The first time EXECUTIVE met Jean Riachi, chairman and general

manager of Financial Funds Advisors (FFA), was in the

summer of 1998 at the head office of Bou Khalil Markets

in Baabda. The meeting centered around Riachi and Walid El Khalil,

then the head of special projects at Banque Libanaise pour

le Commerce**’s** capital markets division, who were taking Bou

Khalil public.

Even though the private placement and moving

Lebanon’s biggest supermarket chain onto the Beirut Stock

Exchange (BSE) was a success, it was the last time Riachi was

involved in investment banking activities.

“We would like to be investment bankers, but we’re realistic,”

says Riachi. “We know that it’s not possible right now; there is no

market for this in Lebanon.”

Instead, Riachi has kept FFA focused

strictly on brokerage activities and asset management, which has

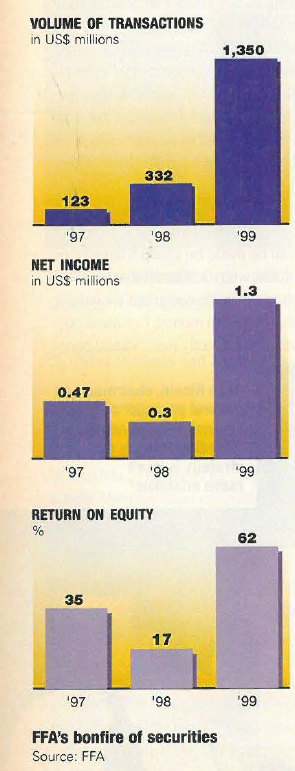

paid off. It got its license from the central bank in 1996 and was up

and running in 1997, the year that trading on the Lebanese equity

markets was in vogue. FFA capitalized on investors’ interests:

Eighty percent of its transactions were on the local markets, and it

pulled in $470,000 in earnings during its first full year of operations.

But the “bull run” was short-lived. Trading volume on the BSE

dropped to $330 million in 1998 from $639 million one year earlier,

and FFA went with it. Profits sank 36% to $300,000.

The logical step? Go where the action is. That’s where Riachi and

his clients headed. Last year, over 90% of FFA’s trading deals were on

international markets, which pushed its trading volume up from $332

million to $1.4 billion. Profits climbed 333%, up to $1.3 million.

Those

who trade only on the local markets sat idling. Banque Audi’s capital

markets division, for example, watched its trade in equity on the BSE

drop from $384 million in 1997 to $39 million last year.

Avoiding full-fledged investment banking, which includes corporate

finance and advisory services, makes sense. Investment

bankers complain that family-run businesses are afraid to lose control

and are not transparent.

They also claim that local companies

are not familiar with investment banks, don’t understand how they

can benefit from such services, and are reluctant to pay fees even

once they are aware of what they can get in return.

If an investment

bank does take in a company, the chances are high that it will be

working with a wily client, according to Nicolas Photiades,

senior vice president at Thomson Financial Bank Watch, a former investment

banker. “It’s too much effort,” he scoffs. “There is not a lot

of cooperation from the client and there’s a lack of transparency,

professionalism and organization.”

Photiades argues that with the amount of time spent working with

a client to finish a deal, the returns are not worth it. “A deal that

would take you a month or two in the West would take you a year

or two here,” he says. “One of my deals took me

two years, which was for no more than $1 million in fees.

If I had done it in London, it would have

taken three months, max.”

To compound the

problem, even if companies want to work with

investment banks and go public, the BSE being in

intensive care is pushing them away.

Lebanon Invest and Middle East Capital Group,

two prominent local investment banks that started

making deals in 1995, have had difficulties facing this

unruly business community. Their solution? Move

their services into the region where more deals can

be made. “With so many problems in Lebanon, you end up

with overheads and might end up with losses,” argues Fouad

Trad, general manager at Credit Agricole Indosuez Liban. “You have

two options: go into regional business or create a regular source of

income, which is asset management and brokerage activities.”

FFA focusing on foreign markets — especially the US — was the

major catalyst in creating growth. But it is not alone. Many investment

houses have caught the wave in equities abroad.

Across town

is Fidus, which has built up a solid client base over the years: It does

at least 97% of trading on foreign markets. Société Générale

Libano-Europeenne de Banque bought a 51% stake in the investment

firm at the beginning of 1999.

