Salim Sfeir, sitting in his modest conference room at the Bank of Beirut’s headquarters, gives the impression of a mild-mannered chairman and general manager, content with where the bank stands. In an interview with EXECUTIVE, he chose his words carefully, and his voice certainly didn’t rock the Richter scale. But don’t be fooled. This is the man who has led one of the fastest growing banks in Lebanon since BoB came about in 1993.

It started small: only five branches with $101 million in assets and earning only $37,000 in its first year of operations. But by the end of 1999, its assets, deposits and profits grew on average by a whopping 62.89%, 78% and 139.5% annually. And there is another positive sign. Last year’s merger with Transorient Bank, which pushed BoB from a medium-sized bank into the top 10, was a successful marriage. The mixing of two corporate cultures and synergies is never easy: more than half of all mergers in the West fail. And BoB did not swallow up Transorient. They were of equal size, both had 14 branches, and must have had differences in business philosophies.

“It was a very good merger,” says Talal Ghali, senior associate at Middle East Capital Group (MECG). “It was successful, smooth; the mixing of the two corporate cultures was good, synergies were fine and it boosted BoB’s growth.” The numbers speak for themselves. Last year, BoB’s earnings jumped 27%, from $14.1 million to $18.1 million. From the 1999 consolidated income statement relative to the 1998 unconsolidated income statement, net interest income jumped 59.7%, and non-interest income soared 138.7%.

Now that the merger is complete, what will the bank be up to this year? The bank is concentrating on what shareholders want to hear: strengthening profitability. “It has been a fixture within the bank,” says Sfeir. “We focus more on profitability than on growth. This is our main strategy.”

Troubleshooting will be one of Sfeir’s tactics this year to continue strong profit growth. “We will be looking at whatever weaknesses we have,” says the chairman. “For profit centers that are not yielding returns, we expect to correct those weaknesses. For example, if there is a branch that is losing money, we’ll focus on it to make it profitable by the end of the year. If there are services that are not making money, we’ll see what the weaknesses are in the department and make it profitable.”

But BoB is doing more than just looking for weaknesses to maintain a steady growth pattern. It just created an asset management department that will run private banking. The private banking arm will be fund-oriented and will operate in a conservative fashion. “We are creating our own funds presently, but mutual funds outside will also be available,” says Sfeir. “It’s more of a capital preservation strategy, rather than a risky approach with a lot of profits on one day and losses on another day. This is why we are focusing on fund management.”

Private banking is not an easy chore; it takes time to develop and convince customers to come on board. But, according to Ghali, “This is an area of growth in Lebanon. There is a huge market for it. Lebanon has a substantial number of high-net-worth individuals.”

Last year, BoB did not emphasize new products and services while it was concentrating on the merger. It already has a strong product base to work from, including savings plans for all ages, an insurance program, Visa and MasterCard credit cards and bill-paying services. BoB also has a capital markets division, providing brokerage services on equities both locally and internationally, plus dealing with Lebanese T-bills on the secondary market. It is heavily involved in trade finance, ranking in the top ten for letters of credit in 1998 before the merger. Since then, its volume has increased considerably, which according to BoB, may have placed it as the leader in the sector.

Although the bank is hesitant to disclose plans for expanding products and services, financial controller and IT manager Sami Saliba offered a few hints. It will expand on its plastics business, especially targeting new clients that use cards more regularly. BoB also plans to launch e-banking this year, see “Virtual piggy bank,” p. 38. Its goal is to offer a full-service Internet package, such as transferring funds, applying for loans, paying bills, trading currencies and checking equity markets.

But one important development that may give a push to BoB’s profitability is its strategic alliance with the Dubai-based Emirates Bank International. One of the Gulf’s leading banks, EBI bought into BoB in 1997, 10%, and the two came up with a scheme that is generating another income stream for the local bank. What do the two banks offer? “All banking activities,” says the chairman. BoB recently changed its slogan to “Banking beyond borders.” This allows an expatriate in the United Arab Emirates to buy a house for his family in Lebanon, transfer money and do trade financing, for example.

A full range of products and services offered through a new channel could boost BoB’s net interest and non-interest income. But there is more. With the economic slowdown, spreads tightening as interest rates drift lower, and the market oversaturated with 65 banks, the heat is on the sector and is creating tough competition. One solution for local banks is to go international, see “Welcome to the real world,” Jan. 2000. Expanding regionally is a start and now is a good time. According to the Economist Intelligence Unit, the economic growth rate in the Middle East will be one of the fastest in the world in 2000, except for Lebanon, which is projected to come in dead last.

“Our relationship with EBI is opening up new markets for Bank of Beirut,” says Sfeir. “It’s helping us penetrate, which is a long-term strategy.” At present, BoB has representatives in several countries in the Middle East. But, says Saliba, “We are concentrating more on regional business; we’ll be more aggressive this year than last.” BoB is also thinking about setting up branches in the region. When is not clear; Sfeir will only say the bank is “assessing the markets.”

BoB’s strategies appear sound, but a question remains. In the midst of a recession that is affecting the entire sector, will the bank be able to report strong earnings in the near future? The first sign of the economic slowdown creeping up on the banks came in 1999. In the first three quarters, the average profit growth for 13 of the top leading banks dropped 3% year-on-year. From the full-year results that came out as EXECUTIVE went to print, Byblos Bank, ranked third by total assets in 1998, reported flat profit growth, and Banque Audi, fourth by total assets, experienced an 11% decrease in earnings. Watch out for Fransabank, Société Générale Libano-Européenne de Banque and Banque Libanaise pour le Commerce results, their third-quarter earnings fell 23.5%, 33.3% and 36.6% respectively.

