Significant Increase of Tourists from Jordan

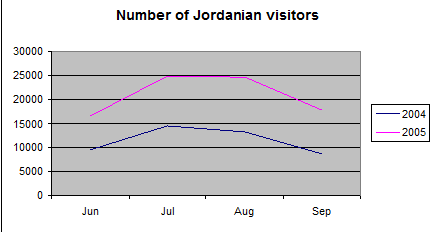

Statistics released by the Ministry of Tourism show a dramatic increase in the number of Jordanian visitors to Lebanon, due to the easing of the visa requirement that came into effect in June 2005. During the June-September period, the number of Jordanians tourists rose by 82% compared to the corresponding period in 2004.

Tax Free Spending by Jordanians on the increase

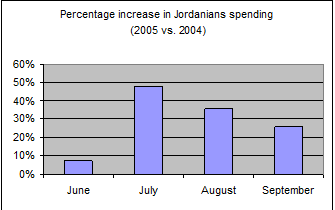

The increase in inbound tourists corresponded with a significant rise in spending by Jordanian tourists during the June-September period. It peaked in July, when spending increased by 48% compared to July 2004. With regard to ranking of top spenders by nationality, in the June-September period Jordanians came in fifth place after Saudi Arabia, Kuwait, Egypt, and the United Arab Emirates. Jordan climbed one spot, up from sixth position for the corresponding period in 2004.

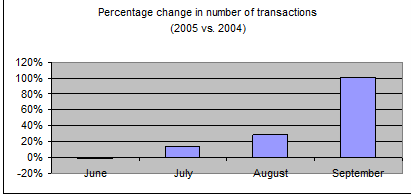

Once the number of Jordanian visitors started increasing in June 2005, a rise in the number of Tax Free shopping transactions was anticipated. In July 2005, the number of transactions exceeded last year’s figure by 14% and it steadily increased until September when it reached as high as 101%.

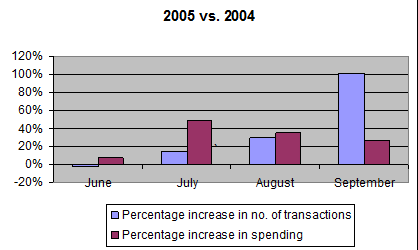

The rise in Tax Free shopping transactions, however, did not always correspond with an increase in spending in monetary terms. For example, in July 2005 the number of transactions rose by 14% and spending increased by 48% compared to the same period in 2004. Then in September 2005, the number of transactions rose by a staggering 101% but spending rose by just 26% compared to the same period in 2004. It is therefore safe to conclude that the subsequent rise in transactions indicates a greater awareness about Tax Free shopping by Jordanian tourists.

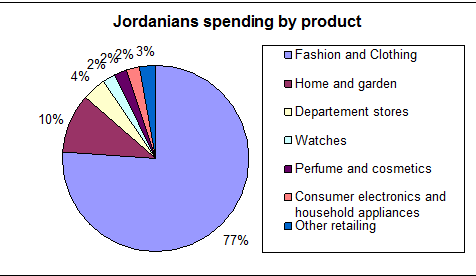

Preferred products among Jordanians:

The preferred product category among Jordanian tourists was fashion and clothing, which accounted for 77% of their total spending in the June-September 2005 period. Home and garden items follow with a 10% share. Interestingly, watches accounted for just 2% of their total spending, down eight percentage points from the 10% share it constituted for the corresponding period in 2004.