“Because Société Générale is an

international name, present in the

US, European, Asian and Middle

East markets, it has added credibility

and confidence to Fidus,” says

Nabil Aoun, who sold his shares but

still runs the firm.

Fidus also benefits

from Société Générale’s client base and through technical assistance from the bank. According to

Ort, Misri & Associates, Fidus carries out at least $6 million worth

of transactions a day.

Local banks have flooded the market by setting up capital market

divisions. Byblos Bank’s brokerage arm is averaging about $5 million

a day in trading volume.

Banque d’ Affaires du Liban et d’Outre-Mer

(BALOM), a subsidiary of Banque du Liban et d’Outre-Mer, has also

been caught up in the rush, watching trading volume

jump 143% and net commissions on share trading

shoot up 135% from the first quarter of 1999 to the

same period this year.

Plus, big foreign firms are present.

Merrill Lynch, the world leader with $35 billion

in total revenues in 1999, has an active branch

in Beirut, while CCF Finance Moyen Orient

moved in a few years back.

Credit Agricole last year

doubled its trading volume, reaching around $2 billion.

“If there is peace, more big foreign institutions

will come into the market,” says Riachi. “It’s a permanent

fight to improve your people, technology and services.”

That’s exactly what FFA is trying to do. Similar to what Merrill

Lynch and Arab Finance Corporation (AFC) provide, FFA just

launched an up-to-date online account.

That gives clients access

through the Internet to their immediate portfolio summary, holdings,

statements, profits and losses, recent transactions and risk management.

FFA also has plans to set up online trading by the end of the year.

AFC has launched “online trading” but is merely passing orders from

clients to brokers to execute. FFA will take on Merrill Lynch, which

already has online trading.

Even though entering cyber trading is considered a must for the

future by many investment firms, there’s hesitation. First, firms are

uncertain about how much money can be made on cheap transactions

online.

Brokerage houses are also in line with local banks that are moving

slowly to accommodate customers with complete e-banking

services.

The general belief: When it comes to money, Lebanese customers

still want to interact with the banker directly (see “Virtual piggy

bank,” February 2000).

“Online trading will eventually come, but it

will be difficult to compete,” says Fadi Osseiran, general manager at

BALOM, which is thinking about offering online trading next year.

“Eventually you give access to clients with virtually zero income on

transactions. But if someone trades online and makes mistakes, he

can’t talk to the computer. He still needs to talk to a person.”

Osseiran anticipates customers using a portion of their money to trade

online, leaving a larger sum in the hands of asset management.

Although FFA has doubts, now might be the time. Some large US

investment firms, like Merrill Lynch, got left behind when online trading

caught on and had to scramble to catch up to retain customers. FFA’s

chief local rival, Fidus, also has plans to launch online trading this year.

Even though FFA is exploring the new world of technology, Riachi

stresses the tight control of its operations.

“When it comes to taking

on new clients, if I feel I cannot handle that many, I stop. I drop clients

that can be a problem; ‘terrorist clients’, which is risky business. We

don’t want risky business,” says Riachi.

FFA also pays close attention

to risk management. By monitoring clients’ investments, it tries to trim

down exposure to risk. “When Nasdaq crashed in April, we didn’t feel

the pain. We have clients that lost money but within an acceptable range,” says Riachi.

Other brokers felt pain with their clients.

“Some bought at the top and

believed that prices would

continue to rise,” says Tarek

El-Ahdab, vice president of

asset management at AFC.

“For some people trading on

leverage, the consequences

were very harsh.”

Brokers at

FFA didn’t have to make any

margin calls during the turbulent

times in the US markets.

Was FFA’s spectacular jump

in earnings last year a fluke?

It might be difficult to repeat,

and Riachi aims at consistent

growth.

“We’ll have growth

unless we make mistakes,”

he says. “The first thing in

our strategy is don’t make

mistakes; make sure things

are operating well before

taking the next step.”

A hint at

FFA’s results in 2000: In the

first quarter, transactions

were $450 million and earnings

came out as $450,000. If

it keeps up the pace, FFA’s

profits will increase about

38%. Not as sensational as last year, but for any investor

or broker, something to

smile about.