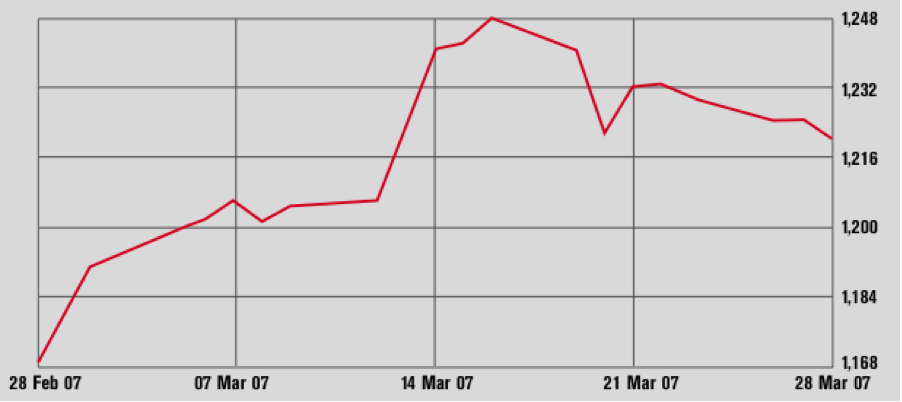

Beirut SE: Blom (1 month)

Current Year High: 1,625.45 Current Year Low: 1,168.36

Between Feb. 28 and March 16, the BSE saw a spike in hope, as much as spikes go in a coma. The index moved from a year low of 1,168.36 points in late February to 1,248 points on March 16, basically driven up by talks between the opposing sides in the Lebanese political quagmire. As the voices announcing impending solutions faded, so did the traders’ enthusiasm and the third week pushed the BSI lower, to 1,224.19 points on March 26. Research, which Dubai-based investment bank Shuaa conducted on Audi Saradar banking group and concluded with a Neutral recommendation, led Audi to shoot back and claim that the fair value of its stock is significantly better than the $61.09 calculated by Shuaa. Audi shares closed at $63 on Mar 26.

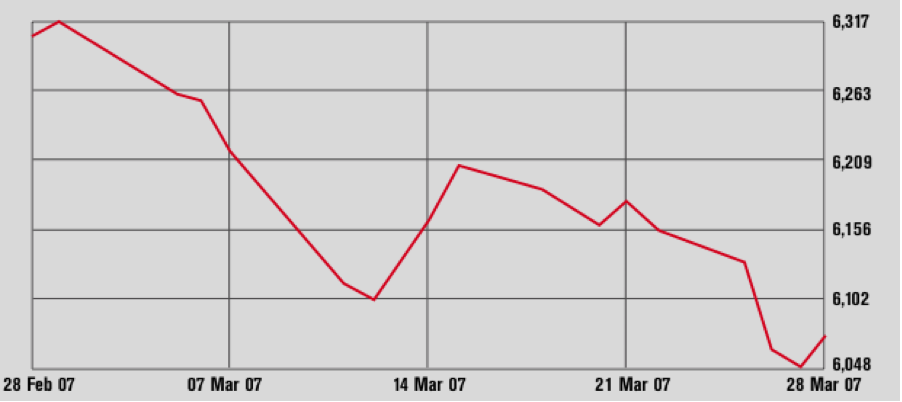

Amman SE (1 month)

Current Year High: 7,407.15 Current Year Low: 5,267.27

The Amman Stock Exchange moved sideways in a range above 6,200 points to close at 6,219.51 points on Mar 26. Arab Bank made headlines, beginning with having to deny a story in a US newspaper that warmed up allegations from a lawsuit that the bank had been used to finance “terrorism.” Later in March, the bank said it halted negotiations on a share sale to a strategic investor thought to be Emaar Properties, and the Jordanian government was said to be increasing its shareholding in Arab Bank in order to keep the Hariri family shareholders from buying up a controlling stake. The stock saw some lively trading in March, with a downward drift. Real estate firm Taameer Jordan was one of the main volume movers toward the end of March. Its share price regained in the second half of the month what it had given in the first half.