Although some banks are faring well, BLOM has become the benchmark of how to make money in the face of recession, see “Cool conservatives,” Nov. 1999. Riding through the storm, BLOM’s profits last year jumped 20%, from $58.7 million to $70.4 million.

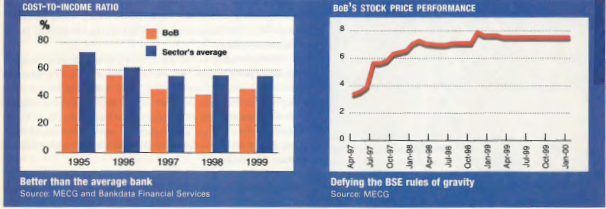

One of the keys to making it through a recession and strengthening earnings is cost control. BLOM is one of the best in the market. It was able to lower its cost-to-income ratio from 56.8% in 1995 to 38.2% in 1999. BoB is also sensitive to efficiency; its cost-to-income ratio dropped from 64% in 1995, ranked 23rd in the sector, to 42.5%, ranked 4th, in 1998. “This is another fixture of the bank,” says Sfeir. “We always focus on lowering our costs.” According to Saliba, the bank closely watches every penny, even the chairman’s business lunch expenses have to pass through the proper channels.

Yet in 1999, its cost-to-income ratio, excluding non-recurring merger charges, climbed to 46.6%. But, according to Sfeir, the increase can mostly be accounted for by some expenses that came from the merger but were not recorded in accounting for the merger costs. Some examples are upgrading hardware to handle the two systems, redecorating the new branches, and consulting fees. On track with its cost-control obsession, BoB cut the initial swelling of its staff during the merger from 498 to 417 and is aiming to reduce that to 400 by the end of 2000. According to Ghali, BoB’s cost-to-income ratio in 1999 was still far below the average for the sector, estimated at 55% by MECG, and its efficiency will remain a competitive advantage.

BLOM has also mastered pulling in large deposits, even though it has one of the lowest deposit rates. The so-called “BLOM premium” comes down to a customer perception of BLOM as the safest bank. But BoB is also able to have low deposit rates and keep the deposits flowing. In 1999, its average deposit rates fell from 8.7% to 7.5%, a full percentage point lower than the average deposit rate. Nonetheless, BoB’s deposits grew 16.7%, reaching $1.3 billion, last year, despite stiff competition to attract deposits. It was also substantially above MECG’s estimate for the average of the peer group, up 7% to 8%. On the income side, by lowering its deposit rates, BoB’s net interest spread increased from 1.9% in 1998 to 2.6% in 1999.

“Bank of Beirut has established itself with a brand name,” says Ghali. “BLOM has differentiated itself from other banks as the ‘BLOM premium.’ But Bank of Beirut is coming up with the ‘BoB premium.’ It’s visible now, it launched campaigns, it tells you how important it is. Customer service is an indicator of how the brand name is being established; it’s on the right track.”

On the lending side, BLOM is very conservative. Its loan-to-deposit ratio was below 25% in the first half of 1999 while BoB’s ratio stood at 38% at the end of 1999. However, its ratio is below MECG’s calculation for the sector’s average in 1999, up around 50%. BLOM mostly lends to high-net-worth corporate clients. Unlike the sector’s increase in non-performing loans, NPLs, BLOM’s ratio of NPLs to gross loans decreased from 7.3% in 1997 to 6.3% last year. BoB generally targets small- to medium-sized businesses and individuals. That’s a little more risky, but analysts believe that BoB’s risk management department is good at being selective in choosing customers. According to MECG, its ratio of NPLs to gross loans in 1999 came out at about 10%, a drop from around 15% in 1998.

For investors, it may be difficult to speculate on BoB’s share price performance. In the last year-and-a-half, trading volume and stock prices on the Beirut Stock Exchange have tumbled. The BLOM index fell 20.9% in 1999. Following the good price performance of the bank’s shares after it was listed in April 1997, it has leveled off since spring 1998, but avoided the bad showing by most of the shares on the market, see graph.

BoB’s price/earnings, P/E, ratio is in the safe zone, at 13.1, based on 1999 earnings and the share price on January 28. The bank is expected to pay out 25% of its net income in 1999, the same as last year, a 0.12% dividend yield. Its return on average equity increased to 21%, one of the strongest in the sector. However, it is still not known when the BSE will emerge from its torpor. Furthermore, some analysts believe that although its shares are reasonably priced, other banks are cheaper, considering that its P/E ratio is the second highest among listed banks, see chart.

But BoB is generally considered to be a long-term buy. “If somebody wants to buy in Lebanese equities, BoB has to be included. It has been resilient to the downturn of the overall market. It will be paying the same dividends as last year and will continue to pay good dividends,” says Ghali. There is also faith in the management of the company. “They have the management to outperform other banks in terms of bottom line growth,” says Financial Funds Advisors chairman and general manager Jean Riachi. “They proved that hard work counts. Delivering is important to them, and they never miss any loophole anywhere. They never sleep.”

Sfeir’s style of management drives Riachi’s point home. He uses a hands-on approach, close to the dirty work with the rest of the management, and has an open communication policy, wiping out the layers that a manager has to go through to talk with him. And the management usually works from at least 8 a.m. until 8 p.m. As long as Sfeir is omnipresent, there is a good chance that BoB will defy the economic slowdown and show healthy growth in profits.