Beirut SE: Blom (1 month)

Current Year High: 1,934.21 Current Year Low: 1,177.03

In beleaguered Beirut, the Blom Shares Index managed to rise to 1208.57 points on the last Friday of January, an improvement of some 30 points since the start of the year which nonetheless is an achievement, given the circumstances of continued demonstrations in the Lebanese capital and a one-day violent “general strike” which saw the BSE closed. After Lebanon was promised $7.6 billion in new international funds on Jan. 25 but simultaneously suffered bloody street fighting, Lebanese stocks moved two directions the next day—major banks went down while Solidere nudged up. Authorities in Ajman, UAE, announced that Solidere will be involved in a new urban development project there. Bank Audi said it expanded the number of its listed GDRs by a small percentage. Byblos Bank announced a new private equity fund in collaboration with the European Investment Bank.

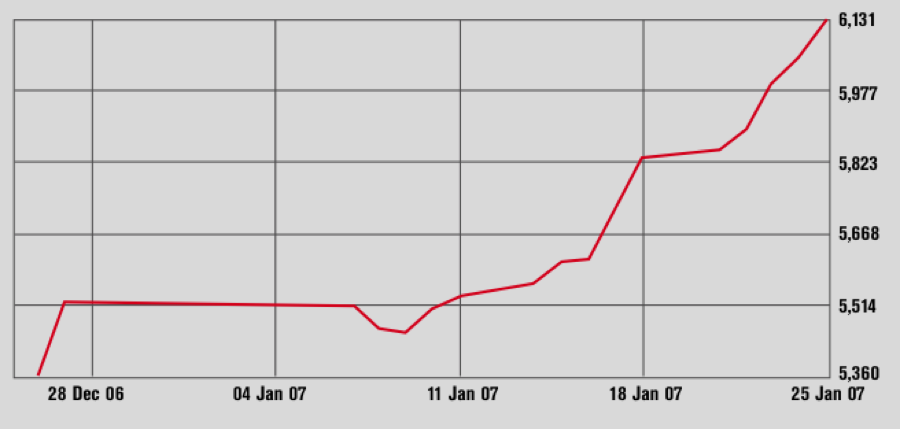

Amman SE (1 month)

Current Year High: 8,730.58 Current Year Low: 5,267.27

The Amman Stock Exchange outdid its regional peers from the start of the year and improved 11.1% to 6,130.61 points on Jan. 25. Brokers in Jordan jubilated about new buying interest by Gulf investors, attributing it to good banking results and low share prices. Banking was the driver of ASE growth. Market behemoth Arab Bank thrived in 2006 and announced 31.6% higher net profit for the year. The bank’s share rose by over 18% in January even before Arab Bank announced its profit and said it would consider 25% cash dividend for 2006. Two real estate development firms, Afaq and Methaq, had shareholders approve capital increases and Industrial Development Bank said it would invite strategic shareholding by Dubai Islamic Bank and Dubai Jordan Investment later this year. Jordan Telecom considered downsizing its capital significantly.

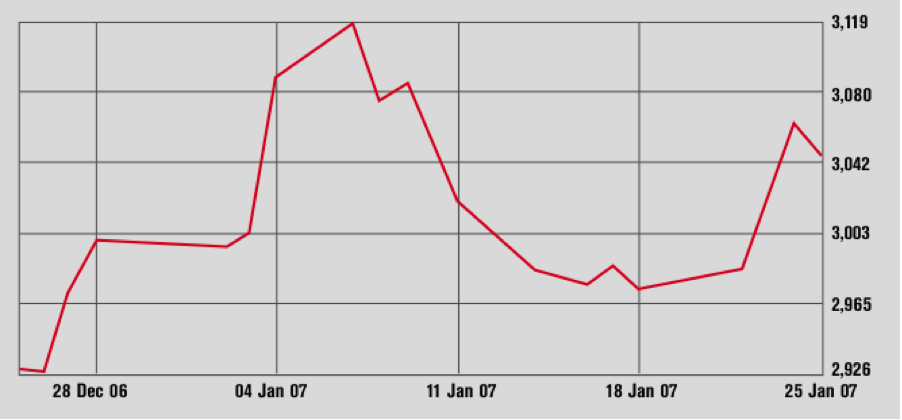

Abu Dhabi SM (1 month)

