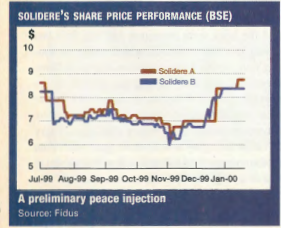

“There’s a good chance that Lebanese stocks will jump 40% to 60% if there is a peace agreement this year,” proclaims Philip Khoury, vice president at Merrill Lynch in London. Ask a local broker and he’ll say the same. And we’ve already seen some action. With negotiations almost building up steam, Solidere’s A and B shares jumped 40% from their November 1999 lows through January.

No analyst doubts that Solidere shares will benefit; investors expect more money to come in to gobble up Lebanon’s prime real estate once there is peace, bringing brighter days to the company’s earnings. An increase in Solidere’s shares would lift the entire market as its market cap alone accounts for about 70% of the Beirut Stock Exchange (BSE). Bank shares might follow. “Even though their earnings are not as good as before, price/earnings ratios are at fair levels,” says Jean Riachi, chairman and general manager of Financial Funds Advisors. “You’ll get an increase.”

But once prices reach higher levels and excitement settles down, will peace support stocks for the medium term, pushing prices higher?

Looking at the fundamentals, investors have to consider how much Lebanon’s economy will benefit from peace. According to Marwan Iskandar, a leading economist, the market will get a decent boost from a deal. He believes tourism will improve once Lebanon, Syria and Israel complement each other as destinations. There is a good chance that Lebanon will normalize its economic relations with Israel in a fairly short period, forcing the private sector to become more competitive, and Arab countries will have more freedom to consolidate their economic policies to create a common market. “The most important change will be a boost of confidence. It will give more incentives for foreign investors to come onto the scene in the Middle East, including Lebanon,” says Iskandar.

Others have doubts about how much Lebanon will benefit. Paul Salem, a development and political analyst, thinks many expats will move money back home. “And the agreement could stimulate renewed interest by the US, Europe, and possibly Japan.” But Salem expects foreign direct investment (FDI) to trickle into Lebanon: “This is a very small country; you’re not talking about India or Egypt.”

Ziad Maalouf, vice president at Middle East Capital Group, is wondering if it will even be a trickle. “Why would there be FDI? We have the highest labor cost in the region, the highest price of land, the highest price of raw materials, energy, water and the highest cost of living. Why would anybody want to build a manufacturing plant here?”

Another analyst doubts that Arab nations will liberalize trade. “Harmonizing those relations never got to what it could have been and Israel was not really in that equation. It’s always been politics before economics in the Middle East. They can eventually pull it off, but it will take time.”

As for normalization between Lebanon and Israel, Salem says: “There might be formal clauses related to normalization and trade attached to the peace agreement, but if documents are signed, I don’t think those in Syria and Lebanon will be very open to it, just as we saw in Jordan and Egypt. I’d expect a cold peace at all levels.”

Maalouf draws a parallel between Jordan after peace and what could happen in Lebanon. “Before Jordan signed, you wouldn’t believe how much excitement there was in the market. But stock prices today are close to where they were when peace arrived. The benefits from peace they were hoping for never materialized.” From 1997 to 1999, Jordan’s GDP growth rate dropped from 2.2% to 0.5%. Despite better business opportunities in Lebanon, Maalouf says Jordan was better prepared. “We have to get our house in order.”

Lebanon is in dire need of administrative and fiscal reform. Debt-to-GDP reached 130% at the end of 1999. The deficit was reduced from 43.73% in 1998 to 42.41% in 1999, but missed its target of 40.5%. The Economist Intelligence Unit predicts that Lebanon will have the slowest growth rate in the Middle East this year.

“The peace agreement will not go down to the bottom line right away,” says Salem. “I’m optimistic in a limited, cautious way. You’ll have a country that’s not at war. It’s an essential building block for economic development and important for any investor who’s thinking of investing in Lebanon.”

Investors are still waiting for BSE reform. Riachi says open trading and a regulatory body are essential. “We have to have a real market to see stocks move.” He predicts that after an initial jump in prices, stocks will level off until investors see more positive results. A building block will be a good start, but it’s difficult to predict what will happen after the flurry.