We recently went on a banking spree at a top foreign bank where we both have accounts. One of us queued behind six people waiting for a teller, which took 15 minutes. At the counter, after watching paper shuffling and stamping, plus signing four documents, the grand total was 25 minutes.

At the same time, the other went looking for her biannual statement, which never materialized. After two clerks thumbed through stacks of statements, a bank officer appeared and announced that the lost statement could be collected several days later. Time: 45 minutes. After the second visit, it will be 45-plus.

One day all this will be taken care of at the click of a mouse. Log on. Click. Check balance and do a transfer. Click, click. Log off.

E-banking has already begun in Lebanon, however modestly. A number of leading banks have taken the plunge with an informative presence online and possible further development in the future. Customers at several banks can sit at home and browse services, order checkbooks and enter the scary world of looking at their account balance. A foreign giant in Lebanon has already trumped local competitors. Banque Nationale de Paris Intercontinentale (BNPI) locally launched BNP Net last September, allowing clients to view exchange rates, stocks and mutual funds and move money from one account to another clickety-click.

But BNPI won’t be alone for long. Right around the corner, savvy Saradar will add transferring funds and ordering credit cards to its virtual menu. Credit Libanais, which is now on a tear in profit growth, up 65.6% year-on-year in the first three quarters of 1999, will soon launch e-banking as well, including moving money and loan applications.

Virtual banking is on its way, but will it be a booming business?

Not overnight. The first argument against it may be the way the Lebanese like to bank. They are used to the human touch inside the brick-and-mortar outlets, which could hinder luring customers to use the cold comfort of hardware. According to James Ross, assistant general manager at Bank of Beirut, the habit of customers walking in to see actual transactions and meet with an officer to discuss credit or products may be hard to break, especially with the older generation. “But Lebanon will gradually adapt. The depersonalized aspect will move upwards, from ATMs to phone banking to e-banking, which will probably crystallize in about three years.”

The number of Internet users is still insignificant compared to Western markets. Data Management’s managing director Maroun Chammas estimates a total of 50,000-80,000 subscribers. Since an account can be used by more than one person, the total number of users is higher. The Professional Computer Association (PCA) estimated a total of 100,000 users last fall, see “Going too low,” November 1999. While that number would be expected to increase at a much faster pace following the price drop for unlimited Internet access last fall, from around $29 to as low as $6.66, IntraCom’s managing director Bahjat el-Darwiche doesn’t think so. He estimates the market growth is 3,000 users per month, or close to 40,000 annually.

One major impediment to the growth of the Internet community is PC sales: The computer market has not caught fire yet. The growth of Internet subscribers is in sync with the PCA’s statistics on PC sales in Lebanon, roughly 40,000 annually.

According to Chammas and Darwiche, prices for PCs are too high in the stagnant Lebanese market. And telephone bills are too steep as well: The cost of a telephone connection is $1.40/hour.

Since it might be difficult to pull customers from branches and there aren’t enough Internet users yet, the younger generation is more likely to embrace e-banking. Darwiche maintains that the potential market for new subscribers is mainly fresh graduates. “They get free access in the universities, so once they graduate they buy a PC and log on. How many students are going to graduate each year? 30,000-40,000. That’s the potential.” And the bankers know it. “If I were a student about to graduate, next year I’d bank on the Internet,” says Andrew Stephens, head of retail banking at Credit Libanais. “They know how to use a PC, they’re not worried that their money is in the ether somewhere. It’s the new generation, and we will target them.”

That’s why some banks recently launched major marketing campaigns offering free Internet access with PC loans. Their target was mainly household clients or, more specifically, students. But these are future clients. The primary goal for e-banking now is to retain existing customers. The Lebanese market is small, around 3.5 million people with about 60% having a bank account, and the market is saturated with financial institutions, 65. “The problem is that you don’t get economies of scale. If I want to operate Internet banking, how many customers am I going to get? 10,000?” says Stephens. “There are 3.5 million people in Lebanon. Let’s say there’s 1 million of them that I can consider as potential clients. They’re not all going to bank with me. Everybody banks with several banks here. Your share of the wallet is small, so it’s a real fight for customers.”

If just a few leading banks do it, customers might migrate. None of the larger banks are going to be left out and risk losing major accounts; expect e-banking to flood the alpha group in no time at all. Carlos Heneine, Saradar’s head of strategic planning and marketing, says, “Lebanese banks are all concerned with serving their own existing customers. That’s what we should do, retain valuable customers. In other words, I have a customer who’s valuable to me, who has a PC, and somebody else offers him Internet service, and he finds it convenient. I can’t afford to lose him.”

If the top banks are the ones that will work with e-banking to keep their customers, what will happen to the smaller ones? If the smaller banks are unable to afford to keep up, we may see the Internet banking wave followed by another wave: mergers. Pressure is already mounting on the smaller banks as the sector is experiencing a decrease in earnings, due to the economic slowdown. Everyone knows that the last thing an owner would want to do is sell his bank. That has been and might continue to hinder a merging trend. But if customers uproot from small banks without e-banking and head for the larger banks, acquisitions will definitely pick up.