Current Year High: 4,939.18 Current Year Low: 2,925.03

The Abu Dhabi Securities Market didn’t stray far from the 3,000 points line in January and concluded the year’s first four trading weeks 1.36% up at 3030.5 points on Jan. 28. Aldar Properties was among the most active stocks along with Arkan Building Materials which was the biggest new name on the bourse with an AED 1.75 billion IPO. Arkan’s share price jumped from AED 1.25 to AED 1.66 on the second day of trading and closed at AED 1.29 on Jan. 28. Two companies from Fujairah also went public on the ADSM. Construction supplies firm Fujairah Building Industries assumed trading on ADSM on Jan. 11 at AED 3.85 and slipped to AED 3.71 on Jan. 15.

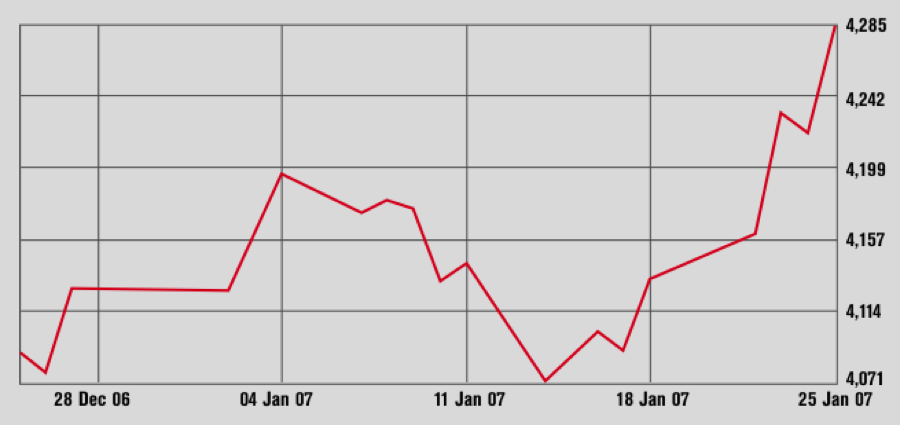

Dubai FM (1 month)

Current Year High: 7,608.99 Current Year Low: 3,997.29

The Dubai Financial Market moved in positive territory during much of January and climbed some 240 points in the second half of the month to close at 4,314.46 points on Jan. 28. As with all markets of the region, earnings season loomed large over the DFM where analysts forecasted 2006 company profits to show 15 to 20% higher. According to analysts, some companies have multiplied profits in 2006 but such performance did not translate into universal share price gains for these firms in January. Dubai Investments improved by over 10% in the course of the month but didn’t shine in the dividend announcements. Emaar Properties achieved incremental improvements and got a small boost in volume late in the month on news that Deutsche Bank saw it as a “buy.”

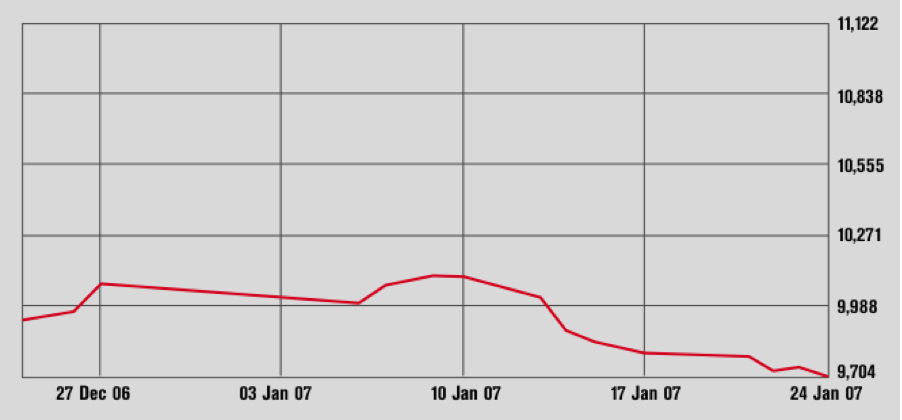

Kuwait SE (1 month)

