Starting next year, major players in the oil and gas industry will have some extra financial reporting to do. Any company listed on a European Union member state stock exchange (whether or not it is registered in the EU) or domiciled there will have to publish payments to foreign governments on a project-by-project basis beginning January 2016. A similar rule is under development in the United States as well, although it will likely not go into effect until later. The 2013 EU directive – according to a European Commission (EC) press release – is the result of campaigning in the late 1990s and early 2000s by civil society organizations around the world for more transparency in an industry long associated with bribery and corruption, particularly in impoverished but resource-rich developing countries. The goal of these measures, as the EC puts it, is to “provide civil society in resource-rich countries with the information needed to hold governments to account for any income made through the exploitation of natural resources, and also to promote the adoption of the Extractive Industries Transparency Initiative (EITI) in these same countries.” Unlike the new legal requirements for industry, the EITI is voluntary and puts the onus to report on governments. Some countries, however, are making the initiative’s requirements mandatory by codifying a commitment into law.

Given that Norway – which is not an EU member state – is currently implementing a similar reporting rule on its own, half of the 12 companies currently pre-qualified to drill as operators offshore Lebanon would be legally required to do project-by-project reporting if and when exploration and production begins here (three more companies are based in the US and could have similar reporting requirements in the future). This international push for transparency would go a long way toward making the bribing of Lebanese officials more difficult for international oil and gas companies operating in the country. This would alleviate the fears of corruption that local businessmen and politicians with industry ties, like Fouad Makhzoumi, have.

Following the money

Civil society players involved in the transparency push see a direct link between publishing payments by oil companies to developing country governments and more widely distributed economic prosperity in those countries. Daniel Kaufmann, president of the Natural Resource Governance Institute – an international NGO involved in transparency initiatives – tells Executive that, “There’s an enormous developmental rationale behind the transparency calls.” If citizens in developing countries know exactly what their governments are paid, they can demand those revenues be spent in certain ways or at least cry foul when they go missing, so the logic goes. As for whether or not development benchmarks can be legislated the way transparency was, Kaufmann does not see a practical way forward. “You cannot do development by edict, by law, unfortunately; otherwise we would have solved it a long time ago,” he says.