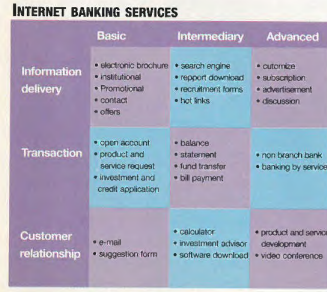

Even though many financial institutions will soon take a step from the basic to the intermediary phase in Internet banking, see chart, moving up to full cyber-service is out of reach for now. This is where regulation and security come into play, and the central bank will have a crucial role. The central bank’s attitude about banks offering products and transferring money within the same institution has been laissez-faire. But inter-bank operations online, like moving money from one bank to another, are perceived as living in the danger zone.

“Bigger operations in the future, which will entail higher risk, are in need of full security,” says the head of the information technology department at the central bank, Ali Nahle, who is in charge of setting up safer e-banking. He says it will take two to three months to regulate but two years for security to be implemented.

This will probably delay one of the best markets available. The Lebanese expats, who are in tune with the benefits of riding the tech waves and have accounts in local banks, would jump on the opportunity. “They’re probably more used to banking in those terms, they tend to be more wealthy than the Lebanese here, and if they want to maintain banking facilities in Lebanon, they could easily access us through the Internet,” says Stephens. But without advanced e-banking, they won’t be able to move money overseas.

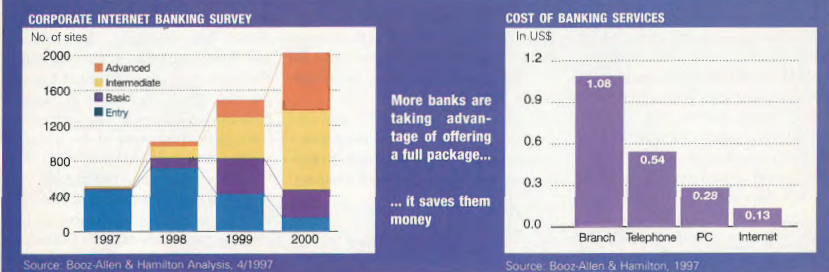

One of the most blatant benefits of e-banking is efficiency. From Booz-Allen & Hamilton’s study on US banks, the drop in cost per transaction from in-house to Internet services is mind-boggling: $1.08 to $0.13, see graph. No study has taken place in Lebanon, but the US figures prove that e-banking can bring down costs. Yet there is a hitch in the Lebanese system. If there is less shuffling of paper, stamping and posting, downsizing staff is the key to cutting costs. But political and social pressure has made it difficult for businesses to lay off employees.

Still, e-banking could be the tool of the future for retail banking, which is on the upswing among the leading banks, pumping out more products and services at a steady pace.

Picture this: Each time you go to a bank to carry out a transaction, would you be pleasantly surprised if a teller tried to sell you a product over the counter? Intercepted on the way out by a staff member as you’re counting your money? Not likely. Instead, it would be more convenient for customers to see products on the screen after logging on to do some banking at home.

This would be the same for cross-selling products, an important catalyst to see banks increase volume that could help push up non-interest income. “Services and reminders, for example, are much easier to do with Internet banking,” says Stephens. “We can send an email to tell clients when the loan is due and ask if they want another one. If they have a mortgage, we can offer new furniture or a new car. We can talk to them more easily. Call you at home and you’re not there. Maybe a mobile phone, but you’re at a restaurant and you don’t want to talk now. With Internet, bam! You see it, you read it and I’ve got you.”

In the long term, e-banking can take on much more power for retail banks. A recent Booz Allen & Hamilton article explains how: “Using new, analytical, decision support capabilities, customer data can be mined to create predictive models of customer response and behavior.” With a customer profile and keeping track of client behavior, spending habits and activity on their websites, banks can determine who to target with which products.

The full development of e-banking in Lebanon will take time. But over the long haul, there is a good chance that the bank model you see today will change. Banks may get into e-commerce themselves. This is no different than Europe, where banks are creating shopping stores on their websites to get those credit cards rolling.

Joint ventures are an alternative, where the bank cashes in on transactions without having to worry about the web design or marketing side. Credit Libanais has teamed up with Data Management to create NetCommerce, an online shopping mall.

The Internet is also creating brickless banks. European start-ups, usually subsidiaries of brand names, include egg.com, Smile (smile.co.uk), and First-e. With low overhead and only a warehouse to operate from, these banks can offer higher interest rates on savings accounts and lower card rates. Customers can open accounts online, as well as apply for loans and receive a response within minutes, or even go shopping. In the longer term, as boundaries fade, these branchless banks could be a threat to the local industry.

But as banks start getting into this new virtual discovery, whether it pays off or not, customers should benefit the most. Convenience is the name of the game, and if the main focus of banks is to retain clients by offering a better service, luxury will fall into their laps.

Just imagine: At 2:30 a.m. you come home after paying for a big dinner using your debit card, and you know that you need to transfer funds into one account to cover your expenses for the rest of the week. You don’t want to leave your office, sit in Beirut traffic and spend time in the bank’s lobby the next day. Logging on before getting a few hours of shut-eye would do the trick. So the next time you’re stuck in line, ask your branch manager, “Ever heard of Internet banking?”