Current Year High: 12,054.70 Current Year Low: 9,164.30

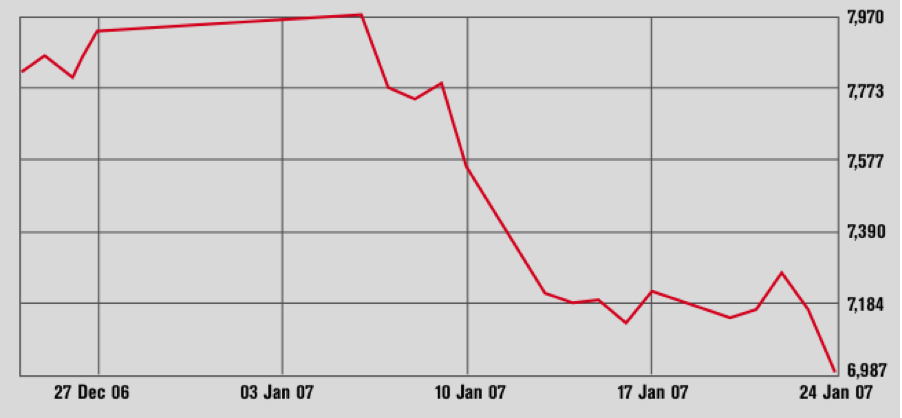

The Kuwait Stock Exchange started the year with a rise above 10,000 points in the first week after its long holiday break but slipped in the third and fourth weeks of January to close at 9,707.5 points on Jan. 27, down 3.58% since the start of 2007. The imbroglio over the government contracts of logistics firm Agility carried on with statements and counter-statements which sent the stock dipping in the middle of the month. Telecommunications firm MTC advanced in the first trading week of the year and again started to climb in the last week upon announcing plans to list on the London Stock Exchange a year from now. NBK saw a massive spike in volume after releasing record profit figures on January 23. Investment holding KIPCO gained 20% early in the month and was also among January’s more active stocks. Very high asking prices by international firms for building the large Al Zour refinery led the Kuwaiti government to ask the bidders to revise their offers.

Saudi Arabia SE (1 month)

Current Year High: 20,634.86 Current Year Low: 7,665.73

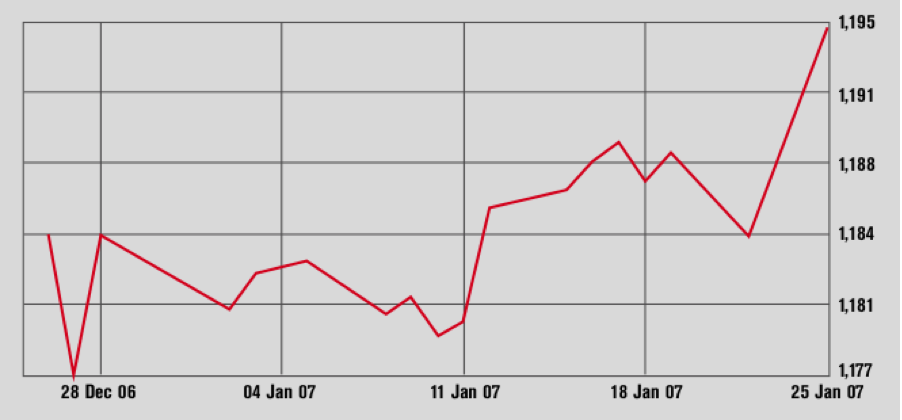

The new year has arrived and the Saudi market didn’t change direction. The Tadawul Index rolled to less than 7,000 points, closing at 6922.13 points on January 27—already down by 12.75% from the start of the year. Positive was newly listed Advanced Polypropylene Company which debuted on Jan. 20 and announced a few days later it obtained an SR 1.2 billion loan to build its production plant. The stock, which most people prefer calling APPC, leapt 60% in its first week of postpartum trading to SR 16 on Jan. 27. Market heavyweight Sabic, which had nosedived in the first half of January, climbed SR5.5 in the week after announcing annual results. Another potentially positive factor was a CMA decision to temporarily suspend two companies, the more prominent of which was Anaam, a company formerly specialized in livestock trading.