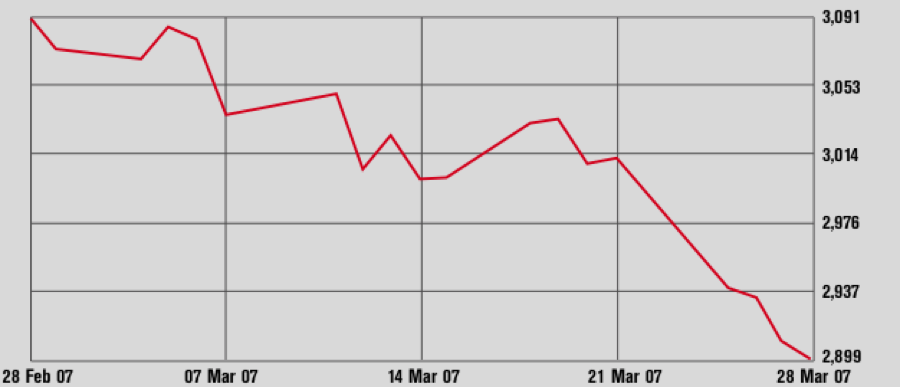

Abu Dhabi SM (1 month)

Current Year High: 4,648.80 Current Year Low: 2,899.43

The Abu Dhabi Securities Market could not sustain the gains it had made in late February when it clawed its way above 3,000 points. The index dropped by 4% between March 1 and its close of 2,939 on March 25. At the end of the month, property and energy stocks were on the sunny side of the ADSM while banking values were selling. National Bank of Abu Dhabi, which issued 40% cash dividend and 30% bonus shares on March 22, traded down by 11% in the week between March 19-26. Banking news from neighboring Dubai with its impending merger between Emirates Bank and National Bank of Dubai mean the NBAD will, upon completion of the merger, lose its claim to being the biggest bank in the UAE.

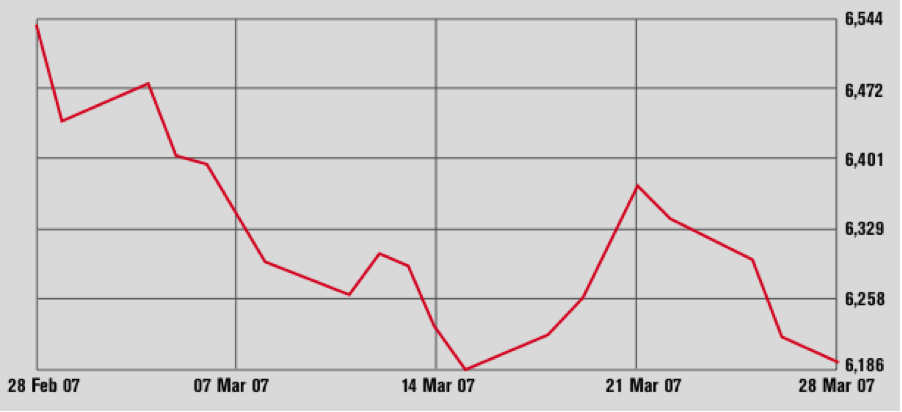

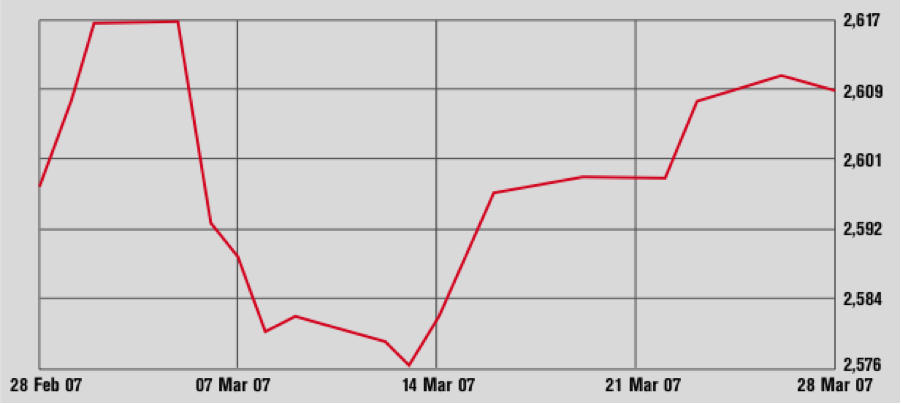

Dubai FM (1 month)

Current Year High: 6,987.91 Current Year Low: 3,675.93

The DFM had a bad month in March, as its index weakened by almost 13% to a new year low of 3,675.93 points on March 25, from 4,207.51 points on Feb. 25. The DFM’s own shares started trading. Emaar, which pleased some analysts with a lower than expected dividend of 20% but disappointed stock owners with the move, traded down and was pushed even to a 12-month low of AED 10.60 on March 25 after Dubai Holding said it will acquire 28% in Emaar through a land-for-shares deal. Shuaa Capital bought back 3 million shares and the stock jumped 10.8% on a single day with high trading volume before sliding again.

