It has never been easier to be branded a financial pariah. You wake up one morning and when you check your correspondence you find that you have been given the ominous title of “specially designated national” (SDN) by the Office of Foreign Assets Control (OFAC) at the United States Department of the Treasury.

This designation means that, according to “evidence” which can range from classified information of US intelligence services to reports in your local newspaper, you have been found to be a perpetrator of terror, narcotics, weapons of mass destruction or other threats to the national security, foreign policy or economy of the United States. As of this moment, you are a financial outcast with whom no US citizen or corporation with American interests will do any business. If you have assets in the US, these will be frozen.

International criminals, but also people with ties to organizations such as Hezbollah and persons doing business with sanctioned countries such as Iran and previously Cuba, are frequently added to the SDN list without much public attention, except for rare cases when big names in business are concerned. In one such recent case, Lebanese magnate Kassem Hejeij (Middle East and Africa Bank) was listed by OFAC on the grounds of “direct ties to Hezbollah organizational elements”. His alleged misdeeds also included investing “in infrastructure that Hezbollah uses in both Lebanon and Iraq.”

The worst thing for economically active people hit by the SDN hammer is that their businesses are just as ostracized as they themselves are. This was the implication for Hejeij when he was placed on the SDN list in early June. His business interests, most importantly the Middle East and Africa Bank (MEAB) under his chairmanship and majority ownership were in acute danger of being crippled. Hejeij, despite protesting and declaring his determination to fight the SDN label foisted upon him, eventually stepped down from his position, sold his shareholdings in MEAB, and overnight became a thoroughly private individual as far as business is concerned. Within one month, MEAB had presented a new management team, gotten busy on new business plans and started communicating its intended future.

Is there a defense?

The good news about the case of Kassem Hejeij and MEAB is that it cannot be compared to the notorious dismantling of the Lebanese Canadian Bank on the basis of money laundering allegations by the US treasury more than four years ago, says Paul Morcos, a Beirut-based lawyer and consultant specialized in banking. “It is not realistic to compare the two cases of LCB and Kassem Hejeij since the [Middle East and Africa] bank was not listed on OFAC but rather the name of the chairman,” he explains.

In the LCB case, the bank was sold and its identity dissolved to control the damage. According to Morcos if MEAB itself had been accused, it would also in the Hejeij case have led to “catastrophic results” beginning with a total shutdown of all correspondent banking relationships. “This distinction is to differentiate between listing the juristic person of the bank, which was not the case, versus listing the natural person. This is why I think that there was a chance to handle the situation differently than other cases when banks are listed,” he says.

Being based, as Beirut observers are, far outside the Beltway, it would be idle speculation to wonder why the treasury department’s officials chose this particular time to target Hejeij, or why the department’s top man in the Office for Terrorism and Financial Intelligence, acting (and according to President Obama to be fully appointed) under-secretary Adam Szubin, would last month issue a fiery press release specifically attacking Hezbollah and declaring that his office would “pursue all of Hezbollah’s revenue sources, whether charitable fundraising, criminal proceeds, or state sponsorship.”

Hopeful news from the de-risking front

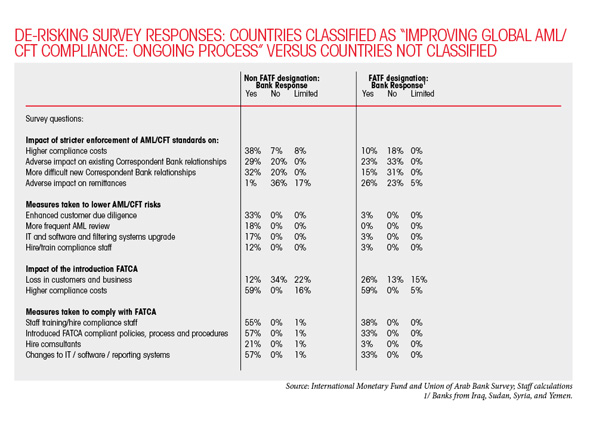

The good news is that de-risking and other impacts of greater compliance pressures are perceived as manageable by banks across the Arab world. A recently released joint study by the Union of Arab Banks and the International Monetary Fund shows that the region’s bankers noted increased costs related to correspondent banking due to stricter AML/CFT enforcement. However, “wholesale de-risking by global banks does not appear to have taken place so far,” the report said. On the other hand, regional banks did not indicate that they had taken several measures to improve their immunity to ML/FT risks.

