Not a bad start.

Only two

years after the

central bank let Credit

Libanais loose in the

market – followed by a

complete restructuring

program (see “Back to

life,” December 1999)it

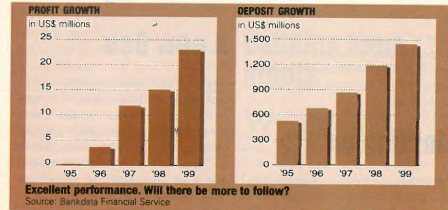

outshone the leading

banks. Net income

jumped 52.5%, from

$15.l million in 1998

to $23.1 million last

year, while average

profits of the top-tier

banks dropped 3.7%

(Bankdata Financial

Services). Bank of

Beirut came in second,

up 27.6%. Credit

Libanais’ strategy is to

become a strong retail

bank, and results are

coming through. It led

its competitors in

deposit growth and non-interest income increased over 10%,

above the two leaders in retail banking,

Banque Audi and Byblos Bank.

But questions are beginning to surface. Is

Credit Lihanais a threat to the top retai I

banks? Leaping into the market with a

splash soon after Saudi entrepreneur

Khaled Ben Mahfouz bought the bank is

one thing; maintaining healthy returns in the

years to come is another. “The test is not

today,” says Ziad Maalouf, vice president at Middle East Capital Group. “The test is

this year and the next few years to come.”

According to Spiro Youakirn, senior

manager of corporate and project finance at

Schroders, Credit Libanais is well positioned

to compete in retail business. It has

a far-reaching branch network with 49

outlets and is highly liquid – 69% of liquid

assets to total assets. Youakim argue~ that

in the long term, “Retail banking revolves around retail lending, and once economic

conditions improve, Credit Libanais will be

able to he a major lender.”

Credit Libanais has already taken a step

forward in lending. Last year its loan portfolio

shot up 43%, “Most of our loan

growth has been in small consumer lending,”

says Andrew Stephens, head of retail

banking. “What we tried to do is speed up

the decision process so the customers enjoy coming to us,

rather than taking a

week or more to get a

loan. For small loans,

we can virtually agree

on the spot.” It also

cleaned up the faulty

loan portfolio inherited

from other banks it

acquired under the central

bank’s control. By

collecting $4.3 million

and writing off bad

loans, its non-performing

loans to gross loans

dropped from 26% in

1998 to 11.8% last

year, which is around

the average for the

leading banks.

Audi is still considered

the leader in producing

products and services:

“It always pays for

Audi to be the innovator

and to be the first in the

market,” says one analyst.

But Credit

Libanais is not far

behind, having already developed insurance,

leasing, phone banking, free Internet and ecommerce

facilities. Already the leader in

credit cards, its number of cards issued and

points of sale through businesses increased

20% last year.

Will it whip out more products this year?

“Enough is enough for now,” says

Stephens. “Customers can only take so

much. They mostly want fast, efficient and

value for money services. They don’t like you to mess around with their money too

much.” Instead, the bank will focus mostly

on cross selling existing products, which

fits in with its restructuring program to be

more sales oriented, turning its outlets into

points of sale.

Credit Libanais is also looking into

acquiring the American Express outlet in

Lebanon, which has over $80 million in

assets, within the next few months. “It’s a

good small bank that has a small portfolio

with prime, high net worth customers,”

says Credit Libanais’ chairman and general

manager Joseph Torbey. The bank knows

American Express well: It has an exclusive

partnership with the American bank as the

service provider for it~ cards, accepted only

through Credit Libanais’ network.

But some analysts see a weakness Credit

Libanais bas to work on to be a real competitor

in retailing and maintaining steady

growth. “The new upper management that

was acquired recently is high caliber, but

human resources and services at the outlets

have to improve,” says one analyst. “If you

want to establish yourself as a retail bank, it’s

the service and the quality of staff behind it.

Credit Libanais is slower in tenns of training

and improving the quality of service,

especially compared to Banque Audi.”

Stephens replies: “We’ve recognized it and

we’re doing something about it. Training

began 12 months ago, and it will go on and

on.” Another issue is cost control. Its costto-

income ratio came out at 60.5% in 1999,

higher than Banque du Liban et d’Outre-Mer

(44.3%), Byblos (52.8%) and Audi

(56.2%). But with increasing efficiency

being a part of the restructuring program,

Credit Libanais’ cost-to-income dropped

7 .2 % from 1998, the largest decrease

among the top-tier banks.

After an initial burst of growth, it will be

interesting to watch how Credit Libanais

does from here on out. But the bank has an

idea of where it is heading. “What Credit

Libanais started two years ago was a statement

that we’re open for business,” says

Stephens. “We’ve put the building blocks in

place and we’ve done some good business.

We’re going to build on those building

blocks, and I see no reason why we can’t

sustain steady growth and be prepared to

take on opposition.”