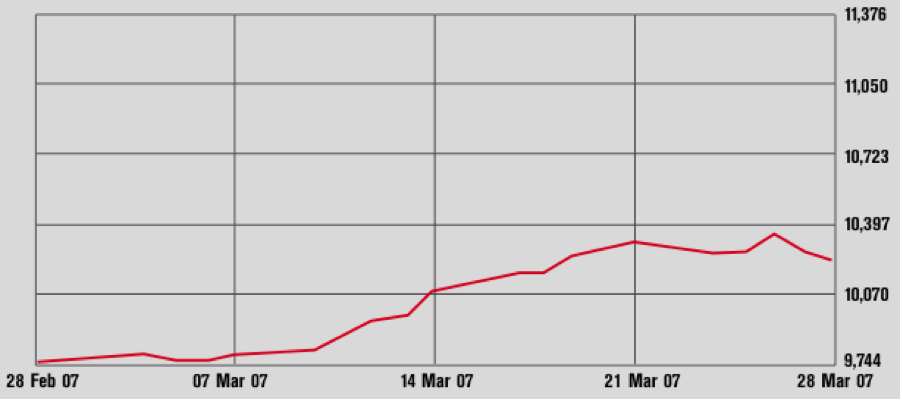

Kuwait SE (1 month)

Current Year High: 10,812.30 Current Year Low: 9,164.30

The Kuwait Stock Exchange had a period of growth as its index strengthened by almost 6% to 10,341.3 points on March 26 from 9,769.2 points on Feb. 27. Telecommunications events supplied major influences on the KSE. In the beginning of the month, the share price of Kipco got a boost from the company’s extraordinary profit from selling shares in Kuwaiti mobile operator Wataniya to Qatar’s Qtel. Shares of MTC, the leading telco in Kuwait, advanced 15% to KWD 3.20 on Mar 26, from KWD 2.79 on Feb. 28. At the end of March, MTC emerged as highest bidder in the contest for Saudi Arabia’s third mobile phone license.

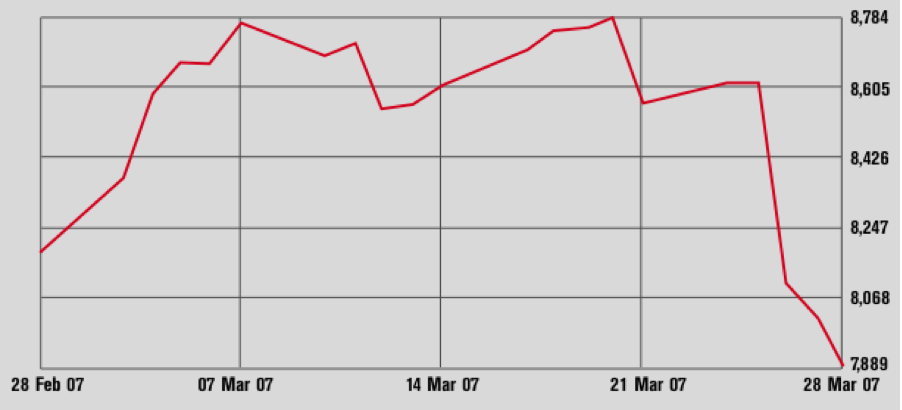

Saudi Arabia SE (1 month)

Current Year High: 17,730.96 Current Year Low: 6,916.85

The Saudi Stock Exchange ended a month of modest gains and sideways movements with a splash of cold water. The TASI lost 522 points, or just over 6%, on March 26 in its worst one-day drop since falling 6.3% on July 19 of last year. Sell-offs on March 26 included blue chip companies and leading banks such as Sabic, Al Rajhi Bank, SEC, and the two telcos. For the month, the market moved from 8,356.48 points on Feb. 27 to 8,098.36 points on the evening of March 26. Insurance industry IPOs came in a bundle of five simultaneous subscription offerings worth combined SAR 266 million. The Saudi government created a new $320 million company to operate the SSE, with a long-term view of taking the bourse public.