The study was conducted in spring 2015 via a survey sent to 471 banks in 20 MENA countries. The response rate of about 25 percent was not very high and further research is warranted according to the study’s authors, but the exercise provided useful indications on the business impacts of AML/CFT measures, Foreign Account Tax Compliance Act (FATCA) and Basel 3.

The highest impact was perceived in the area of correspondent banking where 40 percent of responding banks indicated that these relationships were becoming “more demanding, more time-consuming, more complex, and expensive to maintain.” Impacts on remittance flows were seen as minor, and so were business impediments related to FATCA and Basel 3.

Impacts were more pronounced for banks in countries classified by the Financial Action Task Force (FATF) as having strategic deficiencies in AML/CFT regimes that are however in the process of being addressed under “high-level political commitment”. In the four MENA countries in this category – Iraq, Sudan, Syria and Yemen – banks’ responses indicated higher negative impacts on business due to the introduction of FATCA and significantly higher impediments of remittances but lower cost impacts due to the stricter AML/CFT regimes.

When compared with banks in the non FATF designated countries, banks in the four designated countries showed significantly less eagerness to take measures that would reduce ML/FT risks or to enhance their FATCA compliance. The study pointed to a possible reason for this underwhelming implementation of new compliance measures – a paltry 3 percent of banks in sanctioned countries enhanced their customer due diligence to lower ML/FT risks versus 33 percent in the other countries – in the fact that their nation’s inclusion on the sanction list nullified any individual efforts for achieving greater compliance. Over one third of the banks that responded to the survey – 41 out of 117 – were based in sanctioned countries.

Also a counter-intuitive result of the study was the situation of regional de-risking. Whilst the study did not directly identify the countries whose banks undertook regional de-risking, it said that about 10 percent of the survey respondents had closed some correspondent banking relationships with banks in sanctioned countries and/or weak AML/CFT policies – meaning that “de-risking of regional correspondent banking relations by MENA banks”, as the study termed it, is a subject which warrants attention.

Statements of this sort are well-worn in the American repertoire, as was the name of Hezbollah’s Mustafa Badreddine who was highlighted in the July 21 dispatch. In past scenarios, such sanctions messages were interpreted to be warnings, or threats, demanding good behavior from Lebanon.

Whatever the hidden sticks-and-carrots in the current American strategy may be, it remains possible that the last word has not yet been spoken on whether the potential threat to MEAB has been solved with the intra-familial transfer of chairmanship at the bank. In more general terms, however, all signals suggest that Lebanese and Arab banks cannot relax their attention when it comes to compliance with the US agenda.

One problem, Morcos says, is the American insistence on publicly confronting alleged financial facilitators of terrorism without giving these entities a chance to cooperate. He recalls how Arab participants in a 2006 workshop with officials from the Federal Reserve Bank of New York were asking the US entities not to expose Arab banks in public statements immediately after having discovered a concern, but first to employ information channels such as the financial intelligence units that exist in all countries of the region.

As Morcos remembers, this request was brushed aside by the official in question, with a reference to the victims of the 9/11 Twin Towers attack who had been murdered without any consideration. The single-minded US desire to fight terrorism finance in the sharpest way possible has kept relationships problematic since that time, Morcos says, and argues, “Now is another occasion to reemphasize that any subpoena and any suspicion should be channeled through official channels, i.e. the financial investigative units and through the central bank of Lebanon, especially since it works efficiently. Why not adhere to this channel instead of spreading the word as news, which has a dramatic impact on depositors’ interests and even on the sector here?”

No alternative to compliance

Financial institutions need to abide by anti money-laundering (AML) and combating the finance of terrorism (CFT) rules, and have had to learn their lessons in this regard as even top international banks changed their processes only after being hit with multi-billion dollar fines for having facilitated financial transactions with sanctioned countries such as Sudan, Iran, and Cuba, says the secretary general of the Union of Arab Banks (UAB), Wissam Fattouh.

“In my opinion, penalties for non-compliance with AML and CFT or also with [Foreign Account Tax Compliance Act] regulations are very good. Banks need to behave and this is not only about issues related to AML and CFT but also about corporate governance and violations of rules such as exchange rate manipulations,” he says.

While the strengthening of international regulations and enforcement of penalties against rule-breaking banks comes with general questions about the proportionality and effectiveness of such penalties, Arab banks in Fattouh’s view struggle with a different set of challenges that are grounded in the presence of economically powerful terror organizations, namely ISIS.

In order to deny these organizations an increase in power because of their ability to provide jobs, populations in ISIS-affected countries need to be offered economic opportunities and better jobs. In this context, Arab banks have a major role in developing employment structures through the financing of small and micro businesses.