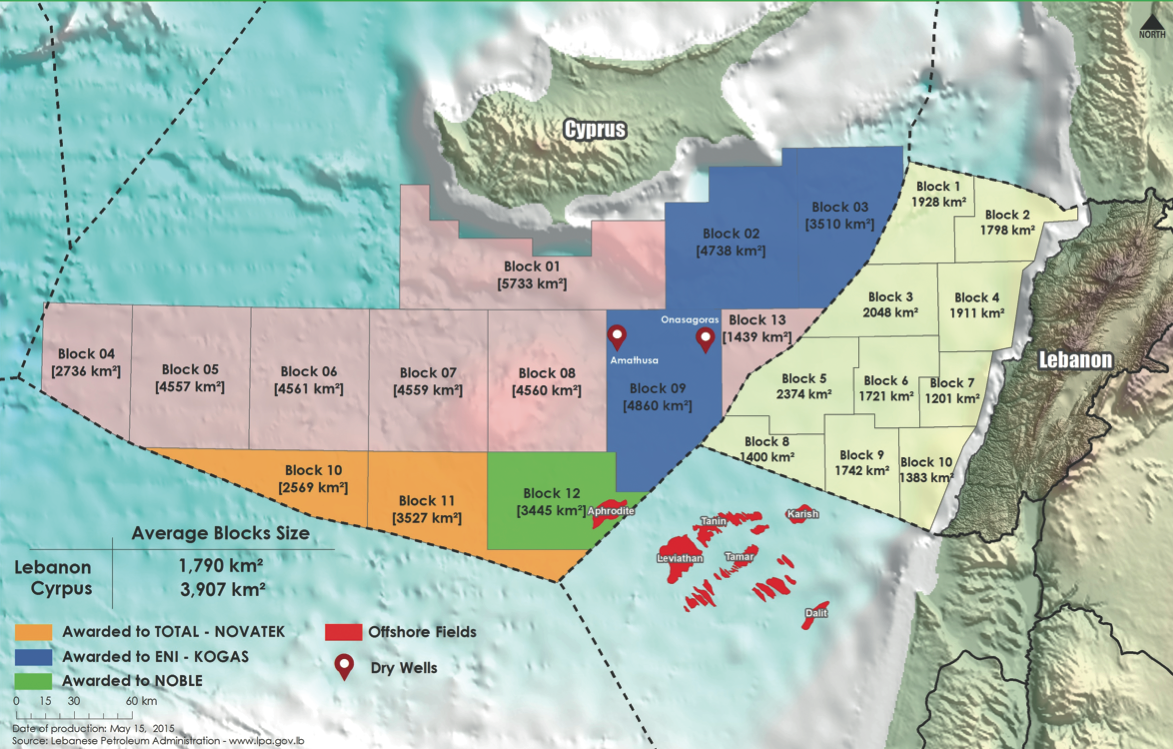

Block boundaries. Source: Lebanese Petroleum Administration & Executive.

Lebanon is still years away from even knowing for sure whether or not it will have oil and gas revenues, yet local legislation exists – and more is being drafted – aimed at developing a clean hydrocarbon industry (see story page 36) with money well spent. The barrier to transparency and good governance moving forward – as always – will be proper implementation and enforcement of the laws in place if and when the money starts flowing.

Three questions for NRGI President Daniel Kaufmann

E: Oil and gas companies are not always completely honest about who their owners are. Some even register in jurisdictions that allow actual ownership to be obfuscated. The notion of beneficial ownership, therefore, calls for finding out who is really profiting from a business. Where does beneficial ownership stand today as part of the Extractive Industries Transparency Initiative (EITI)?

Beneficial ownership is part and parcel of the expansion of the EITI requirements which began a year ago. Before EITI was very narrowly focused on the disclosure of revenues – the payments that companies made to foreign governments. But then it expanded very significantly to also include disclosure in terms of contracts, enterprise finances – and beneficial ownership is a crucial part of that expansion. It is quite complicated, requiring political will and consensus with many stakeholders. It’s in a pilot phase and not yet under fully fledged required implementation, but that is the direction it is moving, and we consider it an absolutely crucial part of the triangulation of information. It is very useful to know the payments, the revenues coming to the budget – if one doesn’t know what the original terms of the contract [were], how can one assess whether it is a good deal or not? And [knowing] who benefits [is important] because if there are interlinkages with politicians it might not benefit the whole population but only some cronies and elites.

So [beneficial ownership] is a crucial aspect but there is still a way to go before fully fledged required implementation. We are reviewing the results and lessons of the pilot phase so at the board level we can have discussions as to how it should be implemented. Because let’s face it, there are also practical issues regarding implementation. Do you always rely on public government registries? The answer is probably not. Instead, one goes to a company and basically asks them to fully disclose and there are ways to monitor and vet.

E: Is there a benefit to adopting the EITI for a country like Lebanon before signing exploration and production agreement (EPA) contracts?

Absolutely. Already you can start setting up the systems for transparency once the contracts come about – the structure of reporting. Many of the countries that might not be rich in natural resources are adopting the EITI because there are also issues of transit pipelines and the revenues from those. Or if it is an important financial center, or there may also be trading issues involving oil and gas at ports. So it is not all about production – for instance we’re working very hard for the Swiss to implement the EITI and they don’t have [a significant extractive industry] but they have very important trading companies.

E: How important is international legislation like the United States’ Dodd-Frank Act or the European Union’s Accounting and Transparency Directives to hold multinational companies accountable, and what can be done regarding governments?

The mandatory disclosure requirements following the Dodd-Frank initiative and the EU Directives essentially puts the pressure on companies to do their part to disclose. Why do I mention companies? In terms of the responsibility of the recipient government to also disclose that’s where the EITI is an important initiative. So what’s important [is that], eventually in Lebanon if there are deals for exploration and production, international companies report, and that will be governed by the EU Directives and the Dodd-Frank. That should be good enough, but from a Lebanon perspective it’s going to be making the government accountable and that’s where the EITI comes in – some countries are enacting legislation to implement the EITI to make it internally mandatory.