Muscat SM (1 month)

Current Year High: 5,956.46 Current Year Low: 4,657.16

After a slide in February to 5,781.1 points on Feb 26, the Muscat Securities Market went down by 216.73 points, or 3.7%, between Feb. 26 and March 14 before regaining some ground to close at 5616.24 on March 26. The sultanate’s primary market raised new expectations as four companies announced IPO plans. Besides engineering firm Galfar’s OMR 60 million flotation, Oman Merchant Bank and government-owned investment firm Takamul (in May) and Oman Oil Marketing Company are the IPO candidates for 2007. Additionally, Al Omaniya Financial Services will float a two-year OMR 8 million convertible bond.

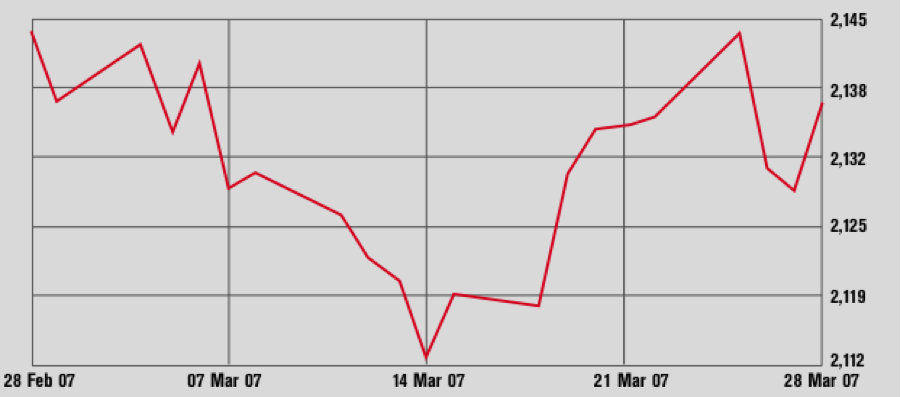

Bahrain SE (1 month)

Current Year High: 2,251.15 Current Year Low: 1,996.68

The Bahrain Stock Exchange closed at 2,130.71 points on March 26, down by 0.6% when compared with its level on Feb. 27. The index had dipped lower in the middle of the month but things appeared uneventful and volumes were once again low. Esterad Investment Company moved up 12% in the second half of March and Nass Corp saw some volume toward the end of the month. Mobile phone operator Batelco announced the purchase of 20% in Yemeni network SabaFon for $144 million.

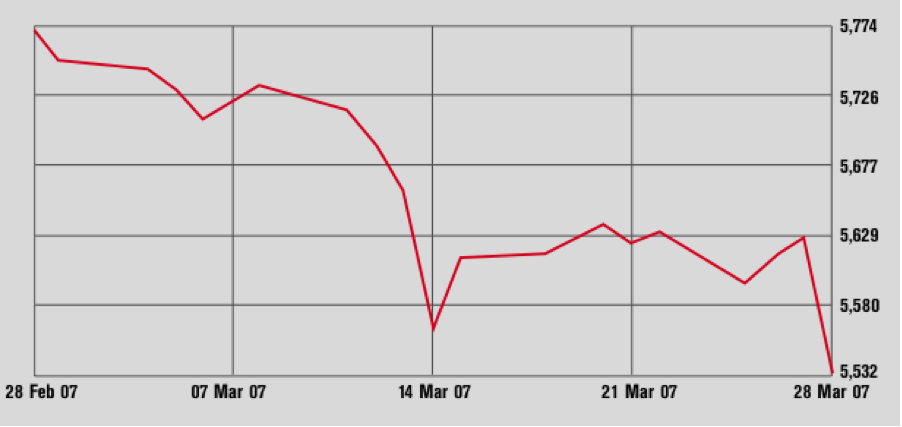

Doha SM: Qatar (1 month)

Current Year High: 9,878.10 Current Year Low: 5,825.80

The downward movement of the Doha Securities Market slowed but did not cease and the DSM index slipped 3.5% to 6,060.16 points on March 26 from 6,277.1 points on Feb. 27. This performance put the DSM again as the GCC’s largest underperformer for the year-to-date with a drop of 15% since Jan. 1. After dividend events, banking stocks such as Ahli and Commercialbank paced the market’s downward trend in the later part of the month. Qtel, which initiated the purchase of 51% in Kuwait’s Wataniya telecom, stabilized toward the end of the month. Nakilat continued its rise that started in February and gained 18% in March. DSM market authorities suspended a brokerage for one month for violating regulations.

