown, they

may move money into real estate on the

assumption that it’s better to trust the land

than the government. If the desire to invest

in real estate is as strong as the deflationary

pressure, then prices won’t fall.” According

to Karim Salameh, director of the Property

House, prices have already been falling

since 1996 or 1997. “But there is a certain

floor,” he says. “If at that point, a virtuous

circle of investment is created, then prices

could go up again.” Perhaps. But with the

slack in the market and current macroeconomic

s ituation, most analysts believe

prices are unlikely to rise across the board.

Recession does, however, bring its own

opportunities. Benefiting from steady yields

in a falling market is part of the thinking

behind the Real Estate Investment

Company (REIC), Eagle One, which the

Property House announced in February.

The plans for a ten-year, close-ended fund

have been delayed by the fears and uncertainties

that surrounded the Israeli withdrawal.

The company’s strategy is to buy

properties with good existing tenants whose

prices have fallen but whose yields have

remained constant. Such opportunities

should increase as pri1.:es fall – giving the

investor both the income from the yield,

either directly or in the case of REIC

through a dividend and capital gains as and

when the market improves.

Whatever happens to the market overall,

there are always prices that buck the general

trend. Picking the right spot – in time and design as well as space – is what turns real

estate from a passive resource into a marketable

commodity. In retail, BHV and

Monoprix, Spinney’s and ABC have all

been successful despite the recession. At the

same time, Hamra and Verdun have managed

to maintain prices at around $5,000 and

$5,000 to $7,000 respectively and have

attracted high-profile brands like Etam,

The Body Shop, Mothercare and DKNY.

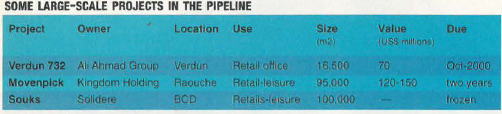

The Ali Ahmad Group is confident that

Verdun 732, which is nearing completion,

will repeat the success of Verdun 730.

Consumer attraction to high-profile brands

is clearly increasing. International retailers

have increased their numbers of shops from

110 in 1997 to 144 today, with those held by

US retailers rising from 26 to 38, according

to a recent survey by Healey & Baker.

Raja Makarem, managing partner of

Ramco and broker of the recent deal that will see Virgin open in downtown, believes that

in general prices are about as low as they will

go. “I think we’re now at the bottom of the

hole, and people are already sniffing round

for bargains,” he says. “Don’t forget that

Lebanon is a small country, and that many

people would like a foothold here.” And

despite the construction downturn, a number

of ambitious large-scale schemes are steaming

ahead. Down by the sea at Raouche,

Kingdom Holding is well into the construction

of a complex with a Movenpick hotel

(see box). Like Solidere’s souks, such a

development is large enough to have strong

knock-on effects elsewhere. Whatever happens

to prices, it will be the ability to see and

take the opportunities that will distinguish the

sheep from the goats