[pullquote]“Advancing financial inclusion and job creation are priorities…in the war against the sources of terrorism.”[/pullquote]

“Advancing financial inclusion and job creation are priorities where banks play a role in the war against the sources of terrorism, [namely] the economic distresses that enable terror groups. It is my opinion that banks have to play a large role in economic growth through SME finance, housing and real estate finance, infrastructure lending, etc,” Fattouh tells Executive.

However, this is exactly where the emphasis on AML and CFT compliance clashes with the banks’ responsibility to expand their national economies. As Fattouh points out, micro entrepreneurs and small business owners more often than not run ventures where compliance checks on their customers are nearly impossible to enforce and financing of SMEs with a dedicated lending program may turn out to be too risky for banks purely from a compliance perspective.

Risks of fixation on AML-CFT

Extreme AML-CFT compliance pressure is counterproductive to the overall global targets of achieving greater financial inclusion and universal access to finance, which have been highlighted most recently in the United Nations’ Addis Ababa Action Agenda, which was globally adopted by UN member states last month at the Third International Conference on Financing for Development in the Ethiopian capital. The agenda noted [in article 38] without being more specific that “some risk-mitigating measures” in finance could create barriers against access to formal financial services by micro, small and medium enterprises.

Risk mitigation, or rather risk deflection, is another AML-CFT induced challenge for the relationships between Arab banks and international banks, as well as among Arab banks themselves. This is because of a temptation for banks to sever correspondent banking ties when compliance requirements make these relationships too cumbersome. Called de-risking, the practice potentially impedes international finance for smaller partners and according to Fattouh is generally ill-advised and not the intention of US stakeholders. “From the point of view of the regulator and the treasury, banks have to continue to understand risk and manage it, not talk about de-risking, and I agree with them. But we are witnessing some international banks cutting their relationships with Arab banks,” Fattouh explains.

De-risking is an economy 101 decision; banks compare the rewards of doing business with individuals and institutions with the cost of compliance attached to having those relationships. This positively implies that decisions on correspondent banking are non-ideological for the vast majority of commercial banks and financial institutions, supporting the assumption that current occurrences of de-risking are a temporary phenomena and will not impede global financial structures in the longer term.

However, Fattouh is concerned that the region’s bankers could lose something much more precious than correspondent banking relations or even licenses: their risk cultures. “My impression is that law enforcement is changing the hearts and minds of bankers, which is very dangerous,” he says. “Banks are by themselves conservative. When they feel the pressure of law enforcement upon them, it changes the spirit and this is my worry, as it could impact the role of banking negatively.”

Practical tools for making the burdens of AML-CFT compliance less costly for Arab banks could include an authoritative regional entity empowered to carry out compliance checking as intermediary for all banks in the region, Fattouh suggests, noting that such an initiative is not currently feasible for the UAB and could be initiated perhaps by the Arab Monetary Fund acting as the secretariat of Arab central banks. However, to facilitate dialog between Arab and international bankers the UAB will expand its private sector dialog program on combating the financing of terrorism from a US-MENA dialog to a EU-MENA dialog, which will be inaugurated on September 3 in Brussels.

[pullquote]“My impression is that law enforcement is changing the hearts and minds of bankers, which is very dangerous.”[/pullquote]

To help Arab banks with the cost and behavior challenges of the many sanctioned waters they have to operate in, UAB is currently working on compiling a code of ethics which, according to Fattouh, will guide banks in their approach to four central points, namely a) rules and regulations, b) corporate governance, c) financial inclusion and universal financial access and d) financing of the economy. The parameters for the project have been assembled and he hopes for publication of the Code of Ethics as guidebook for Arab banks by November, Fattouh says.

In the meanwhile, the American crusade against the financing of terrorism will continue and implicated persons will have to struggle if they want to contest their pariah status. Comments shared by US law firms suggest that even proving one’s innocence has not been the most successful approach for removal from the SDN list – delisting was more often achieved by offenders for admissions of guilt rather than protestations of innocence.

Another option of interest to the region and of great potential business value for Lebanese banks, although not in any way likely to benefit people accused of Hezbollah affiliations, is the change of US political views. As Cuba was finally allowed to hoist its flag over its recently reopened embassy in Washington D.C., it was no surprise that a single OFAC update had already announced the deletion of more than 50 Cuba-related names from the SDN list. What the US calls “sanctions relief” vis-à-vis Iran will take at least several more months to gain momentum, but the prospects for new opportunities from the Iran deal are infinitely more promising than making any attempt to change minds across the Atlantic about the status of people who act as open bank accounts for alleged Hezbollah operatives or invest in mysterious infrastructures that can be used by the organization.