Muscat SM (1 month)

Current Year High: 5,956.46 Current Year Low: 4,657.16

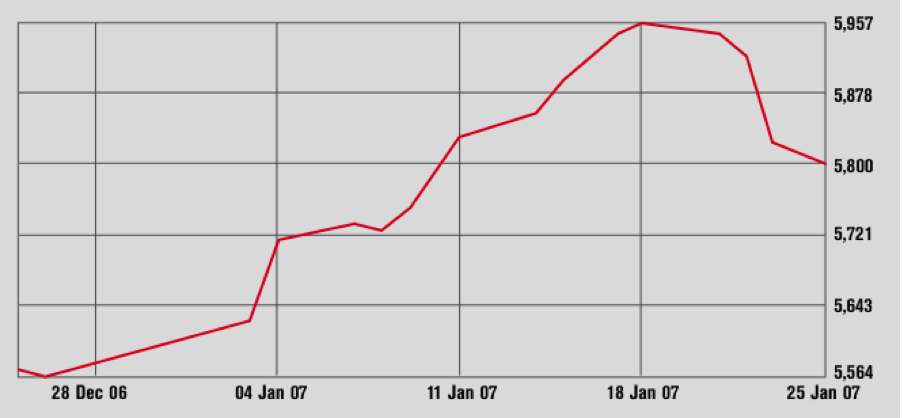

The Muscat Securities Market rode to a new historic index record of 5,829.1 points on Jan. 11 after which it let out some steam and closed at 5,769.6 points on Jan. 28. Oman was all banking news in January. The two largest banks by market cap., BankMuscat and National Bank of Oman (NBO), announced respective profit gains of 33% and 50% in their 2006 results. Shares of BankMuscat dropped a few baisas in the week after the bank published its results on Jan. 22. Shares of NBO, which had made some gains in the first half of January, did likewise. Bank Sohar, which offered 40 million shares in a month-long OR 20 million initial public offering that closed January 7, saw its IPO five times oversubscribed. It was the Sultanate’s first IPO in 18 months and Bank Sofar is expected to start trading this month.

Bahrain SE (1 month)

Current Year High: 2,347.01 Current Year Low: 1,996.68

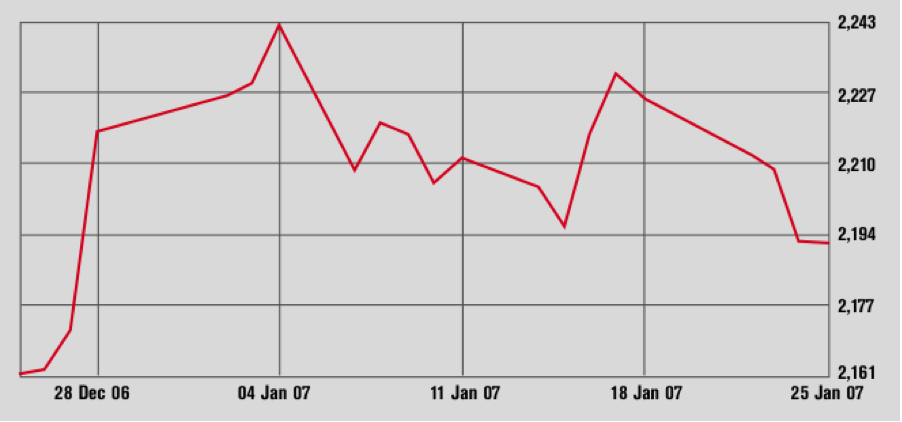

Stocks in Bahrain slipped in the last week of January and closed January 28 at 2,191.37, lower by 1.63% compared with the start of the year. Volumes remained unexciting on many trading days and serious fluctuations rarely occurred. On Jan. 28, for example, 28 stocks saw no action while nine losers stood vis-à-vis four gainers and four stocks that traded without price movements. Gulf Finance House was among the more vibrant movers, rising from $2.41 at the start of the month to $2.70 on Jan. 18 to recede to $2.49 on Jan. 28. Shares of Batelco, National Bank of Bahrain, Ithmaar Bank, and Ahli United Bank also saw noteworthy activity. Sharia-compliant leasing specialist, First Leasing Bank, which is not traded on the BSE, completed an $89 million private share placement.