Revenue plans

The 2010 law governing offshore oil and gas activities calls for the creation of a sovereign wealth fund (SWF) with a dual purpose: spend some, save some. Article three of the law elaborates, “the capital and part of the proceeds [from oil and gas activities] shall be put in an investment fund for future generations, leaving the other part to be spent according to standards that will guarantee the rights of the State and avoid serious, short or long term negative economic consequences.” In an indebted country with poor service provision and crumbling infrastructure like Lebanon, hashing out the details of what gets spent, what gets invested, and how will be an important policy debate to follow.

One apparently settled revenue-related dispute is whether Lebanon should open all 10 offshore blocks for bidding in the first licensing round, or award rights to only a few blocks at first and have multiple licensing rounds over the course of several years, if not decades. Parliament Speaker Nabih Berri allegedly favored the first game plan, which would have increased the state’s chances of bringing in cash as quickly as technically possible, which can still take up to a decade, because a commercially viable discovery is more likely if 10 blocks are being explored instead of only two. One drawback of licensing all blocks together is losing the ability to negotiate from a position of power in the future. If some blocks are held back from the first round of licensing and a big discovery is made, there will arguably be more interest in future rounds and the state might be able to secure better terms. The Lebanese Petroleum Administration (LPA) website lists five blocks as “open” (see map above), suggesting they will be the only ones up for bidding in the first licensing round. In a written response to questions for this report, the LPA speaks of “gradual licensing” as a way to “smooth revenues.”

The waiting game

When Lebanon will move from planning how to manage revenues to actually managing them is anyone’s guess. A commercially viable offshore oil and/or gas reservoir cannot be found until holes are drilled into the seabed. Lebanon intended to award offshore drilling rights to oil and gas companies in February 2014, but cabinet’s failure to pass two decrees (one outlining the tender protocol and model exploration and production sharing agreement, the other delineating offshore blocks up for bid) stopped this very important part of this sector’s development in its tracks. While the LPA notes that “this delay has a high opportunity loss cost,” lost time has not necessarily been wasted. Additional oil and gas prospectivity survey data has been collected in the past 12 months, and the LPA says it is re-interpreting existing offshore data in light of dry wells in a Cypriot offshore block that borders Lebanon’s acreage with plans to do more analysis in 2016. The more quality data available to drilling companies, the less time spent before well sites are chosen. Often countries have no data before signing exploration and production agreements, so when those deals are signed here, drilling could begin faster than industry average. That said, the 2010 law governing offshore sets a maximum limit for the exploration phase at 10 years.

Still a roll of the dice

Given how far away Lebanon is from production – assuming it ever gets there as the possibility of not finding a commercially viable discovery can never be ruled out – speculation on how current price trends will impact the future is arguably useless. Worth noting, however, are three wells drilled in the past year and the reminder they bring that fortune can so easily change. In late 2014 and early 2015, Italy’s ENI and South Korea’s KOGAS drilled two wells in a Cypriot offshore block near Lebanon’s offshore acreage. Both were dry. Around the same time the second disappointment was being burrowed into the seabed, France’s Total announced it wouldn’t even drill in the Cypriot blocks it had licenses for because the risk of failure was too high. After a 2013 downgrade in the estimated size of Cyprus’ only offshore find – a field called Aphrodite – the news made the already questionable proposal to build a multi-billion dollar liquefied natural gas export terminal seem even more unlikely. Not far to the southwest of the dry wells, but just across the Cypriot maritime border in Egyptian waters, ENI found the largest field yet in the eastern Mediterranean in August – dubbed “Zohr” and estimated at 30 trillion cubic feet of gas, it is larger than the previous record holder, Israel’s Leviathan. The find is so close to the Cypriot border that, at time of writing, there were speculations in the Cypriot press that it might bleed over, meaning Nicosia would get a cut of revenues under an earlier agreement with Cairo. Either way, Total said in response that it would re-evaluate plans for the neighboring Cypriot block to which it has rights. Even in times of decreased investment because of the price pounding, ENI’s discovery has certainly put the eastern Mediterranean back in the headlines.