Tunis SE (1 month)

Current Year High: 2,712.33 Current Year Low: 1,861.15

The Tunisian Stock Exchange in March traded sideways on a high plateau and the Tunindex closed at 2,610.14 points on March 26, about 100 points below its year high from Feb. 9. Tunis International Bank participated as lenders in a 55 million euros project finance facility for a new residential project in Libya, the first such finance arrangement in Libya’s real estate sector.

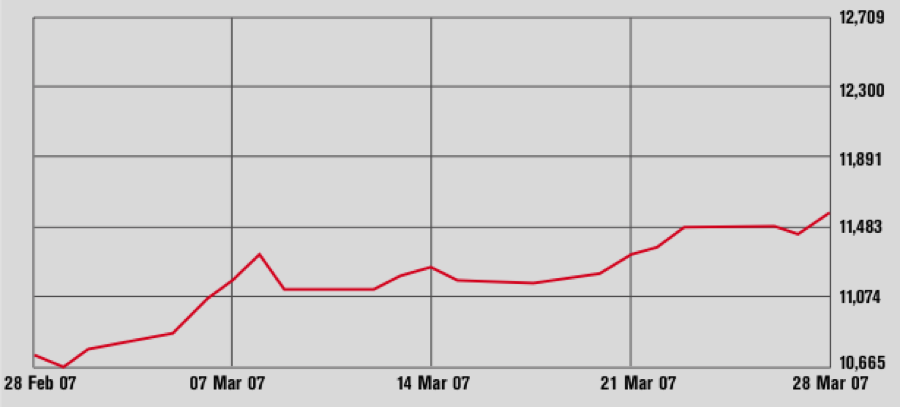

Casablanca SE All Shares (1 month)

Current Year High: 11,552.97 Current Year Low: 6,563.27

The Moroccan exchange broke through the 11,000 points line in early March and scaled further index gains to close at 11,478.87 points on March 26 in continuation of its rise which brought its gain for the year to date to a tidy 21%. Morocco’s central bank said it expects commercial banks in the country to be compliant with Basel II rules by this summer. With ongoing reforms, the central bank also hinted that a loosening of restrictions on investing in foreign bourses might be on the books, which might take steam out of the Casablanca Exchange and its extended rally.

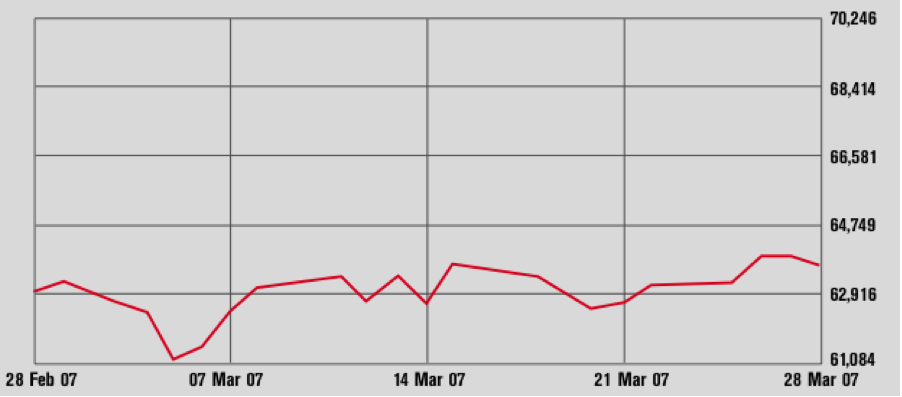

Cairo SE: Hermes (1 month)

Current Year High: 65,135.08 Current Year Low: 41,965.37

The Cairo and Alexandria Stock Exchanges entered the month with a week of downward motion to the 61,000 points level but the index moved back up and closed at 63,859.80 points on March 26. While Telecom Egypt shares made some gains in late March on news of higher 2006 results and a very faint outlook of a secondary 20% flotation in a few years’ time, Orascom Telecom Holding received three regulatory decisions against its MobiNil affiliate and got disqualified from bidding for the third Saudi mobile license, with rumors going wild on the reasons. Al-Watany Bank found several suitors interested in buying a strategic stake. Emaar Properties subsidiary Emaar Misr said it would file a complaint over a CASE decision refusing to list its shares.