Doha SM: Qatar (1 month)

Current Year High: 10,781.12 Current Year Low: 5,825.80

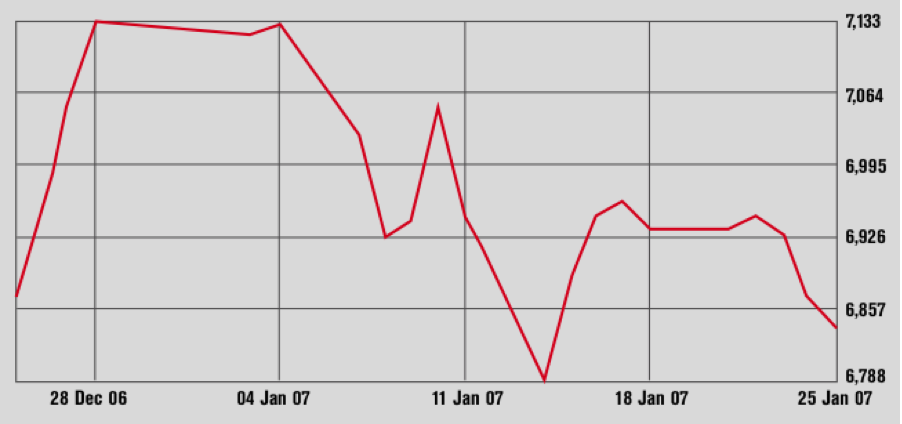

Index movements on the Doha Securities Market pointed southwards at the end of January as the DSM ended the Jan. 28 trading day at 6,781.08 points. This represented a drop of 4.93% from the start of the year but one wants to be mindful of the fact that December had been a month of rebounding in Qatar from index levels below 6,000 points. Earnings and dividend announcements had significant impact on share movements, with banking stocks at the center of attention. Barwa Real Estate also grabbed a lot of attention—it lost almost 20% in the first half of January, but rebounded with news of new projects and new financing deals. LNG tanker company Nakilat issued a cash call for the second half of its capital asking shareholders to pay up QR 5 per share between Feb. 1-15.

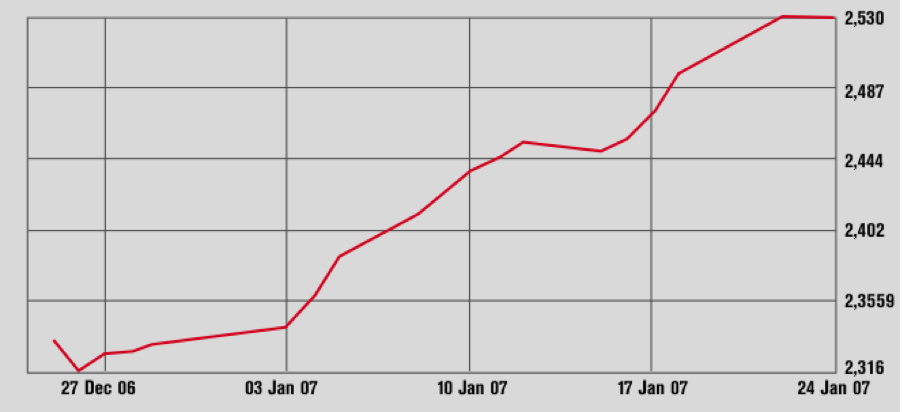

Tunis SE (1 month)

Current Year High: 2,529.53 Current Year Low: 1,681.90

The Tunisian Stock Exchange rocked its way into 2007 and had a month of solid 8.06% improvement in its index. It closed at 2,518.81 points on Jan. 26. Shares of private equity and funds firm, Tuninvest, surged by 28% in January to 11.90 Dinars on Jan 22, from where they retreated slightly to TND 11.16 on Jan. 26. Leasing shares were among the most active shares in late January trading. Sector firm Tunisie Leasing, whose shares appreciated by 17% in the first half of January, lost close to half of its share price gains in the second half of the month. Similarly, Arab Tunisian Bank shot up 32% before profit taking brought the stock lower. Banque de Tunisie, the largest listed bank and the bourse’s leader in market capitalization, ended January 11% higher compared with the start of 2007.

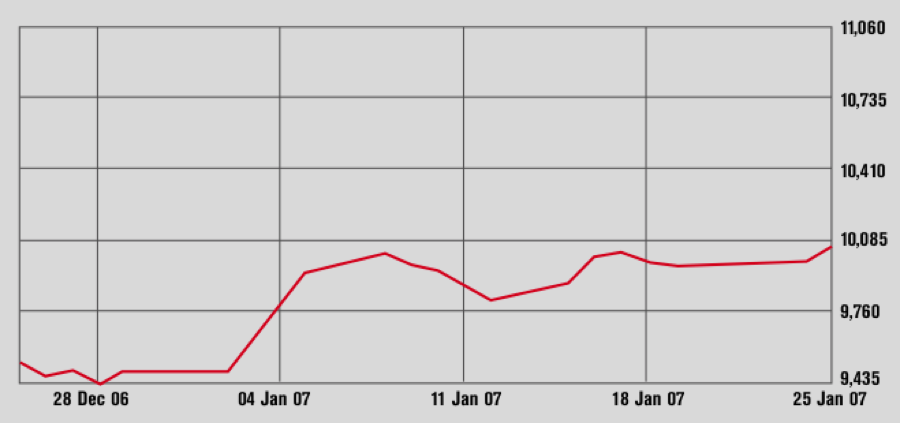

Casablanca SE All Shares (1 month)

Current Year High: 9,109.55 Current Year Low: 5,337.53

Humphrey Bogart should be thinking to take his Rick’s Café Americain public. The Casablanca Stock Exchange, after an index dip in the second half of December, moved up in January and closed at 10,217.59 points on Jan. 26, a new index high and an improvement of 7.79% year-to-date. Of major stocks, Attijariwafa Bank showed a notable share price performance and gained 9% from MAD 2,310 on Jan. 2 to MAD 2501 on Jan. 26. The Economist Intelligence Unit says that Morocco’s textile and manufacturing industries should have a growth year in 2007 because of demand in Europe and the country’s Free Trade Agreement with the United States.

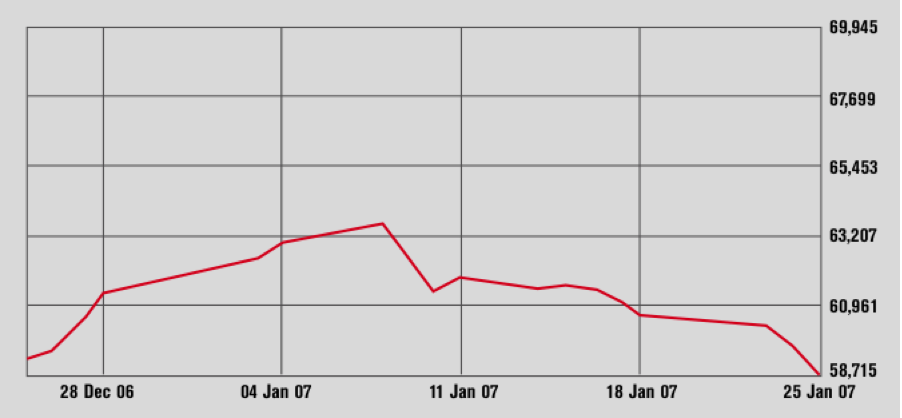

Cairo SE: Hermes (1 month)

Current Year High: 68,994.73 Current Year Low: 41,965.37

Egypt’s Cairo and Alexandria Stock Exchanges got off to a not-too-strong start in 2007. After gains in the first week, the Hermes Index reflected market losses in the rest of the month and closed at 57,236.56 points on Jan. 28, down 6.61% year-to-date. Orascom Telecom Holding had a rather bad month and dropped from LE 400 on Jan. 4 to LE 370 on Jan. 28. EFG Hermes had it even worse and slumped from LE 42.11 on Jan. 4 to LE 32.40 on Jan. 26—although the share got a “Strong Buy” recommendation with a target price of LE 52 from analysts at competitor Prime Securities. CASE contracted Scandinavian stock exchange operator OMX to create a new trading system for the Egyptian bourse.